As rising global tensions send oil and gas prices soaring, Britain is, once again, on the brink of an energy price crisis. Because of the way British electricity markets work, ordinary people risk paying the price.

Even though gas accounts for about a quarter of electricity in Britain, it sets the electricity price most of the time. This means that cheaper renewables, nuclear and hydro power are given inflated prices — set at that of the higher gas price. This is how companies made billions in windfall profits during the last energy price crisis, while households struggled to heat their homes and businesses scrambled to pay high bills.

The Government and regulators must, therefore, break the link between gas prices and electricity bills. In this briefing, we explain how this could be done. The Government should instruct the National Energy System Operator (NESO) to act as a single buyer of electricity, taking legacy clean power generators out of the wholesale market and paying them fair, fixed prices close to the costs they were built on, and moving gas generating plants to a regulated model that stops crisis profiteering.

If wholesale prices remain around £100 MWh, the single buyer model would save around £67 for an average household over the next 12 months and around £4.7 billion in total, not including the additional savings on payments to gas plants themselves. If wholesale electricity prices stay at closer to £200 MWh, the savings would be nearer to £203 per household, and £14 billion overall.

The model can be implemented quickly, deploying mechanisms that already exist in the energy sector, akin to Contracts for Difference (CfD) to fix prices. It offers a fast way to protect households and a fair approach to stop another energy crisis being turned into windfall for energy companies.

The US and Israel’s illegal war on Iran has triggered an immediate and painful rise in the price of oil and gas. While Britain only imports a small fraction of its gas from the Gulf, over the last few weeks, UK natural gas futures surged 70 per cent to a three-year high.

This is eerily reminiscent of the convulsions in global energy markets following Russia’s invasion of Ukraine, where gas prices eventually rose to five times their previous levels.

There is a high risk that the present situation could transform into a severe and sustained energy crisis that worsens the cost of living. Given this, the nascent energy crisis requires urgent and forward-thinking action.

British households are especially exposed to external energy shocks. Around 75 per cent of homes are heated via natural gas — in 2024, despite only representing around a quarter of the electricity generation by volume, natural gas set the electricity price 85 per cent of the time.[1] This transmission of volatile and inflated gas prices into the electricity price is an artefact of how Britain’s wholesale market operates.

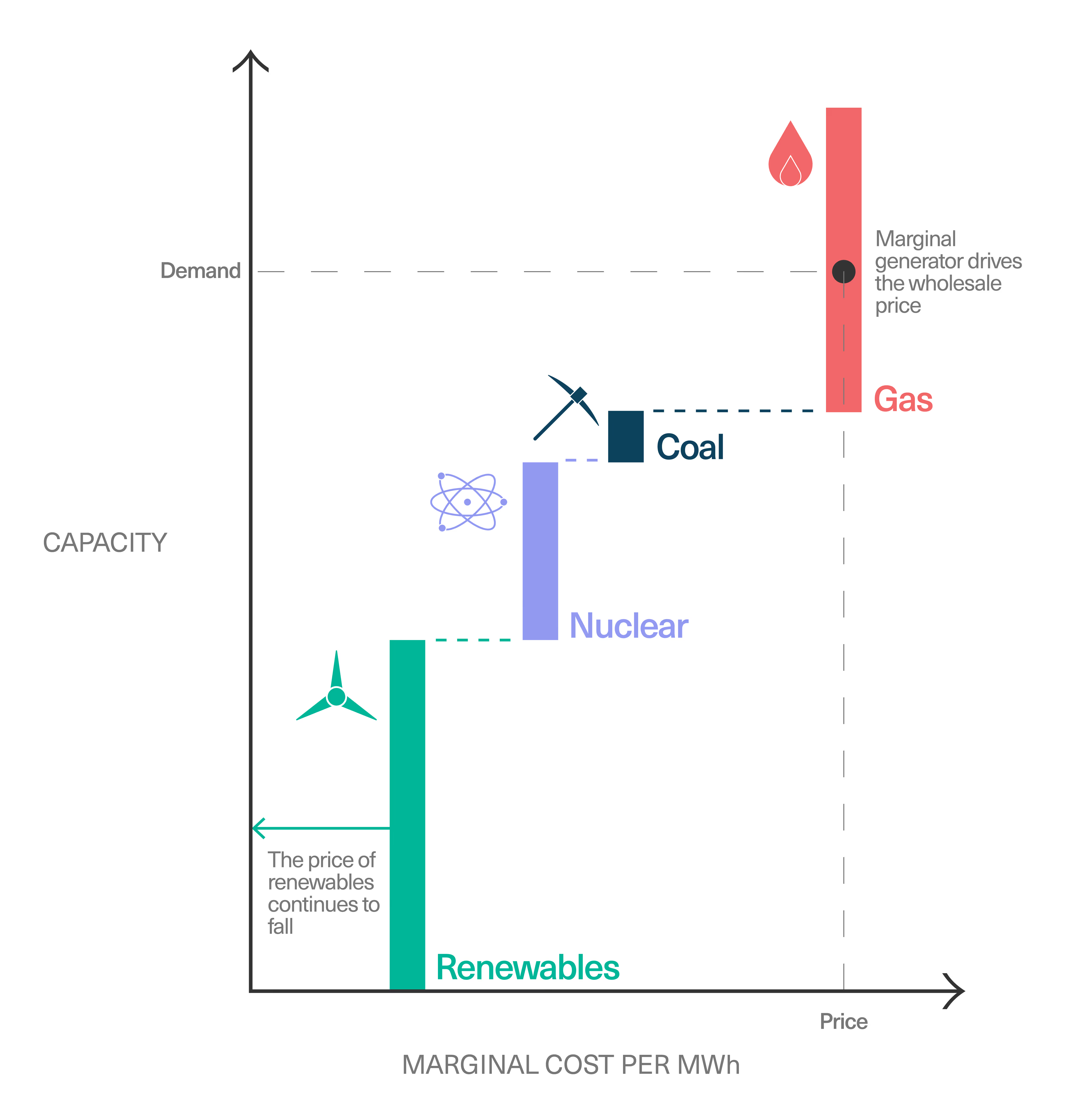

As shown in Figure 1, while the system is now dominated by ostensibly low-cost renewables, the short run marginal pricing mechanism means that the wholesale price is set by the marginal generating unit, used to provide the final portion of power in the wholesale market.[2] This means that Britain’s privately owned fleet of legacy wind farms, nuclear and hydro plants receive the wholesale gas price 85 per cent of the time.[3]

[.fig][.fig-title]Figure 1: Illustrative “Merit Order” of Generators[.fig-title][.fig]

[.notes]Source: Common Wealth visualisation[.notes]

In 2022, electricity prices reached £200–£400/MWh. However, these legacy low carbon assets were built on a business case of £50–60/MWh. This led to windfall profits to these clean power generators, of an estimated £22 billion or around £300 per household in 2022. [4]

Rather than address the root cause of the problem — a system where gas sets the electricity price via the wholesale market, generating unearned windfall profits for legacy clean power generators at the expense of the public, and scarcity rent for gas plant owners — the Truss government created the Energy Price Guarantee (EPG), capping unit costs for gas and electricity to shield households from soaring energy prices.

Despite their windfall profits, the EPG effectively saw the government subsidise the energy companies by around £24 billion. Since then, operators of gas plants have exploited this volatility to charge exorbitant fees for balancing the system, with examples of over £5000/MWh in January 2025.[5] Under the current market design, if the wholesale price of gas remains elevated, without action, it is inevitable that this will be passed on to homes and businesses, when the next price cap period expires in July.

It is too early to predict how high prices will rise and how long the crisis will continue. But recent memory suggests the impacts could be catastrophic for struggling households and reignite the inflation crisis of the early 2020s.

We must act now to mitigate this. Importantly, the proposals we outline below would deliver a significant and enduring benefit regardless of the duration of the crisis, leaving households better off, stabilising a systemically important price like electricity, and shoring up consent for the decarbonisation project.

The Government must remove the price setting function of gas from the electricity market. This will prevent other generators receiving windfall profits and minimise the scarcity rents that can be charged by gas plants.

In 2023, Common Wealth investigated options for reducing windfall profits. We found that the greatest price savings would come from the nationalisation of legacy Renewables Obligation (RO) funded wind and solar along with the nuclear and hydroelectric plants.

Equally, as we argued in 2025, by nationalising the gas fleet and selling at cost, the Government could eliminate any excess profits and rent seeking from the owners and operators of gas power.

If nationalisation is not on the table, the Government must, in any case, act quickly to prevent windfall profits and price increases. We recommend passing emergency legislation and instruct the National Energy System Operator (NESO) to act as a single buyer of power — to remove both these gas and legacy low carbon assets from the wholesale electricity market, onto fixed price contracts. This would address the problem of the windfall profits at source and would be part of our proposal to shift the GB power system towards a single buyer model with power centrally dispatched and prices for all generation brought into a regulated framework, akin to the current Contracts for Difference (CfD) for a new generation.

There is likely to be opposition to these proposals, even though they do not amount to nationalisation, from the incumbents who benefit from the status quo — Britain’s privately and often foreign owned energy sector. Despite this, we believe the scale of this crisis and the structural benefits that can be achieved through reform — for today and the future — necessitate decisive action to put the interests of the British public and British industry ahead of the profits of energy giants.

The Government should instruct the NESO to purchase low carbon power at fixed prices instead of receiving gas linked prices in the wholesale market. Rather than have electricity prices set by inflated wholesale gas costs, our proposal would fix those prices at a (low) level reflecting their cost, meaning lower bills for homes and businesses.

For the legacy low carbon assets, we propose that NESO and the Low Carbon Contracts Company (LCCC) provide a fixed price Power Purchase Agreement (PPAs) to the RO renewables of £50/MWh, £45/MWh to the hydro and £55/MWh for the existing nuclear.

These numbers are indicative, but likely to be a reasonably generous remuneration close to their original business case and similar to the CfD mechanism in operation for newer renewables.

For the gas plants, we proposed shifting these to a Regulated Asset Base (RAB) model, based simply on a regulated profit margin, with all power purchased by the single buyer (NESO) to balance the system. Indeed, Stonehaven and Greenpeace have recently made similar proposals.[7] A similar approach is already taken with the transmission and distribution networks and the new Sizewell C nuclear power plant.

The impact of these proposals depends on the counterfactual wholesale price, the share of electricity that is bought at that price rather than hedged through forward contracts. Building on modelling from a forthcoming report by Common Wealth, Figure 2 outlines some scenarios on the impacts of this policy, based on the difference between the PPA price and the counterfactual average wholesale price. Note that, in the absence of visibility into how much generation has already been locked in under forward contracts, and the term lengths and prices of those contracts, these savings estimates make the simplifying assumption that the counterfactual spot price would apply to 100 per cent of the generation. Assuming the wholesale price does not increase and stays around £80/MWh, the savings on inframarginal rents earned by non-gas generators would still amount to £2.8 billion over 12 months. Should wholesale electricity prices increase to £140 these savings would be £8.5 billion. Should the prices be sustained at the levels seen in 2022/2023 of around £200/MWh, these savings would be a vast £14.3 billion, around £203 per household.

[.fig][.fig-title]Figure 2: Inframarginal Rents Increase with the Scale of the Gas Crisis[.fig-title][.fig-subtitle]Household (right axis) and system (left axis) savings on inframarginal rents from single buyer under different wholesale gas price scenarios[.fig-subtitle][.fig]

[.notes]Source: Author’s calculations based on given parameters. Note: Household savings are based on the domestic sector’s 38% share of consumption.[.notes]

In addition to reducing windfall profits further down the merit curve, there is further scope to reduce rents by gas plants themselves, who appeared to have enhanced their margins during the 2022-23 crisis. Noting the widening “spark spread” between the cost of gas and the price of gas-powered electricity, UCL researchers estimated conservatively that gas plants increased their profits by £3 billion in 2022 (while providing 38 per cent of electricity).[8] As renewable penetration continues to increase, the scale of rent-seeking by gas plants in the wholesale market will be correspondingly lower, but the cost of the balancing mechanism is also expected to further increase (CCGTs accounted for 77 per cent of 2025’s £1.1 billion worth of turn-up costs). This gives a rough sense of the order of magnitude of the direct savings from moving gas into a strategic reserve — whether nationalised or on a RAB model — though more detailed modelling would be required to estimate this more robustly.

No. The proposal would not require transfer of asset ownership.

Instead, generators would remain privately owned. This reform changes how electricity is bought, by asking the NESO to purchase power at fixed prices instead of allowing the market to pay gas-linked prices.

This is similar to how Britain already supports renewable energy through Contracts for Difference, where the government guarantees fixed prices for generators.

No, the single buyer would have no significant fiscal outlay because no fixed assets are being acquired. NESO is already publicly owned.

The current system pays low-cost generators the gas price even though their costs are far lower. In 2022, during the last energy crisis, that produced around £22 billion in windfall profits in that year alone.

By paying generators a fair and fixed price instead, the system prevents those windfalls.

Splitting markets helps but does not solve the full problem in the absence of supplementary interventions. These proposals involve preserving some form of rump wholesale for non-gas electricity and compensating gas plants separately. Greenpeace’s proposal takes gas into a strategic reserve deployed by central dispatch. The Regulatory Assistance Project’s price shock absorber pays the highest non-gas spot price to all non-gas generators further down the merit curve and continues to pay gas plants the marginal price as they have determined it. While gas power is still needed to meet demand most of the time, both proposals could allow the inframarginal rent problem to reappear as non-gas plants increase their sale bids closer to the level set by gas, confident that they will not be pushed out the merit order. In response to this, the gas strategic reserve would allow gas to be deployed as a price ceiling. If gas prices are themselves spiking then an adequate price ceiling would require selling at a loss and recovering those losses through charges to suppliers.

Conversely, during periods of oversupply, prices would likely crash — known as “price cannibalisation”. Our proposal to move these sites onto fixed price contracts would avoid this volatility offering predictable, stable revenues, while eliminating the windfall low carbon generators currently receive.

No, because generators would still receive predictable, stable revenues.

In fact, fixed prices often reduce investor risk compared with volatile wholesale markets. That is exactly why Britain introduced Contracts for Difference, which investors in renewables widely support. The proposal simply applies a similar principle to existing assets.

However, the proposals would reduce revenues for private generating companies and signal that the Government aims to keep a lid on excess profits.

Meanwhile, it is unlikely that the windfall profits from this gas price spike will act as a signal for further private investment in clean energy generation selling into spot markets. This is because the lead time on such investments will likely exceed the duration of this episode, and there is insufficient certainty that future such episodes would make good on such an investment. At the same time such investments will also be especially vulnerable to rising interest rates.

While this would represent a significant change, there are similar systems in operation around the world. Within the context of Britain’s energy system, this proposal reflects and extends the ongoing movement towards a regulated price regime via the CfD.

Examples include:

Emergency action in electricity markets during crises is not unusual, as evidenced during the 2022/3 when major interventions were undertaken by the government.

Implementation would be able to draw on existing mechanisms and practices to expedite the transition. Britain already has a range of institutions and policies that could be expanded and operationalised, there are:

Implementation would involve:

This proposal doesn’t confiscate assets or remove ownership. Generators would continue operating and would receive stable fixed prices close to the levels many projects were originally financed on around £45–£55/MWh. It would allow legacy RO assets to continue receiving the top-up revenues from the Renewable Energy Certificates for the duration of those contracts; it would merely fix the sale price that those ROCs are topping up, removing downside risk as well as upside. Assets on Contracts for Difference would not be affected.

Governments also have clear powers to regulate energy markets in the public interest, especially during crises. The Government has already intervened repeatedly through the energy price cap, windfall taxes and revenue caps on generators during the 2022 crisis.

Legal challenges are possible, but the goal is fundamental and legitimate: protecting households from extreme price shocks is a public interest objective, and allowing billions in windfall profits while families struggle to pay their bills is far harder to justify.

[1] George Smeeton, “Renewable Energy in the UK”, Energy and Climate Intelligence Unit, 2025. Available here.

[2] These issues do not occur in the Contracts for Difference (CfD) mechanism, which offers a fixed price for newer low carbon generators.

[3] This also incorporates the carbon price paid by the marginal gas plant, which does not apply to these low-carbon generators.

[4] Rob Gross, Callum MacIver, Will Blyth, “Pot-Zero: Can renewables and nuclear help keep bills down this winter?”, UK Energy Research Centre, 2024. Available here.

[5] Adam Khan, Chris Hayes, Mathew Lawrence, “Nationalise Gas to Lower Bills”, Common Wealth, 2025. Available here.

[6] RAB models stipulate a significantly lower rate of return than tends to be demanded of assets bearing merchant risk, often less than half.

[7] “Power Shift”, Greenpeace, 2025. Available here.

[8] See footnote 14 in S. Maximov, P. Drummond P. McNally, M. Grubb, “Where Does the Money Go?”, Working Paper #2 UCL Institute for Sustainable Resources, 2023.