Green planning is emerging as the progressive policy paradigm for decarbonisation. In the UK, the current Labour government’s ambitious clean power agenda and Industrial Strategy testify to a decisive shift away from the free-market fundamentalism that has long dominated the political spectrum, especially after Thatcher came to power in 1979.

But green planning must also become effective in delivering on its promise. Putting this paradigm into practice depends on the state's capacity to deliver public investment at scale, provide key goods and services and coordinate various actors. A capacity that decades of privatisation and market-oriented reforms have drastically eroded.

Rebuilding a functional institutional architecture is a precondition for any future green planning to succeed. It requires, as a first step, a clear understanding of the entities currently in place, including their respective responsibilities and interactions.

This study offers a pioneering insight into the existing UK institutional architecture for potential green planning. It does so by mapping and assessing central-government public institutions across four policy fields: international, macro-financial, cross-cutting and sectoral.

The preliminary results are mixed, showing some potential but also significant shortcomings that should be addressed with the repurposing of existing institutions and, where necessary, the creation of new ones.

International and macro-financial institutions, in particular, hold mandates that are ill-matched to the roles required under a green planning framework. Cross-cutting and sectoral institutions, meanwhile, often combine inconsistent legal statuses with unclear relations and responsibilities — both among themselves and with their supervising departments.

No blueprints without spades. The long list of advisory and regulatory bodies is no substitute for executive entities capable of directly undertaking public investment programmes and providing essential goods and services. The UK lacks public corporations with a direct capacity to deliver on the green plan’s sectoral decarbonisation objectives. Those that do exist, often lack the adequate scale and mandate.

The main UK public financing institutions (UKEF, NWF, BII, BBB, NHB) and non-financial corporations (GB Energy, GBR and others) cannot achieve the systemic scale needed to support green planning objectives unless they are separated from the government’s accounts and granted autonomous borrowing powers — as it is already in most other European countries.

Central government public institutions pursue their mandates independently and often replicate institutions from devolved nations and local authorities. Beyond drafting the plan itself — as a bottom-up exercise synthesising inputs from the main stakeholders — a newly established central planning institution should be responsible for the governance and supervision of the green planning process.

On 14 March 1932, John Maynard Keynes concluded a BBC radio broadcast wishing success to “state planning by Public Corporations responsible to a democracy in Great Britain”.[1] Keynes was not just making the theoretical case for economic planning.[2] He was also sketching the architecture of a future British planning system, with a functional division of roles between elected and administrative institutions.

The post-war configuration of the UK planning system was, perhaps inadvertently, quite resemblant of Keynes’ suggestion.[3] Subsequent governments from 1945 until 1979 established a comprehensive architecture of planning institutions made of public financing entities, public corporations controlling nationalised industries, state-owned manufacturing companies, planning authorities and state holding bodies. These enabled successive governments to influence not only the volume of investment but also its direction, shaping structural change in the British economy.[4]

Those post-war planning institutions began to be dismantled during the Thatcher era, with their final dissolution taking place under the Major and Blair governments in the 1990s. However, in the current state of permanent “polycrisis”,[5] the need for effective government intervention is resurging. “Missions” and “strategies” are part of the new vocabulary of policymaking, especially for the current Labour government. Yet beyond the stated ambitions, what institutional capacity actually remains to address today's interconnected economic and climate challenges?

Answering this question, through a detailed mapping and assessment of the existing institutional architecture, is a key prerequisite to embracing a successful green planning approach over the next decade. Although focused on the UK case, this study offers a replicable methodological framework, suitable for other national contexts. As such, it is intended not only as a domestic policy contribution but also as a blueprint for comparative analysis and international dissemination. A parallel review of US planning institutions will follow.

This study maps and assesses a defined set of UK entities — hereafter defined as “green planning institutions” — that is public institutions with sovereign responsibility for decarbonisation.

[.box][.box-paragraph]Institutions. The term institution is used here in its broader sense and encompasses a range of entities in the form of legal persons. Individual “actors” — or natural persons — are therefore excluded. [.box-paragraph][.box-paragraph]Public. Public institutions are legal entities belonging to the public sector, as classified by the Office for National Statistics (ONS) in accordance with the international statistical standards set out in the UN System of National Accounts 2008 (SNA 2008).[6] Private companies, third sector entities (charities, social enterprises) and other civil society associations (trade unions, industry bodies) are likewise excluded.[.box-paragraph][.box-paragraph]Sovereign. The term refers to public institutions whose administrative level corresponds to the sovereign state — in the UK case, HM Government. This excludes potentially relevant public institutions tied to the devolved nations — such as the Scottish National Investment Bank (SNIB), Cardiff Airport in Wales, or Translink in Northern Ireland — as well as public bodies linked to local authorities, such as Transport for London (TfL) or Manchester Airport. [.box-paragraph][.box-paragraph]Decarbonisation. This category further narrows the scope of investigation to public institutions with major direct or indirect policy responsibility for driving decarbonisation. It excludes institutions active in other policy domains (e.g. education, health, security, culture) — such as Universities, the NHS,[7] the Post Office, national museums and galleries, HM Prison Service and several others.[.box-paragraph][.box]

[.fig][.fig-title]Figure 1: Green Planning Institutions In The UK[.fig-title][.fig-subtitle]Perimeter of entities surveyed and appraised in this study[.fig-subtitle][.fig]

[.notes]Source: Author’s analysis.[.notes]

This methodological choice restricts the sample to a limited number of “most relevant” institutions, with some degree of discretion arising from their varying characteristics. The institutions considered differ in territorial scope: some operate across the entire UK, others across Great Britain, and others still within England and Wales, or England alone. They also vary in ownership structure — some are classified as “public” despite being only partially government-owned. Finally, “green roles” — whether actual or potential — constitute the core mandate of some institutions, while forming only part of the broader remit of others. Nonetheless, the set is sufficiently homogeneous to support valid comparative analysis and classification.

Public institutions in the UK maintain a hierarchical dependence — or other formal relationship — with at least one of the 24 ministerial departments in HM Government. This study considers 93 institutions, linked to 12 ministerial departments. Each surveyed green planning institution can be further classified according to its institutional type, legal status, function and mandate (see Appendix for definitions).

To identify shared functional roles across the long list of institutions, we propose an analytical taxonomy that groups them around four key policy fields: international, macro-financial, cross-cutting and sectoral. Within each policy field, institutions are mapped according to the ministerial department that oversees them.

These are institutions that operate abroad or in relation to international matters — through trade policy, foreign investment screening, development finance, multilateral cooperation, or supply-chain diplomacy — yet with significant implications for the domestic economy. The international dimension is crucial — even the largest economies, such as the US and China, cannot approach green planning in a fully autarkic mode. Clean energy and technology manufacturing is inherently global, and several supply-chain segments display extreme concentration in China, particularly the refining of critical minerals, the manufacturing of solar PV components and the production of battery cells.[8] This makes importing manufactured equipment an inescapable necessity for a medium-size economy. While international trade in clean energy technologies accounts for roughly 30 per cent of their total value globally,[9] the UK faces a much higher import dependence. By 2030 this is estimated to reach 47 per cent in battery cells, 99.5 per cent in solar panels, and 100 per cent in most critical minerals (with the sole exception of lithium).[10]

These are institutions responsible for fiscal policy, monetary policy and financial stability. Under a green planning framework, macro-financial policy should enable a higher volume of green investment — both public and private — whether directly, through public spending or indirectly, by shaping the financing conditions that determine the cost and availability of capital for private investors. Global green transition investment and spending reached $2.3 trillion last year,[11] though China accounted for over one-third of that, equivalent to more than four per cent of its GDP. In recent years, the UK has outperformed similar European economies (except Germany) in terms of total energy transition investments. In 2025, the UK invested $85.3 billion (around 2.2 per cent of its GDP). Yet,this was mainly driven by individual consumer spending on purchases of passenger electric vehicles (EVs), while investment in renewable energy (at $16.9 billion) remained below the level of ten years earlier.[12] This figure is still significantly short of the £30.9 billion average annual investment required to achieve the Government’s plan for clean power by 2030.[13] Meanwhile, investment in electrification of heating and industry decarbonisation is also expected to rise.

These are institutions whose functions cut across different policy subfields. Under a green planning framework, some would provide analytical inputs, design the plan and oversee its implementation with coordinating powers. Others would play a critical role in mobilising and directing financial resources — particularly important given the need to cover the high upfront capital costs that are especially sensitive to interest rates, as is the case for renewable energy capacity and power grids. A further group would act as “enablers” of green planning, involved in the delivery of public infrastructure, fostering supportive competitive conditions, promoting research and innovation, managing public land and developing the skills required for jobs in the green transition.

These are institutions directly involved in the sectors where decarbonisation must take place. In descending order of their share of UK total emissions.[14] These sectors are domestic transport (30.8 per cent), buildings (21.9 per cent), agriculture (12.5 per cent), industry (11.2 per cent), electricity supply (10.2 per cent), fuel supply (7.4 per cent) and waste (5.8 per cent). The UK is also typically a small net source (0.1 per cent) of emissions in land use, land-use change and forestry (LULUCF) — a category that can in principle function as a net “sink” of greenhouse gases. It is worth noting that, although electricity supply accounts for an increasingly marginal share of climate-related emissions (having fallen by 82 per cent in absolute terms since 1990), fostering green electrification is essential to enabling decarbonisation across the full range of emissions-intensive sectors, for instance through the deployment of electric vehicles and heat pumps.[15] Public institutions operating in the electricity sector are therefore particularly salient to any comprehensive green planning approach.

Within each of these four policy fields, we identify specific potential roles that could be assigned to individual institutions under a future green planning approach

Under a green planning framework, institutions operating at the international level should aim to increase the resilience of clean energy and technology supply chains from the UK’s perspective — reducing the country’s import dependence while securing the flow of green products needed for domestic deployment.

Specifically, they could perform two main roles:

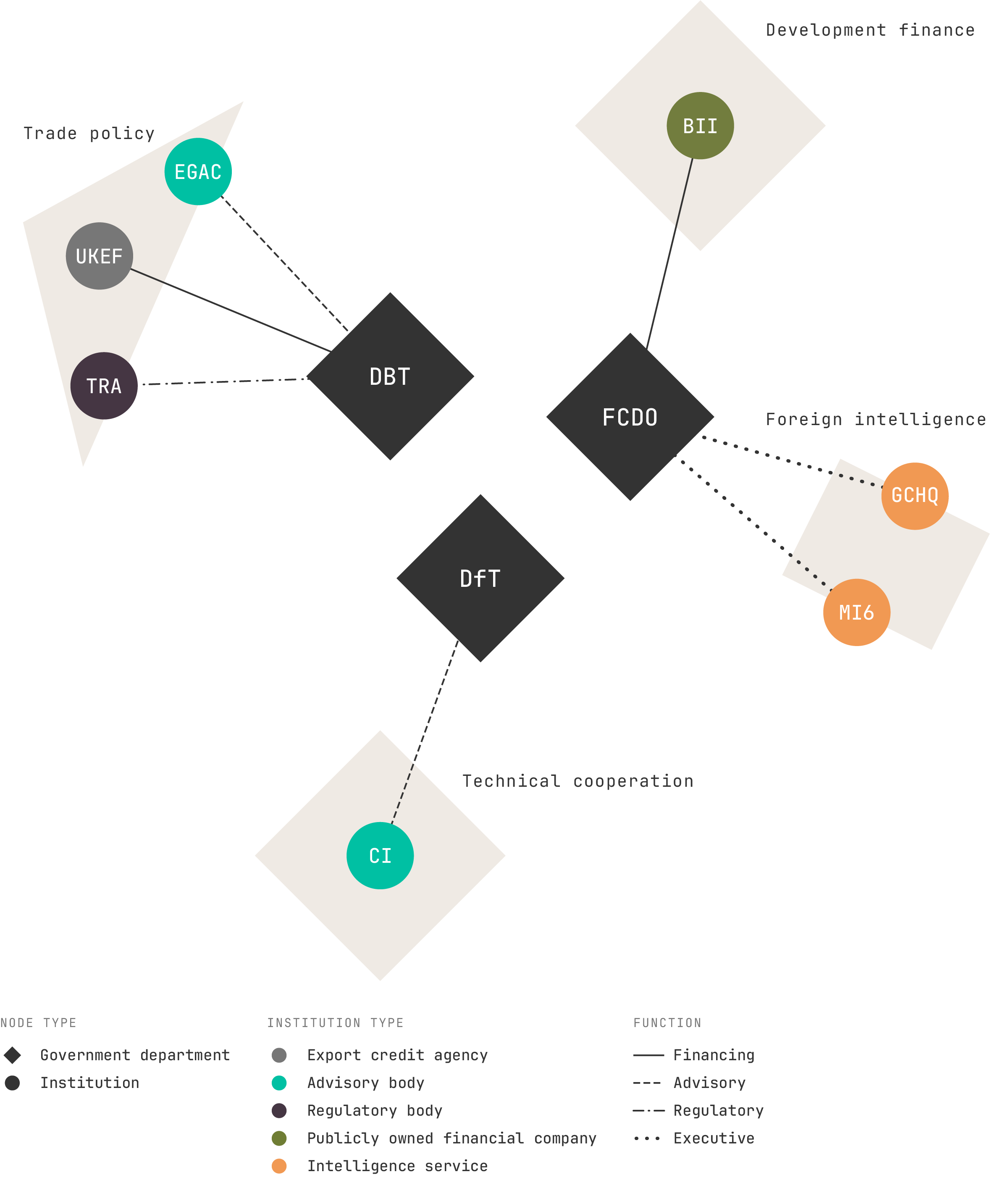

International institutions operate under three ministerial departments: primarily the Foreign Commonwealth and Development Office (FCDO) and the Department for Business and Trade (DBT), and marginally the Department for Transport (DfT).

[.fig]Figure 2: International Institutions[.fig]

[.notes]Source: Author’s analysis.[.notes]

FCDO works with the two foreign intelligence agencies — Government Communications Headquarters (GCHQ) and the Secret Intelligence Service (MI6) — which could prove instrumental in mapping global clean energy and technology developments as well as in sharing knowledge with international counterparts.[16]

FCDO also owns British International Investments (BII), the UK’s development finance institution, which by statute operates independently of the interests of specific UK businesses. Nevertheless, BII could help establish commercial and diplomatic channels with recipient countries, particularly where this is directed towards initiatives in clean energy and technology supply chains.

DBT acts at the international level through its remit over trade policy, which it assumed from the Department for International Trade (DIT), when the latter was incorporated in 2023.[17]

DBT’s principal institution, holding ministerial department status, is the export credit agency UK Export Finance (UKEF).[18] With a maximum exposure limit of £80 billion, UKEF is the largest public financial institution in the UK. UKEF provides insurance to British exporters against non-payment by overseas buyers and extends guarantees to UK banks on loans made to overseas borrowers when purchasing UK goods and services. UKEF itself works in conjunction with the Export Guarantees Advisory Council (EGAC), an expert committee that advises the DBT Secretary of State and the CEO of UKEF on the environmental and climate implications of UKEF’s operations.

A DBT-sponsored regulatory body, the Trade Remedy Authority, investigates unfair trade practices affecting UK industries.

DfT controls Crossrail International (CI), a public corporation that advises foreign transport ministries and public transport authorities on how to develop and deliver complex rail infrastructure projects.

The UK lacks institutions responsible for securing “green imports” and foreign direct investments in clean energy and technology manufacturing

UK international institutions are predominantly “outward-looking”, concerned with the defence or promotion of UK businesses abroad, principally through exports. At present, they are neither actively pursuing inward foreign direct investment in domestic clean energy and technology manufacturing, nor deliberately working to establish bilateral cooperations with other countries — and their principal business players — for the supply of green materials and equipment. The only major exception consists of UKEF’s programmes for critical minerals supply — namely the Critical Minerals Supply Finance and Critical Goods Export Development Guarantee — which nonetheless benefit UK exporters exclusively.[19]

Responsibility for attracting investment sits with DBT and the Office for Investment (see cross-cutting institutions below), with no deliberate differentiation between domestic and foreign investment. This distinction is particularly salient, given that clean energy and technology manufacturing is largely dominated by non-UK players. Moreover, DBT's international trade mandate includes no specialised function for the “planning” of imports — a role whose potential applications range from stockpiling of solar panels to procuring other key inputs such as critical minerals or battery active materials.

The dispersal of institutional roles across multiple departments is a major obstacle to activating a green planning mandate for international institutions

DBT currently oversees international trade as part of a broad portfolio that is largely focused on domestic issues, while FCDO covers foreign affairs more generally, including the UK's economic interests abroad. Consolidating these mandates within a new dedicated ministerial department, with an extended remit over international clean energy and technology supply chains, would facilitate green planning in the international domain.

Under a green planning framework, macro-financial institutions should unlock and accelerate greater volumes of green investment.

Specifically, they could pursue three distinct roles:

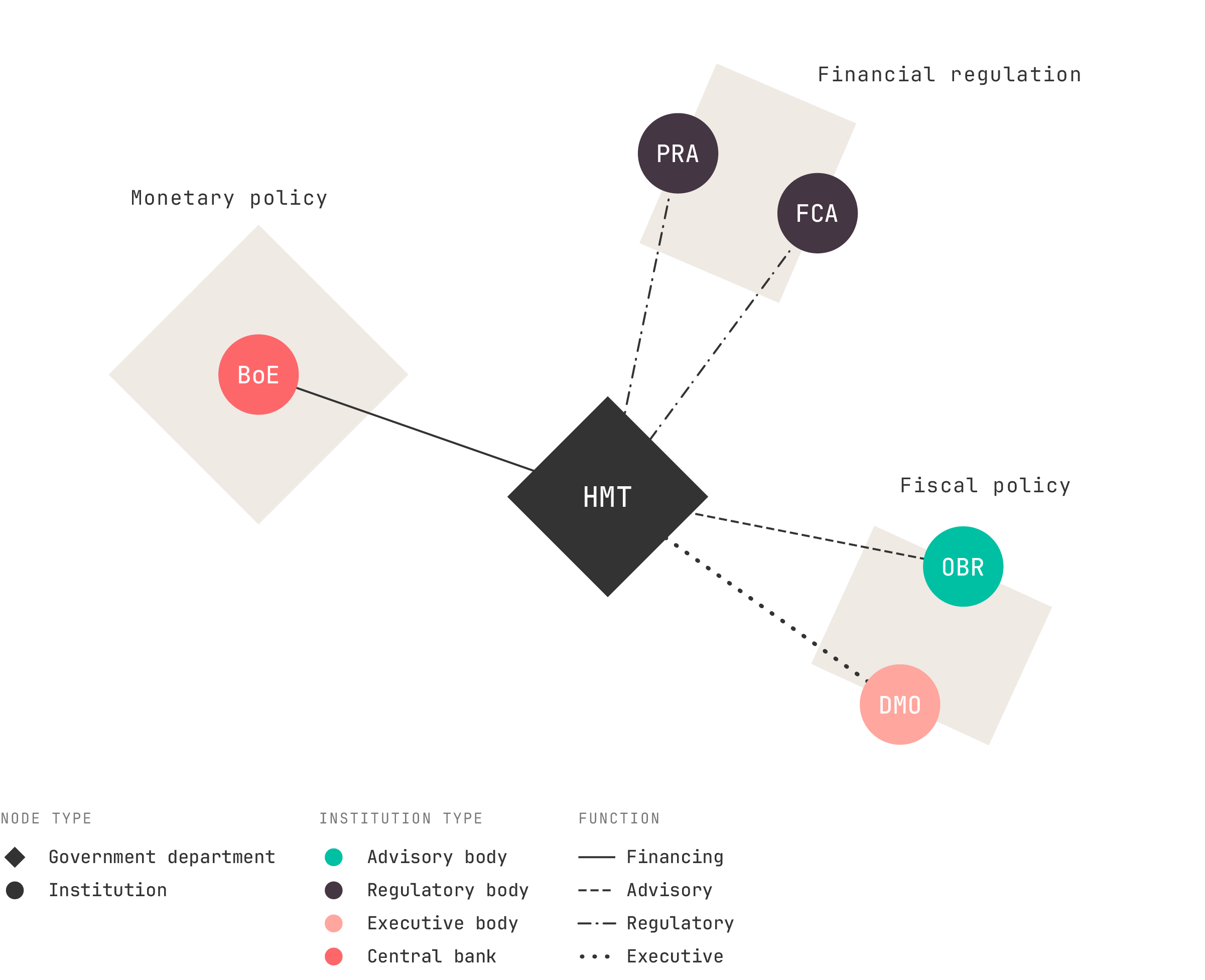

Macro-financial institutions are clustered around the diarchy of HM Treasury (HMT) and the Bank of England (BoE), the latter formally owned by HMT but operationally independent from it.

[.fig]Figure 3: Macro-financial Institutions[.fig]

[.notes]Source: Author’s analysis.[.notes]

The current arrangement between these two institutions has been in place since the Bank of England Act 1998,[21] which granted the Bank of England (BoE) full independence from the Government in setting interest rates and taking other monetary policy decisions, while enshrining price stability as the Bank’s core mandate. At the same time, the 1998 reform transferred responsibility for gilt issuance from the Bank to a new executive agency under HMT — the UK Debt Management Office (DMO) — now in charge of debt and cash management.

Since the 1997 Budget, HMT has conducted fiscal policy under targets that constrain borrowing and spending, with the prime objective of containing debt levels. Initially, the new fiscal framework permitted borrowing to fund investment on average over the economic cycle. However, fiscal rules became more stringent with the Fiscal Responsibility Act 2010 under the Brown Government, and were further entrenched under the Coalition Government (2010-2015) with the passing of The Budget Responsibility and National Audit Act 2011, which established the Office for Budget Responsibility (OBR).[22] The OBR examines and reports on the sustainability of public finances under the framework set out in the Charter for Budget Responsibility. In practice, its forecasts delimit fiscal policy decisions on overall spending and borrowing.

Finally, macroprudential financial oversight rests with the Bank of England's Financial Policy Committee (FPC), which complements the Monetary Policy Committee (MPC) within the Bank's policy architecture. In practice, the MPC sets monetary policy, while the FPC monitors systemic risks to financial stability. Microprudential financial supervision is divided between the Financial Conduct Authority (FCA) and of the Prudential Regulation Authority (PRA), which work respectively with HMT and within the Bank of England. The FCA regulates the broader financial industry in the interests of consumers, while the PRA supervises the operations of major financial institutions — banks, insurance companies and other entities.

The UK does not lack the macro-financial institutions needed for green planning. The main incompatibility with green planning objectives lies in their mandates.

The current fiscal rules are ill-suited to green planning, as they fail to recognise capital expenditure as fundamentally distinct from current spending. The new fiscal framework introduced in 2024, which targets public sector net financial liabilities (PSNFL) rather than public sector net debt (PSND), created some additional fiscal space by netting out government liabilities against illiquid financial assets.[23] Moving to a measure of public sector net worth (PSNW) would open further room for public investment manoeuvre through the offsetting weight of non-financial assets — whose definition depends in turn on whether the entity against which financial claims are held is classified as public or private.[24]

Perhaps more significantly, deconsolidating publicly owned entities of a commercial, revenue-generating nature from the government budget would exclude their borrowing operations — used to finance investment — from classification as public sector liabilities. This is an accounting anomaly peculiar to the UK and at odds with the European System of Accounts (ESA 2010), under which public corporations affect general government accounts only through specific transactional links — such as non-market capital injections, subsidies in the form of current transfers and guarantees called.[25]

These constraints are reinforced by the role of the Office for Budget Responsibility (OBR). Because fiscal rules are anchored to the path of the debt measure at the end of the forecast window, the OBR’s projections effectively determine the space available for new public spending. Under a green planning framework, this arrangement would prove obstructive, since the OBR’s projections and recommendations would limit the scope for additional public investment. At present, the OBR exercises an influence on fiscal policy unlike that of any other independent fiscal authority across Europe.[26] National independent fiscal institutions (IFIs) in the EU monitor and assess the fiscal policy of their respective governments, typically after the annual budget has been approved.[27] In contrast to the UK, EU finance ministers are not required to justify expenditure decisions that deviate from the projections of their independent fiscal authority.

So long as maintaining price stability through interest rates remains the Bank of England’s core mandate,[28] any inflationary episode driven by higher fossil fuel costs will paradoxically hamper capital-intensive green investment, as the BoE will be compelled to raise interest rates. What amounts to a short-term measure to curb inflation through the demand channel can have long-lasting negative effects on supply,[29] particularly on the green technologies and infrastructures that could structurally prevent fossil fuel-driven inflationary episodes in the first place.

In 2016, the BoE did intervene in the corporate bond market through the Corporate Bond Purchase Scheme (CBPS)[30] — partly with the aim of discretionally favouring “green assets” — total purchases were limited to just under £20 billion and began to unwind in September 2022.[31] Targeting corporate “green bonds” purchases and adopting a monetary policy of permanent lower interest rates — the “euthanasia of the rentier” as championed by Keynes in the final chapter of his General Theory[32] — would ease overall lending costs and stand as central features of the Bank’s role within a green planning framework. Lower interest rates would also reduce government borrowing costs, thereby creating greater fiscal space for additional public investment.

Under a green planning framework, these institutions would be responsible for a range of cross-cutting functions: preparing the overall plan and coordinating its implementation, financing the related investment initiatives and enabling the conditions for its delivery.

Specifically, they could play the following related roles:

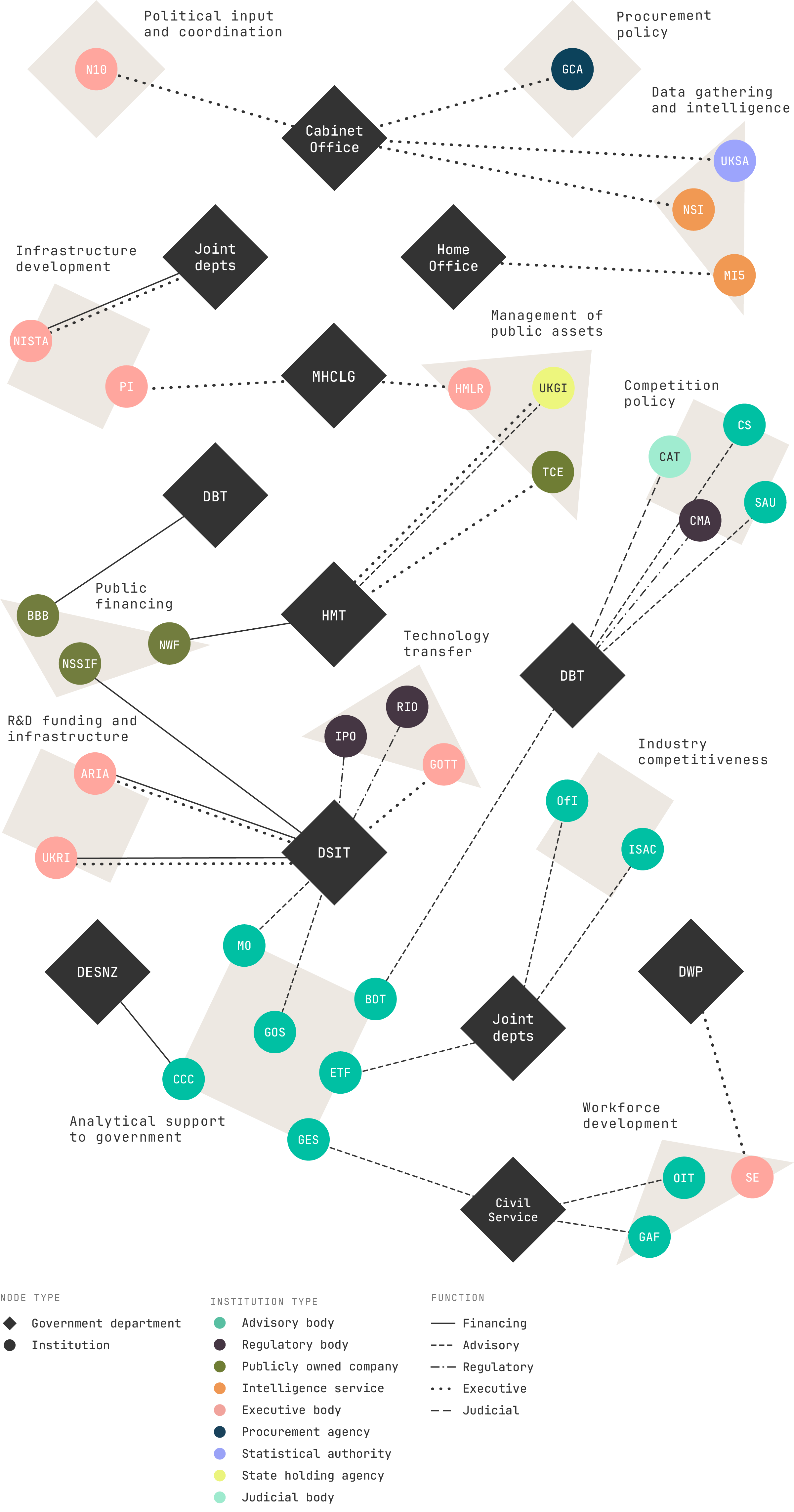

The landscape of cross-cutting institutions is varied, spanning the Civil Service and nine ministerial departments (with joint-units): the Cabinet Office, the Home Office, HM Treasury, the Department for Business and Trade (DBT), the Department for Science, Innovation & Technology (DSIT), the Department for Energy Security and Net Zero (DESNZ) and the Department for Work and Pensions (DWP).

[.fig]Figure 4: Cross-cutting Institutions[.fig]

[.notes]Source: Author’s analysis.[.notes]

The Cabinet Office — with its direct political emanation in the Prime Minister’s Office — oversees entities of various kinds. Data-gathering and intelligence institutions — respectively the UK Statistics Authorities (supervising the Office for National Statistics, ONS) and National Security and Intelligence — fall under the Cabinet Office, unlike the Security Service (MI5), which collaborates with the Home Office. The Cabinet Office also sponsors the UK’s central public procurement body — the newly-established Government Commercial Agency (CGA).

HMT oversees the key institutions for green planning operating at the cross-cutting level: the National Wealth Fund (NWF), UK Government Investment (UKGI) and The Crown Estate (TCE).

The National Wealth Fund (NWF) was created in 2024 from the renaming and repurposing of the previous UK Infrastructure Bank (UKIB), itself established in 2021 to substitute for the role the European Investment Bank (EIB) had played in the UK before Brexit. Although smaller in scale than comparable public financing institutions across Europe,[38] the NWF is the UK’s largest policy bank operating domestically, with £27.8 billion of allocated capital. It provides finance to UK businesses through loans, guarantees and equity instruments. The NWF has a distinct mandate to support the government’s Industrial Strategy, focusing also on clean energy.[39]

UK Government Investment (UKGI) is the holding entity that acts as “shareholder representative” on behalf of the UK government for its publicly owned companies. UKGI’s portfolio covers 26 organisations — including several of the institutions surveyed here (e.g. NWF, GB Energy, NESO, GBR, UKEF, etc.) — on behalf of nine government departments, employing over 109,000 people and generating around £25 billion of gross income.[40] UKGI monitors the performance of these assets through agreed key performance indicators (KPIs). While it does not set policy priorities for the companies in its portfolio, it engages with senior management and appoints a UKGI executive to the board of wholly owned companies.

Finally, HMT works with The Crown Estate (TCE), the public corporation in charge of managing the portfolio of public buildings, land, seabed and other areas of the UK territory. Due to the relevance of space and land costs in clean energy development projects, TCE plays a key role in facilitating investment initiatives — both onshore and offshore. For this reason, TCE entered into a partnership with GB Energy (see section below) on the day its establishment bill was introduced.[41]

In the domestic context, DBT is responsible for driving economic growth by delivering on the new Industrial Strategy.[42] To this end, it is advised by the newly established Industrial Strategy Advisory Council (ISAC) — jointly sponsored with HMT — and by the Board of Trade, though the latter has met only once per year since 2023 and ceased producing reports at the end of 2022.

DBT has one direct policy instrument in the form of the British Business Bank (BBB), a publicly owned bank specialised in providing financing to smaller businesses (SMEs), with invested assets of just under £4.7 billion 2024/25.[43] The BBB currently operates under a broad cross-sectoral mandate with no discretional focus on green sectors, with the exception of a recently launched pilot guarantee scheme for green assets (Green GGS).

DBT also holds responsibility for competition policy through the Competition and Markets Authority (CMA) — and its advisory body, the Subsidy Advice Unit (SAU) — alongside other supporting entities, namely the Competition Appeal Tribunal (CAT) and the Competition Service (CS).

DSIT promotes research and technological innovation principally through UK Research and Innovation (UKRI), the central institution for innovation policy in the UK, with an allocated budget of £8.8 billion in 2025/26.[44] UKRI operates primarily by allocating grants to R&D projects, but also through procurement programmes such as “Contracts for Innovation”, run by its subsidiary Innovate UK. Additionally, UKRI funds the Catapult Network, a national R&D infrastructure for technology transfer in specific areas (see sectoral institutions below). A separate but considerably smaller entity, Advanced Research and Invention Agency (ARIA), with £184 million allocated in 2025/26, was established in 2023, to fund breakthrough R&D in underexplored and more innovative areas.

DSIT oversees public financing instruments, such as the National Security Strategic Investment Fund (NSSIF), a deep-tech venture capital fund owned by British Technology Investments — the corporate venturing arm of the BBB.

Further executive agencies under DSIT are involved in technology transfer (Government Office for Technology Transfer, GOTT) and the provision of weather and climate-related services (Met Office). DSIT also supervises regulatory agencies dealing with intellectual property rights (Intellectual Property Office, IPO) and the commercialisation of new technologies (Regulatory Innovation Office, RIO).

The Government Office for Science (GO-Science), a DSIT advisory body, provides advice to the Cabinet Office and the Prime Minister on science-related decisions.

The MHCLG institutions most relevant to green planning are the Planning Inspectorate and HM Land Registry.

The Planning Inspectorate is an executive agency that deals with “planning”, as currently understood within the work of Local Planning Authorities, primarily in relation to urban and infrastructure development. Crucially, it provides the application process for Nationally Significant Infrastructure Projects (NSIPs),[45] including new power generating facilities.

The HM Land Registry records transactions on property covering more than 90 per cent of land mass of England and Wales, valued at around £9 trillion. It plays a critical administrative role in any transfer of land ownership, including for commercial activities.

Cross-cutting institutions also include the DESZN-sponsored Committee of Climate Change (CCC), which advises the government on emissions targets and reports to Parliament on the progress in greenhouse gas emission reduction.

DWP sponsors an executive agency, Skills England, which focuses on identifying and addressing skill gaps in the economy, working in partnership with employers across England.

The Cabinet Office works closely with HMT, sharing oversight of advisory bodies and executive agencies such as the Evaluation Task Force (ETF) and the Office for Investment (OfI) — the latter formally part of DBT. The OfI is responsible for attracting “transformational” investment across the UK.

The Cabinet Office and HMT also collaborate through the National Infrastructure and Service Transformation Authority (NISTA), which supports government departments in delivering major strategic infrastructure projects.

Several specialised units within the Civil Service perform advisory functions across ministerial departments. The Open Innovation Team operates as an in-house consultancy for civil servants seeking external advice. Analytical support across ministerial departments is provided by the Government Analysis Function and by the Government Economic Service (GES).

The list of cross-sectoral institutions with a potential role in green planning is extensive, though the vast majority are confined to regulatory and advisory functions. Only a few have the capacity to initiate and deliver funded operations at scale — most notably The Crown Estate. Other exceptions include executive bodies within the innovation and environmental clusters.

In other cases, institutions lack the resources to achieve transformational impact. For instance, Government Commercial Agency (GCA) — formerly the Crown Commercial Service (CCS) — handles only a limited share of overall government procurement: £30.3 billion out of £340.9 billion total public sector procurement in 2023/24.[46]

HMT dominates key institutions, leaving limited scope for non-financial policy mandates

The relegation of the key cross-cutting institutions — The Crown Estate, UKGI and the NWF — under the sole control of HMT is problematic within the current fiscal framework centred on strict budgetary discipline.

In several European countries, the finance ministries are the ultimate controlling authorities of state property holdings, industrial asset-holding entities and state investment banks — though other policy interests are also institutionally represented. For instance, Germany’s gargantuan public investment bank, KfW, is jointly supervised by the Federal Ministry of Finance and the Federal Ministry for Economic Affairs and Energy.[47] In France, a “super” Ministry of the Economy — with responsibility for finance, industry and energy policy — oversees the largest state-holding entity in Europe, the Agence des participations de l’État (APE). APE does not only “act as a shareholder representative” for France’s publicly owned companies, it “embodies and carries out the missions of the shareholding State”, including energy independence and decarbonisation.[48]

Ultimately, sharing oversight of key public financing and state-holding bodies across multiple ministerial departments would help ensure that these institutions are aligned not only with fiscal priorities but also with the broader industrial and energy policy objectives of the “green plan”.

Only a few institutions operate across departmental boundaries on cross-cutting issues. These are the advisory bodies linked to the Civil Service and four other joint units: OfI (HMT, N10 and DBT), ETF (HMT and Cabinet Office), NISTA (HMT and Cabinet Office) and ISAC (HMT and DBT). The remainder are currently centred on delivering a sector-specific or even institution-specific mandates.

Although misleadingly focused on “growth” rather than on solving specific challenges,[49] the mission-oriented model of policymaking embraced by the current Labour government should entail a degree of cross-departmental coordination. Yet no formal mechanism aligns public institutions around shared actions. This is partly explained by the absence of a superior coordinating entity responsible for overseeing the implementation of the missions.

The Government Commercial Agency (GCA) operates without a green procurement focus, despite the leverage that such a demand-side policy tool could exert on domestic clean energy supply chains. Competition institutions — and the legislation governing them — leave little room for discretionary public support or the creation of dominant national champions through strategic mergers, even where these would be instrumental in building domestic manufacturing capacity in clean energy. National planning institutions, meanwhile, operate under an adversarial model in which new infrastructure proposals must clear excessively defensive hurdles before approval.[50]

Under a green planning framework, these institutions would be directly involved in delivering the overall objectives of the plan. Given their specific areas of activity, their contribution would vary according to sector and type of entity.

Specifically, these institutions would be responsible for:

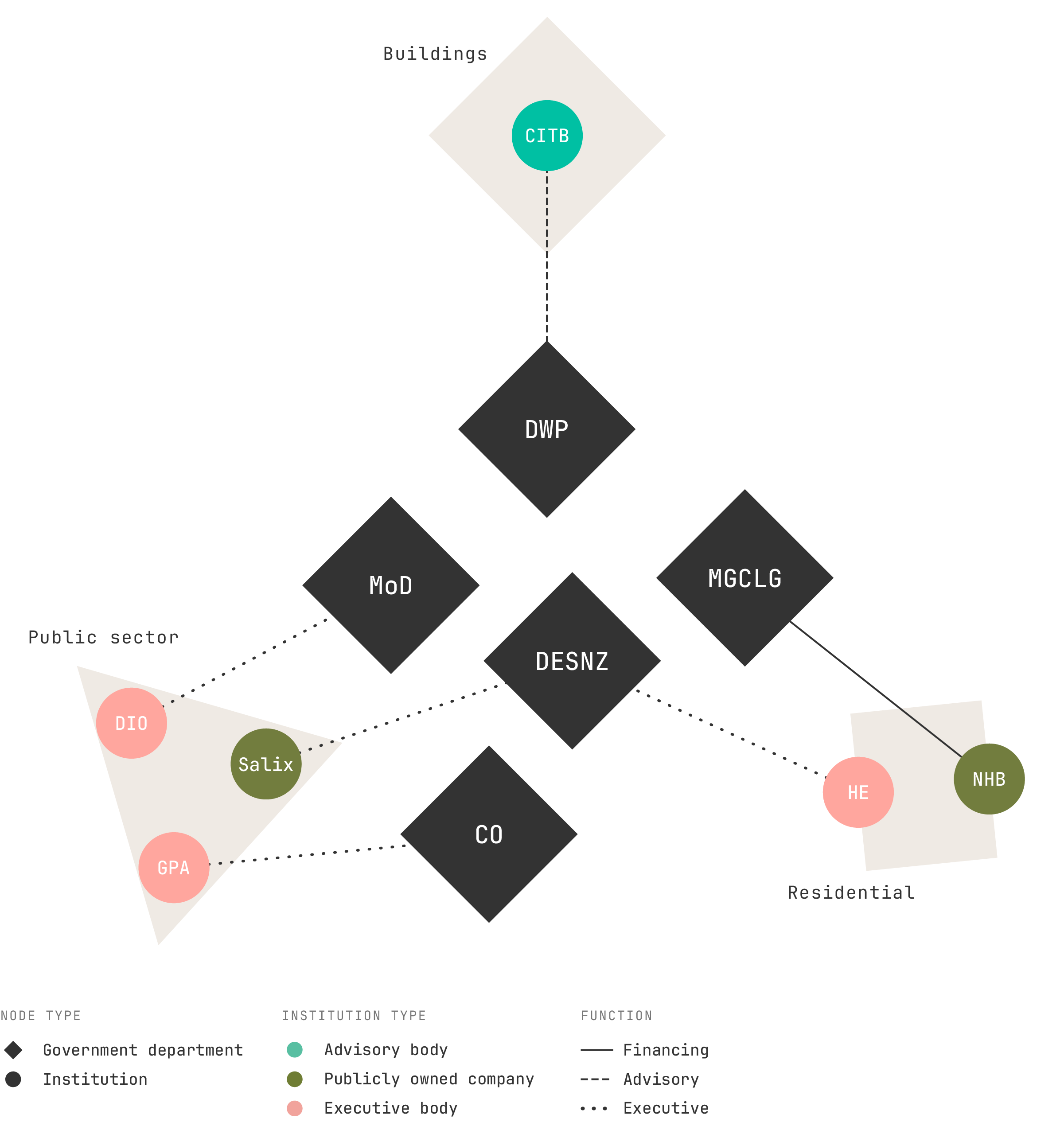

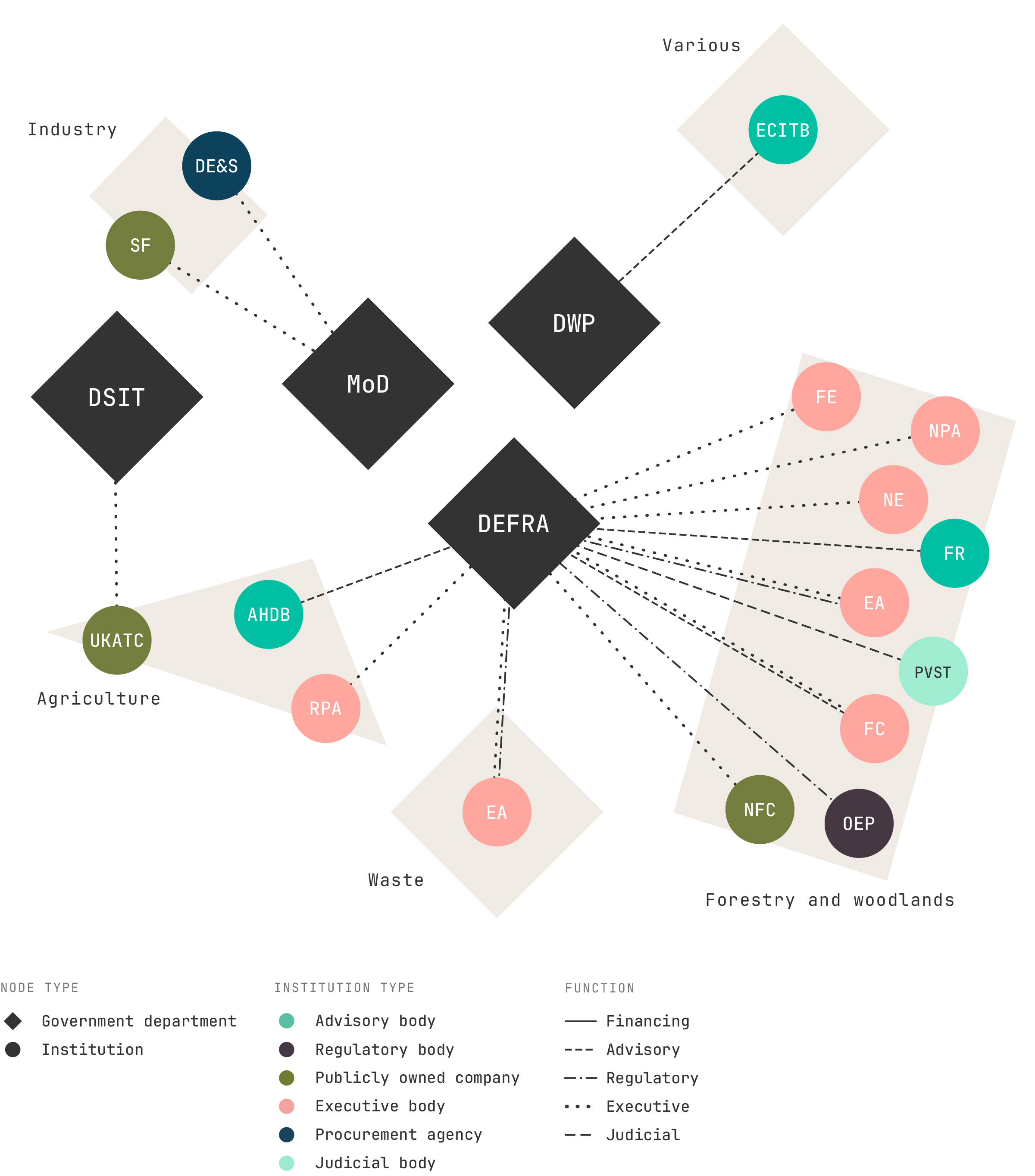

The great majority of sectoral green planning institutions operate under the auspices of the Department for Energy Security and Net Zero (DESNZ) and the Department for Transport (DfT). The former oversees the decarbonisation of electricity supply, while the latter holds responsibility for sustainable mobility and transport infrastructure. The decarbonisation of residential buildings falls under the Ministry of Housing, Communities and Local Government (MHCLG), while institutions operating within the Cabinet Office cover public sector buildings, which account for 11 per cent of total emissions in buildings. The Department for Environment, Food and Rural Affairs (DEFRA) is responsible for agriculture and waste. The Ministry of Defence (MoD) accounts for the largest share of emissions within the public sector, with decarbonisation responsibilities spanning multiple areas. The Department for Work and Pensions (DWP) sponsors institutions that promote sectoral decarbonisation skills. Beyond these departments, a group of sectoral Catapults — which fall under UKRI, sponsored by DSIT — form a further set of relevant bodies. Notably, the Department for Business and Trade (DBT) has no significant sectoral institution of its own that is directly involved in decarbonisation.

[.fig][.fig-title]Figure 5: Sectoral Institutions[.fig-title][.fig-subtitle]ENERGY[.fig-subtitle][.fig]

[.fig][.fig-subtitle]TRANSPORT[.fig-subtitle][.fig]

[.fig][.fig-subtitle]BUILDINGS[.fig-subtitle][.fig]

[.fig][.fig-subtitle]OTHER[.fig-subtitle][.fig]

[.notes]Source: Author’s analysis.[.notes]

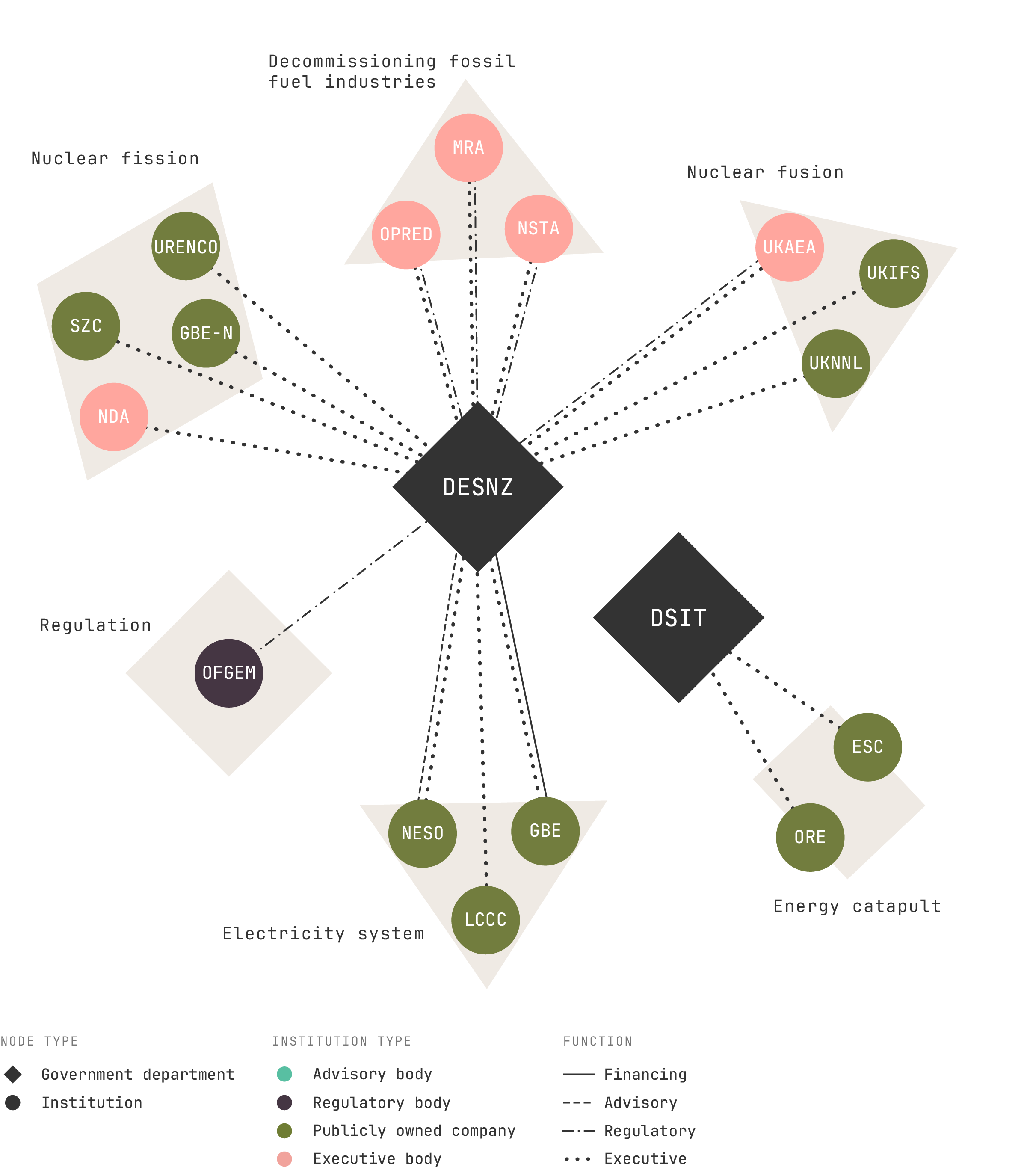

DESNZ collaborates with a range of institutions operating across different areas: nuclear fission, nuclear fusion, electricity system, energy efficiency, fossil fuel decommissioning and regulation of the energy system.

Nuclear fission. DESNZ sponsors GB Energy — Nuclear (GBE-N), a project developer for new nuclear initiatives, focused on Small Modular Reactor (SMR) technology. The department holds significant stakes in two companies operating in the sector: Sizewell C (45 per cent government-owned), which is responsible for constructing the UK’s largest nuclear power plant (3.2 GW of nameplate capacity) in Suffolk; and Urenco (33 per cent government-owned), which supplies uranium enrichment services and fuel cycle products. The decommissioning of closed nuclear power falls under the remit of the Nuclear Decommissioning Authority (NDA).

Nuclear fusion. DESNZ supports nuclear fusion projects through the UK Atomic Energy Authority (UKAEA), which is responsible for research and delivery in the field, including through UKAEA’s subsidiary UK industrial Fusions Solutions (UKIFS), a company leading the designing and building of the UK’s first prototype fusion energy plant. DESNZ also has a role in nuclear fusion research and innovation — external to DSIT’s orbit — through the United Kingdom National Nuclear Laboratory (UKNNL), a public corporation.

Electricity system. Beyond nuclear power, the UK government has only recently reintroduced publicly owned policy levers to intervene in the broader electricity sector, after the full privatisation that took place following the Electricity Act 1989. The first such instrument is the Low Carbon Contracts Company (LCCC), a company wholly owned by DESNZ and funded by a compulsory levy on all licensed electricity suppliers in Great Britain. LCCC was established in 2014 to manage contracts with low-carbon electricity generators under the price-fixing mechanism known as Contracts for Difference (CfD). The LCCC is also responsible — via the Electricity Settlements Company (ESC) — for managing all financial transactions and associated settlement functions under the Capacity Market (CM). Second, following the Energy Act 2023, the National Energy System Operator (NESO) was created in 2024 as a public corporation, through the spin-off of the electricity system operator function previously performed by National Grid — Great Britain's private owner of the electricity transmission network. NESO was subsequently assigned responsibility for planning future electricity and gas networks, as well as advisory functions relating to net zero objectives. The most recent development in the electricity sector is GB Energy, the publicly owned energy company established by the Labour Government in 2025 with a capital endowment of £8.3 billion over the current parliament. GB Energy was conceived primarily as a developer and operator of clean energy generation assets.[51] Its other mandates include the promotion of local and community energy projects under the Local Power Plan (LPP), and support for domestic clean energy manufacturing.

Energy efficiency of public sector buildings. Through its wholly owned company Salix Finance, DESNZ currently delivers funding for energy efficiency improvements and emissions reduction across public sector entities. In 2024-25, Salix Finance awarded grants for a total value of £4.6 billion.[52] From 2027, a new executive agency — the Warm Homes Agency (WHA) — will assume cross-cutting responsibilities for energy efficiency and building decarbonisation, consolidating Salix Finance and selected functions of the energy regulator, Ofgem (see below).

Decommissioning of fossil fuel industries. DESNZ oversees the decommissioning of fossil fuel industries in the UK through three bodies: the North Sea Transition Authority (NSTA), the Mining Remediation Authority and the Offshore Petroleum Regulator for Environment and Decommissioning (OPRED).

Regulation of the energy system. The Office of Gas and Electricity Markets (Ofgem) was established in 2000 through the merger of Offer (the Office of Electricity Regulation) and Ofgas (the Office of Gas Supply) — the two sectoral regulators originally established at the time of privatisation. Ofgem is the licensing authority for the energy sector; it regulates the monopoly companies that run the gas and electricity networks, sets caps on domestic energy bills and supports industries in meeting their environmental obligations.

Institutions supervised by the Department for Transport (DfT) cover the three main modes of domestic transport: rail, road and air.

Rail transport: in this area, DfT operates through publicly owned companies such as High Speed Two (HS2) Limited and East West Railway Company Limited to develop new railway lines. Great Britain’s railway infrastructure is managed by Network Rail, an executive non-departmental public body, soon set to become a subsidiary of the future publicly owned Great British Railways (GBR). GBR will also incorporate DfT Operator, a public corporation acting as a holding company for government-owned train service operators. DfT Operator effectively functions as a “nationalising” agency on behalf of the future GBR, with ten major rail operators already under its control (as of April 2026) and a further six still to be added by 2027, when GBR will be fully established. GBR will bring passenger services, infrastructure provision, network management, fares and ticketing into a single organisation — though it will not own rolling stock, which will continue to be leased from privately-owned Rolling Stock Companies (ROSCOs), nor will it operate all passenger services, since open-access operators will continue to run trains alongside it.[53] Freight operators will remain entirely private, though GBR will have a statutory duty to promote rail freight.

Road transport: DfT manages England's network of motorways and major A-roads through National Highways, an executive non-departmental public body responsible for the planning, construction and maintenance of that network. A DfT tribunal, the Traffic Commissioners for Great Britain, oversees the licensing and regulation of operators of heavy goods vehicles, buses and coaches and the registration of local bus services.

Air transport: the principal national public institution operating in the field of air transport is the Civil Aviation Authority (CAA), a public corporation in charge of regulating aviation safety, airspace use and major UK airports.

Others: Active Travel England, an executive agency, promotes walking, wheeling and cycling as the preferred modes of transport across England. Responsibility for the regulation of rail and road lies with the Office of Rail and Road (ORR) and will remain so even after GBR is fully established.

Residential Buildings. Homes England, an executive non-departmental public body sponsored by MHCLG, serves as the government's main agency for housebuilding and housing regeneration. Its primary instrument is grant funding for affordable housing delivery, which totalled £3.29 billion in 2024/25.[54] Homes England is expected to provide £30 billion grants over the next decade. Since November 2025, this has been complemented by the National Housing Bank — a public financing institution wholly owned by Homes England, supporting housing delivery through debt, equity and guarantee instruments, with an anticipated deployment of £16 billion over the same period.[55]

Public sector buildings. The Government Property Agency (GPA), a Cabinet Office executive agency, is the largest owner of public sector buildings and therefore bears major responsibility for their decarbonisation. Given its extensive property portfolio, the GPA could play a direct role in decarbonising the energy use of public sector buildings — which account for 10.9 per cent of total emissions in the buildings sector. To that end, the GPA has launched a Net Zero Programme, investing in energy measures across its portfolio, primarily through the installation of on-site solar panels.

The most significant DEFRA institution is the Environment Agency, with over 13,000 employees and a £2.3 billion budget in 2025. Founded in 1996, it covers a wide range of statutory duties relating to the protection of the environment, the regulation of industry and waste management, water quality, inland navigation, conservation and others.

Agriculture. DEFRA implements its agricultural policy primarily through the Rural Payments Agency (RPA), an executive agency responsible for distributing over £2 billion in subsidies to support England's farming and rural communities. Research, market intelligence and promotional activity aimed at helping British farmers improve performance and develop their markets are carried out by the Agriculture and Horticulture Development Board, a DEFRA-sponsored executive non-departmental public body.

Waste. At the national level, the Environment Agency serves as the principal waste regulator — enforcing waste management legislation, licensing waste sites and carriers and advising both government and businesses on waste management practices. Operational waste collection and disposal remain the responsibility of local authorities.

Land use and forestry. DEFRA operates through various specialised institutions at the local level, including the ten National Parks in England, each supervised by a park authority, and the National Forest Company (NFC), a DEFRA-owned company involved in reforestation across the Midlands. An executive non departmental public body, Natural England, is responsible for the conservation and restoration of the natural environment. DEFRA also supports the creation and management of woodlands through executive agencies working with the Forestry Commission, a non-ministerial department. These are Forestry England, the country's largest land and tree manager, and Forest Research, the main research organisation in Great Britain on forestry matters. A regulatory agency, the Office for Environment Protection (OEP), holds the government and other public authorities to account on environmental matters. Lastly, the Plant Varieties and Seeds Tribunal (PVST), a judicial body of DEFRA, establishes legally binding rules regarding the national registration of new plant varieties, UK plant variety rights and selected forestry issues.

Military decarbonisation. The British Armed Forces are responsible for 50 per cent of UK central government CO2 emissions and one per cent of total UK emissions.[56] The majority of these arise from military aviation, naval operations and energy use in military buildings. The MoD operates through two institutions with a direct bearing on the military carbon footprint: the Defence Equipment and Support (DE&S), which oversees military procurement and logistics, and Defence Infrastructure Operation (DIO), which is responsible for the construction and maintenance of military buildings.

Industry decarbonisation. The MoD also plays an indirect role in industrial decarbonisation through Sheffield Forgemasters, a public corporation that produces, among other things, specialised steel products for military applications.

Sectoral decarbonisation skills. The Department for Work & Pensions (DWP) sponsors two sectoral training entities — the Construction Industry Training Board (CITB) and the Engineering Construction Industry Training Board (ECITB) — working with employers and companies to develop the technical skills of workers in the construction and engineering construction industries respectively.

Road transport. The Office for Zero Emission Vehicles (OZEV), a joint unit of DESNZ and DfT, supports the uptake of plug-in vehicles and funds the rollout of charge point infrastructure across the UK.

Research and innovation in sectoral decarbonisation. The Catapult Network is a public R&D infrastructure comprising specialist centres focused on different sectoral research areas. The Offshore Renewable Energy Catapult is the UK's leading centre for research and technological innovation in offshore renewable energy. The Energy Systems Catapult focuses on energy innovation for businesses, buildings and energy networks. The Connected Places Catapult promotes innovation in transport and construction, with a particular emphasis on decarbonisation. Lastly, UK Agri-Tech Centre serves as the national hub for the development and adoption of agri-tech innovation.

If adequately funded and managed, GBR could play a significant role in transport decarbonisation — both by substituting for journeys made by private vehicles and by electrifying railway lines. Electrification currently extends to only 39 per cent of total route length, though 70 per cent of the 15,348 railway vehicles for passenger are electric,[57] and electric trains account for a substantially higher share of passenger journeys given their greater speed and capacity. GBR could also serve as the demand coordinator of an integrated supply chain spanning rail tracks, signalling systems and rolling stock — if permitted to own them.[58]

There is, however, no equivalent of GBR for buses — despite one having existed between 1969 and 1988 in the form of the publicly owned National Bus Company (covering England and Wales) and the Scottish Bus Group (operating in Scotland). Under a green planning approach, a national bus company could foster public transport use, reducing dependence on private vehicles and the emissions associated with them. At the same time, it could become a demand-side instrument for promoting domestic manufacturing of electric buses, much as Chinese publicly owned local bus companies deliberately did in the mid-2010s.[59]

At present, the decarbonisation of road transport is left largely to individual passengers — through the adoption of electric vehicles, supported by funding schemes for private purchasers and by private-sector charging infrastructure. No public institution coordinates this transition with the UK automotive supply chain, raising the risk that domestic manufacturing capacity will be eroded in favour of imported EVs.[60]

Virtually no public institutions operate in air transport, with the exception of the regulatory body — the CAA. All major UK airports are privately-owned, save for Manchester, London Stansted and East Midlands — all owned by the Manchester Airports Group.[61] This contrasts with other countries, such as France and especially Germany, where central and local governments are often the controlling shareholders. Since the privatisation of British Airways in 1987, the UK has also had no publicly owned airline, whereas public ownership of flag carriers remains common worldwide, including in Portugal, Finland, France, Italy, Poland and elsewhere across Europe.

Since housing is a devolved matter, Westminster-controlled public institutions such as Homes England operate only in England. Even government funding programmes for installation of residential heat pumps — such as the Boiler Upgrade Scheme and the Social Housing Decarbonisation Fund — are limited to England and Wales.[62] In the absence of coordination and common standards, the proliferation of institutions and funding schemes could hinder the ability of specialised businesses to deliver building and renovation projects efficiently across the UK.[63]

More significant still is the fragmentation of institutions and policies around residential decarbonisation. At present, Homes England's contribution to decarbonisation comes primarily through the energy performance standards it sets for the homes it funds and the land it develops, rather than through retrofit grants. Retrofit funding — including for heat pump installations — is managed by DESNZ and is expected to be delivered by the Warm Homes Agency (WHA), the new public body due to be established in 2027, as part of the £15 billion Warm Homes Plan.[64]

The decarbonisation of public sector buildings is hampered by a similar dispersion of responsibilities across separate entities and ministerial departments. DESNZ runs the Public Sector Decarbonisation Scheme through Salix Finance, though this function will be consolidated into the WHA upon its creation. Civil government buildings fall under the Cabinet Office through the GPA, while military buildings are managed separately by the Ministry of Defence through the DIO. Greater centralisation and coordination would be essential for executing future decarbonisation plans at scale.

Only a limited number of public institutions are involved in the decarbonisation of the agricultural sector, despite accounting for the third-largest share of national emissions. Moreover, those that do exist lack a distinct decarbonisation mandate and are inadequately funded to deliver one.

Measured against the scale of investment and reform needed to transition the electricity sector, the newly introduced public entities remain blunt weapons. Notably, NESO elaborates plans for energy generation, transmission grids and distribution networks — respectively the Strategic Spatial Energy Plan (SSEP), the Centralised Strategic Network Plan (CSNP) and various Regional Energy Strategic Plans (RESPs). But the fulfilment of those blueprints remains largely in private — mostly foreign — and fragmented hands, which operate pursuing primarily their own individual financial interests.[65] GB Energy will remain a marginal player, given its small financial scale and its exclusion from operating in the retail segment.[66]

Moreover, the recent introduction of new public entities — with distinct policy responsibilities — has increased the fragmentation of the electricity sector, hampering efforts towards a more efficient centralisation of policymaking in this field. In the end, an electricity system dominated by the financial interests of privately owned players is difficult to reconcile with the imperatives of higher investment in renewable capacity and lower energy costs.[67]

The most recent comprehensive Industrial Decarbonisation Strategy was published in March 2021 by what was then the Department for Business, Energy & Industrial Strategy (BEIS), before it was split into DESNZ and DBT.[68] The current division of roles between the two departments regarding industry decarbonisation remains unclear. DESNZ is responsible for the Carbon Budget and Growth Delivery Plan[69] and oversees major funding initiatives for investment in carbon capture, usage and storage (CCUS) projects ultimately aimed at decarbonising cement and lime production.[70] DBT, meanwhile, has recently launched The UK Steel Strategy, which sets out provisions for the transition to green steel.[71]

Both departments, however, confine themselves to designing sector-specific decarbonisation strategies and allocating funds to businesses, without operating through any dedicated institution to drive industry decarbonisation. The only public body directly involved in this area is Sheffield Forgemasters, the MoD-sponsored steelmaking company.

The UK has established a set of decommissioning institutions — the NSTA, OPRED and the Mining Remediation Authority — capable of coordinating the phase-out of fossil fuel supply and its associated emissions. The pace and scope of that phase-out, however, depends fundamentally on the objectives and provisions set out in a future green plan.

A first-order problem is the replication of environmental regulatory agencies across the UK: the DEFRA-sponsored Environment Agency operates only in England, with equivalent bodies in Wales (Natural Resources Wales), Scotland (the Scottish Environment Protection Agency) and Northern Ireland (the Northern Ireland Environment Agency). Under a green planning framework, regulatory standards and waste management practices should be aligned across these jurisdictions. Similarly, an overarching plan could foster coordination between national agencies and local authorities responsible for operating waste collection and disposal facilities.

The current architecture of UK public institutions is ill-suited to effective green planning. The mapping exercise performed in previous chapters brings to light a series of structural weaknesses that will need to be addressed.

The current planning architecture suffers from a high degree of compartmentalisation, with each institution pursuing its own mandate with little cross-departmental coordination to bring them together. One example is the support to clean energy supply chains, which sits formally within the DBT's industrial policy remit but is also pursued by the HMT-controlled NWF and by DESNZ — through GB Energy’s supply chain mandate. In other cases, responsibilities overlap directly. For instance, through UKRI, DSIT oversees innovation and research policy — including on clean energy technologies — yet DESNZ retains separate responsibility for nuclear research and innovation.

Green planning will entail a broader scope of policy analysis and design, together with a clear indication of objectives and of what different actors — institutions and individuals — are expected to do. Past and current examples consistently show that this requires the introduction of a unitary authority: what Nobel Prize-winning economist Jan Tinbergen called a “Central Planning Bureau (CPB)”.[72]

In the future UK green planning system, such an entity should be responsible for drafting the plan, and for coordinating the actors involved in its implementation. This planning authority could be jointly supervised by representatives from key ministerial departments.

In the UK, there are three different ways of classifying public bodies that in other countries would simply be called state-owned enterprises (SOEs) — namely joint-stock companies in which the public sector holds a majority or controlling stake.[73] These are: public corporations, companies wholly owned by the government and non-departmental public bodies (NDPBs). The NDPB classification can also apply to executive agencies and even advisory bodies. The NWF exemplifies this confusion of legal status — formally registered as a “private limited company wholly-owned by HMT”, it is nonetheless classified as an NDPB dependent on HMT.

These SOEs are owned or “sponsored” by sectoral ministerial departments and related entities, but the “shareholding function” for most of them is exercised by UKGI, the HMT-controlled holding company. This creates institutional ambiguity over the governance arrangements between public bodies and their controlling entities, with potentially negative consequences for the discharge of their policy responsibilities. In other European countries, SOEs are managed either by a state holding entity or directly by the ministerial department that owns them.

Among comparable public financing institutions, the NWF is several times smaller than the national promotional banks of Germany (KfW), France (Caisse des Dépôts) and Italy (Cassa Depositi e Prestiti). Similarly, the BBB’s total lending activity to SMEs is a fraction of the volumes managed by France’s BPIFrance or KfW’s SME subsidiary.

The same holds true for non-financial corporations. GB Energy will remain a marginal player in electricity generation, having been established as a start-up company rather than through the nationalisation of existing generation and infrastructure assets. Equally, GBR is unlikely to match the systemic scale of long-established vertically integrated rail groups across Europe — such as SNCF (France), DB (Germany), or FS (Italy).

This makes UK publicly owned entities less likely to play a decisive role in green planning, even under a more explicit policy mandate.

The capacity of executive publicly owned entities in the UK — even those with a commercial nature — to achieve a decisive scale is limited by the consolidation of their financial accounts within the government budget. This prevents them from expanding their borrowing to increase investment (in the case of GB Energy or GBR) or lending (in the case of the NWF), even where they would be perfectly able to repay their obligations from generated revenues.

These accounting conventions represent a UK anomaly.[74] In Germany, KfW finances its lending operations primarily through state-guaranteed bond issuance, enjoying a sovereign (AAA) credit rating. In France, EDF — the country's electricity giant — weighs on the government budget only in the case of one-off capital injections.[75] EDF’s borrowing to finance ongoing operations and capital expenditure is kept off the government's balance sheet, while its state-owned status allows it to borrow at a marginal premium over France's sovereign rating.

The UK still lacks meaningful public ownership in commercial companies operating in areas central to green planning — energy networks, transport infrastructure and services and clean technology manufacturing.

By way of comparison, through its state holding agency, the French government controls major companies across the energy sector (EDF, Engie, the electricity transmission grid RTE), several airports, the largest ports, the public transport company RATP, the airline Air France-KLM and even the car manufacturer Renault. This does not mean that these companies currently operate within the framework of an explicit green plan, but the French government already works through them to achieve non-financial policy objectives.

Several Westminster-controlled entities — such as Skills England (of DWP), National Highways (of DfT), Homes England (of MHCLG) and Forestry England (of DEFRA) — only operate in England, while the other UK nations maintain parallel bodies and initiatives. The future GBR is expected either to establish a distinct Scottish subsidiary or to coordinate separately with ScotRail. Scotland also has its own public investment institution, the Scottish National Investment Bank (SNIB). Major cities — such as London and Manchester — run their local transport systems through publicly owned bodies. similar model could emerge in the energy sector if municipally owned energy companies are established, following the German example of “re-municipalisation”.[76]

Future green planning will need to consider how to align subnational administrative levels and their associated public institutions — otherwise, significant parts of the UK risk being left out, weakening the overall impact of policy.

Green planning will entail a broader scope of policy analysis and design, together with a clear indication of objectives and on what different actors — institutions and individuals — should do. But it will also need reforms to address weaknesses in the current institutional architecture. This will imply the repurposing of existing institutions and the establishment of missing ones where critical gaps remain — including, crucially, a central planning entity. Without such reforms, any green plan risks remaining a dead letter.

Lessons on how to design an effective green planning architecture can be drawn from contemporary examples of comprehensive planning as well as from past planning experiences, including those of the UK itself.

Green planning institutions have been classified according to the following defining features:

[.fig]Table A1: UK international institutions for green planning[.fig]

[.fig]Table A2: UK macro-financial institutions for green planning[.fig]

[.fig]Table A3: UK cross-cutting institutions for green planning[.fig]

[.fig]Table A4: UK sectoral institutions for green planning[.fig]

[1] John Maynard Keynes, The Collected Writings of John Maynard Keynes, Volume XXI: Activities 1931–1939: World Crises and Policies in Britain and America, edited by Donald Moggridge, Cambridge University Press, 2013, p. 91.

[2] George Douglas Howard Cole, Principles of Economic Planning, Macmillan and Co., 1935; Lionel Robbins, Economic Planning and International Order, Macmillan and Co., 1937.

[3] Alec Cairncross, The British Economy Since 1945: Economic Policy and Performance, 1945–90, Blackwell, 1992; Geoffrey Denton, Murray Forsyth and Malcolm Maclennan, Economic Planning and Policies in Britain, France and Germany, Allen and Unwin, 1968; Stuart Holland (ed.), Beyond Capitalist Planning, Blackwell, 1978; Andrew Shonfield, Modern Capitalism: The Changing Balance of Public and Private Power, Oxford University Press, 1965.

[4] Charles Hilliard Feinstein (ed.), The Managed Economy: Essays in British Economic Policy and Performance since 1929, Oxford University Press, 1983.

[5] Michael Lawrence, Thomas Homer-Dixon, Scott Janzwood, Johan Rockström, Ortwin Renn and Jonathan F. Donges, “Global polycrisis: the causal mechanisms of crisis entanglement”, Global Sustainability, 2024, vol. 7, e6, pp. 1–16.

[6] “Statistical classification to the public sector”, Office for National Statistics, 2024. Available here; “System of National Accounts 2008”, United Nations, 2008. Available here.

[7] Some of these institutions — most notably the National Health Service (NHS) — were established to discharge planning responsibilities in social policy, while also exerting an implicit influence on the wider economy. This was a central tenet of the Beveridge Report (1942), which tied the creation of the welfare state to the more efficient management of the British economy. Full reference for the Beveridge Report: William Beveridge, Social Insurance and Allied Services, Cmd. 6404, HMSO, 1942.

[8] “Energy Technology Perspectives 2026”, International Energy Agency, 2026. Available here.

[9] Ibid.

[10] Simone Gasperin, Pranesh Narayanan and Sofie Pultz, “Resilient by design: Building secure clean energy supply chains”, Institute for Public Policy Research, 2025. Available here.

[11] “Energy Transition Investment Trends 2026”, BloombergNEF, 2026. Available here.

[12] “Energy Transition Investment Trends 2026: Countries Annex”, BloombergNEF, 2026. Available here.

[13] “Clean Power 2030 Action Plan”, Department for Energy Security and Net Zero, 2024. Available here.

[14] Department for Energy Security and Net Zero (2026) Provisional UK greenhouse gas emissions statistics 2025. “2025 UK greenhouse gas emissions: provisional figures”, Department for Energy Security and Net Zero, 27/03/2026. Available here.

[15] “The electrification imperative”, Ember, 2025. Available here.

[16] “Advancing Clean Technology Manufacturing”, International Energy Agency, 2024. Available here.

[17] DIT was created in 2016, from the non-ministerial department UK Trade & Investment (established in 2003).

[18] UKEF has a standing consent with HMT that provides parameters for fiscal responsibility, including the risk appetite for potential losses that cannot exceed £6 billion for UKEF’s entire portfolio.

[19] "Critical Minerals Supply Finance", UK Export Finance, [undated]. Available here; “Critical Goods Exports Development Guarantee”, UK Export Finance, [undated]. Available here.

[20] “Energy Transition Investment Trends 2026”, BloombergNEF, 2026. Available here.

[21] “Bank of England Act 1998”, legislation.gov.uk. Available here.

[22] “The UK's fiscal targets”, House of Commons Library, 2026. Available here.

[23] “A strong fiscal framework”, HM Treasury, 2024. Available here.

[24] Carl Emmerson and Isabel Stockton, “Public sector net worth as a fiscal target”, Institute for Fiscal Studies, 2023. Available here.

[25] “European System of Accounts: ESA 2010”, Eurostat, 2013. Available here.

[26] “The Office for Budget Responsibility”, House of Commons Library, 2026. Available here.

[27] “The first round of Medium-term fiscal-structural plans”, EU Independent Fiscal Institutions, 2025. Available here.

[28] Alan Taylor, “Getting the right direction”, Bank of England, March 2026. Available here.

[29] Òscar Jordà, Sanjay R. Singh and Alan M. Taylor, “The Long-Run Effects of Monetary Policy”, Federal Reserve Bank of San Francisco Working Paper 2020-01, 2024. Available here.

[30] “Options for greening the Bank of England's Corporate Bond Purchase Scheme”, Bank of England, 2021. Available here.

[31] “Asset Purchase Facility: corporate bond sales programme – Market Notice 6 April 2023”, Bank of England, 06/04/2023. Available here.

[32] John Maynard Keynes, The General Theory of Employment, Interest and Money, Palgrave Macmillan, 1936, p. 376.

[33] Wassily Leontief, “National Economic Planning: Methods and Problems”, Challenge, July/August 1976, vol. 19, no. 3, pp. 6–11.

[34] Brett Christophers, The Price is Wrong: Why Capitalism Won't Save the Planet, Verso Books, 2024; “World Energy Investment 2025”, International Energy Agency, 2025. Available here.

[35] Melanie Brusseler, “Coordinating the Green Prosperity Plan”, Common Wealth, 2023. Available here.

[36] Mariana Mazzucato and Caetano C. R. Penna, “Beyond market failures: the market creating and shaping roles of state investment banks”, Journal of Economic Policy Reform, 2016, vol. 19, no. 4, pp. 305–326.

[37] Sam Alvis, George Dibb, Simone Gasperin and Luke Murphy, “Market making in practice”, Institute for Public Policy Research, 2023. Available here.

[38] Laurie Macfarlane and Mariana Mazzucato, “State investment banks and patient finance: An international comparison”, University College London Institute for Innovation and Public Purpose Working Paper 2018-01, 2018. Available here.

[39] “Unlocking the UK's Future: our Five-Year Strategic Plan to 30/31”, National Wealth Fund, 2026. Available here.

[40] “UKGI Stewardship Code Report”, UK Government Investments, 28/01/2026. Available here; “Corporate Governance”, UK Government Investments, [undated]. Available here.

[41] “New Great British Energy partnership launched to turbocharge energy independence”, Department for Energy Security and Net Zero, 2024. Available here.

[42] “The UK's Modern Industrial Strategy”, Department for Business and Trade, 2025. Available here.

[43] “Annual Report and Accounts 2025”, British Business Bank, 2025. Available here.

[44] “2025–26 budget allocations for UK Research and Innovation”, UK Research and Innovation, 2025. Available here.

[45] The planning policy framework for Nationally Significant Infrastructure Projects (NSIPs), regarding England and Wales, was established under the Planning Act 2008.

[46] “Crown Commercial Service Annual Report and Accounts 2024/25”, Crown Commercial Service, 2025, Available here; “Procurement statistics: a short guide”, House of Commons Library, 2025. Available here.

[47] “Law Concerning Kreditanstalt für Wiederaufbau / KfW Bylaws”, Kreditanstalt für Wiederaufbau, 2026. Available here.

[48] “Stratégie actionnariale: Notre doctrine”, Agence des participations de l'État, 2026. Available here.

[49] Mariana Mazzucato, Sarah Doyle and Luca Kuehn von Burgsdorff, “Mission-oriented industrial strategy: global insights”, University College London Institute for Innovation and Public Purpose Policy Report 2024/09, 2024. Available here.

[50] Dan Davies, "Build the rail! Save the snails! How to really fix UK infrastructure planning", Labour Together, 2026. Available here.

[51] “Strategic Plan”, Great British Energy, December 2025. Available here.

[52] “Annual report and accounts 2024–2025”, Salix Finance, 2025. Available here.

[53] “Railways Bill factsheet: introducing and designing Great British Railways”, Department for Transport, 2025. Available here; “The future of rail”, House of Commons Library, 2025. Available here; “Open access operators for rail services”, House of Commons Library, 2025. Available here.

[54] “Annual Report and Accounts 2024/25”, Homes England, 2025. Available here.

[55] “Investment Prospectus 2026”, Homes England and National Housing Bank, 2026. Available here.

[56] “Reduce impact of defence on climate change”, Defence Science and Technology Laboratory, 2024. Available here.

[57] “Rail infrastructure and assets April 2024 to March 2025”, Office of Rail and Road, 2025. Available here.

[58] Gareth Dennis, How the Railways Will Fix the Future: Rediscovering the Essential Brilliance of the Iron Road, Repeater Books, 2024; “KNOWING WHAT TO DO? How not to build trains”, Centre for Research on Socio-Cultural Change, [undated]. Available here.

[59] Xiaoying You, “How China's buses shaped the world's EV revolution”, BBC Future, 06/12/2023. Available here.

[60] Simone Gasperin and Pranesh Narayanan, “Planes, trains and automobiles: How green transport can drive manufacturing growth in the UK”, Institute for Public Policy Research, 2025. Available here.

[61] The Manchester Airport Group (MAG) is the UK’s largest airport group, owning and operating Manchester, London Stansted and East Midlands airports. MAG is majority publicly owned by Manchester City Council (35.5%) and by the nine other Greater Manchester local authorities (29%). Another 35.5% is owned by the Australian-based investment fund IFM Global Infrastructure Fund.

[62] Simone Gasperin, Pranesh Narayanan and Joshua Emden, “The heatwave: Unlocking the economic potential of UK heat pump manufacturing”, Institute for Public Policy Research, 2024. Available here.

[63] Mathew Lawrence Pauker and Daniel Brown, “A Plan for Places: Transforming Housing and Lowering the Cost of Living Through Home Improvement Corporations”, Common Wealth, 26/02/2026. Available here.

[64] “Warm Homes Plan”, Department for Energy Security and Net Zero, 2026. Available here.

[65] “Grid is Good: The Case for Public Ownership of Transmission and Distribution”, Common Wealth, 08/10/2023. Available here.

[66] Adam Khan, Melanie Brusseler and Chris Hayes, “Purchasing Power: A Public Option Retail Arm for Great British Energy”, Common Wealth, 05/08/2024, Available here; Stephen Hall, “Retail Reimagined: How Regional Energy Boards Could Deliver a Fair and Flexible Energy System”, Common Wealth, 31/03/2026. Available here; Simone Gasperin and Joseph Evans, “2030 and beyond: Great British Energy's role in the green transition”, Institute for Public Policy Research, 2025. Available here.

[67] “Who Owns Britain? Energy”, Common Wealth, 2025. Available here.

[68] “Industrial Decarbonisation Strategy”, Department for Business, Energy and Industrial Strategy, 2021. Available here.

[69] “Carbon Budget and Growth Delivery Plan (Section 14 Report)”, Department for Energy Security and Net Zero, 2025. Available here.

[70] “Carbon Capture, Usage and Storage: Eighth Report of Session 2024–25”, House of Commons [Committee name], 2025. Available here.

[71] “The UK Steel Strategy”, Department for Business and Trade, 2026. Available here.

[72] Jan Tinbergen, Central Planning, Yale University Press, 1964.

[73] “Classification of public bodies: information and guidance”, Cabinet Office, 2016. Available here.

[74] Thomas Aubrey, “Avoiding the pitfalls of private finance initiatives and departmental budgets to fund the next wave of sustainable new towns and urban extensions”, Bennett Institute for Public Policy, 2024. Available here.

[75] As it was with the recapitalisation, in June 2022, that brought EDF back into 100% public ownership.

[76] Oliver Wagner and Kurt Berlo, “Remunicipalisation and foundation of municipal utilities in the German energy sector: Details about newly established enterprises”, Journal of Sustainable Development of Energy, Water and Environment Systems, 2017, vol. 5, no. 3, pp. 396–407.