Over the past several months, the UK has been gripped by a cost of living crisis, in large part driven by elevated energy costs. Under the current design of Britain’s electricity market (referred to as the “wholesale market”), electricity prices are broadly pegged to the price of gas, which quintupled in the year following the February 2022 invasion of Ukraine. The design of the wholesale market has been critical in both transmitting these soaring gas prices to energy bills for households and businesses, and in creating windfall profits for renewable generators. In response to these trends, a range of stakeholders have set out proposals for reforming the wholesale market, including:

Furthermore, in line with one of the proposals reviewed in this report, the government has enacted the Energy Generator Levy, which effectively serves as a windfall tax on renewable generators.

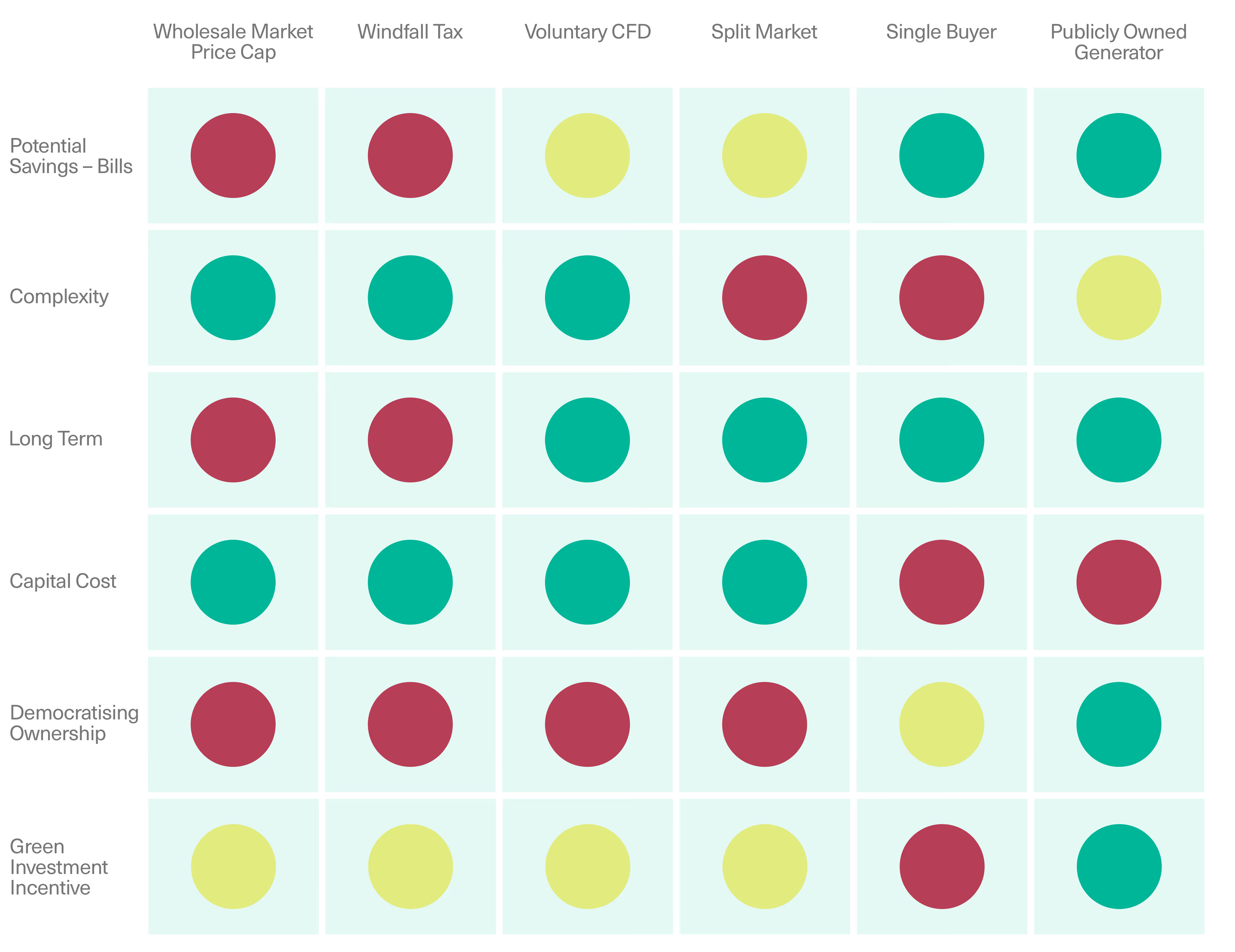

In this report, we review the above proposals, evaluating their respective merits according to key criteria including potential cost savings on bills, complexity of implementation, long term impact, and capital cost, while also considering their potential utility in accelerating the transition to decarbonised electricity system, and in democratising ownership and governance in that system.

While each proposal performs well in different areas, we find that a publicly owned generating company represents the most promising solution across the broadest range of criteria, including its potential to reduce electricity costs by £20.8 bn per year relative to prevailing wholesale prices — the equivalent of £252 per household per year on energy bills. More fundamentally, the public generator is unique in that — depending on its scope and ambition — it could serve as a vehicle for accelerating the transition to one hundred per cent decarbonised electricity generation in the UK as part of a green industrial strategy that prioritises high quality, secure and well-paid jobs within green industries, while also supporting a more democratic energy system.

[.fig]Table 1: Policy Proposals to Reform the Wholesale Market[.fig]

Over the past several months, the UK has been gripped by a cost of living crisis. Much of this has driven by rapidly rising energy prices, particularly household gas and electricity bills. The underlying driver of these rising costs has been surging global gas prices. High gas prices were already driving up electricity prices prior to Russia’s invasion of Ukraine; however, in the year following the February 2022 invasion, the UK’s wholesale natural gas price benchmark quintupled.[1] The impact has been especially acute in the UK, which is almost completely reliant on natural gas for space heating;[2] has among the least energy efficient housing in western Europe;[3] and has a generation mix consisting of 40% gas power, on average.[4]

Importantly, while high global gas prices are the immediate cause of the present crisis, these prices operate within an electricity market whose design is presently inflating bills for homes and businesses while creating windfall profits for some generators. In this report, we examine the current design and functioning of the electricity market in Britain, as well as a suite of existing proposals for its reform. We then evaluate the merits of these proposals according to a set of criteria ranging from savings potential on household bills to the prospects for democratising ownership and governance in the energy system.

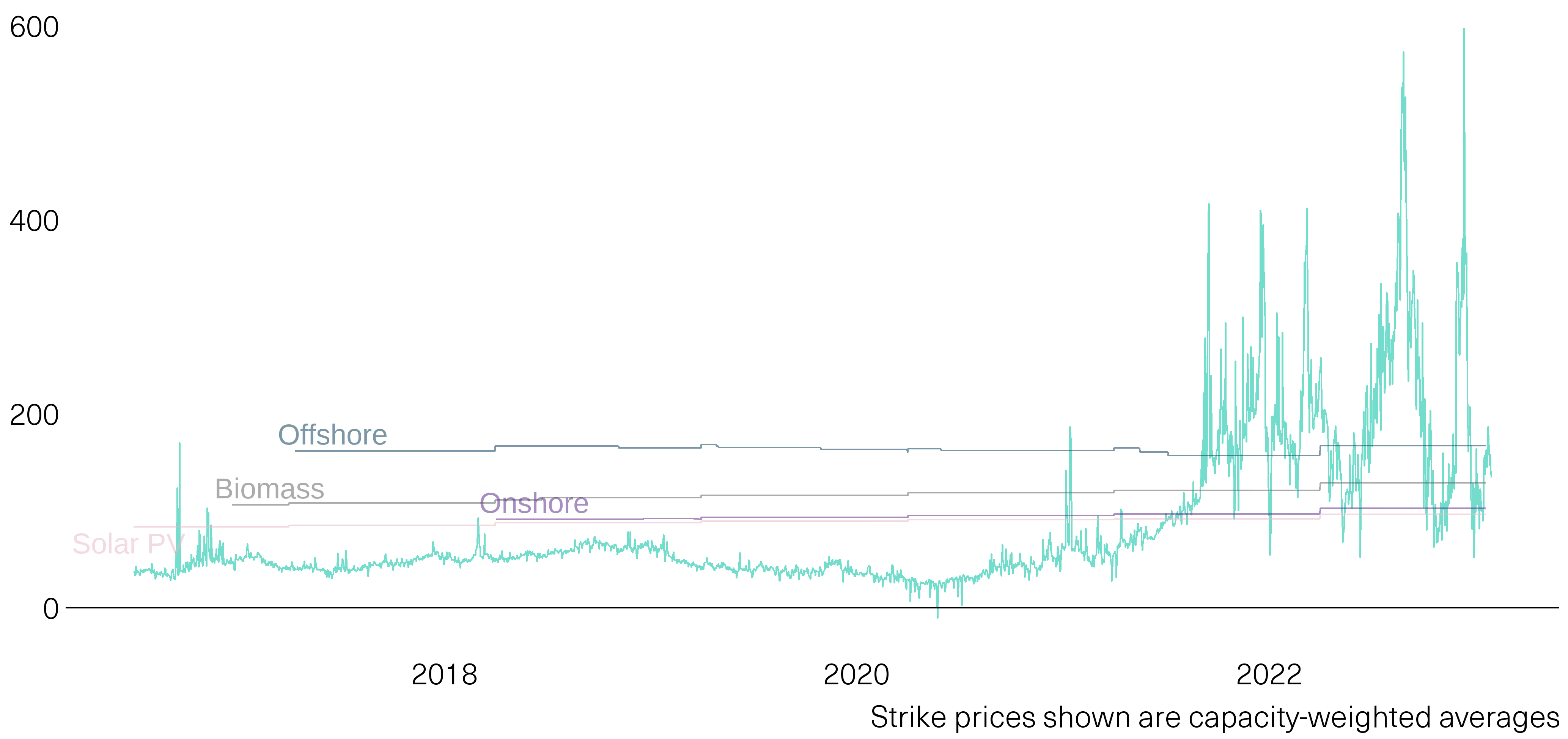

[.fig][.fig-title]Figure 1: GB Day Ahead Hourly Price (£/MWh)[.fig-title][.fig-subtitle]Daily Average Intermittent Market Reference Price (IMRP) vs CfD Strike Prices By Technology[.fig-subtitle][.fig]

The UK was one of the first countries on earth to liberalise, then privatise, its electricity system. The Electricity Act of 1989 paved the way for privatisation, and in 1990 the assets of the Central Electricity Generating Board (CEGB) were broken up into three new companies: Powergen, National Power and National Grid Company, which were floated on the stock market. Later, the nuclear component was privatised into British Energy plc before being sold to the French state-owned company EDF in 2009.[6]

During the 1990s and early 2000s this centralised, integrated system evolved into the fully privatised and fragmented system we have today, which consists of:

At the heart of this system is a wholesale electricity market, which ensures the real-time supply of power to the UK’s consumers on a second-by-second, 24/7 basis. This market has been through several iterations since privatisation, culminating in its present form (since 2005) as the British Electricity Trading Transmission Arrangements (BETTA). BETTA established a single Great British electricity market for England, Wales and Scotland.

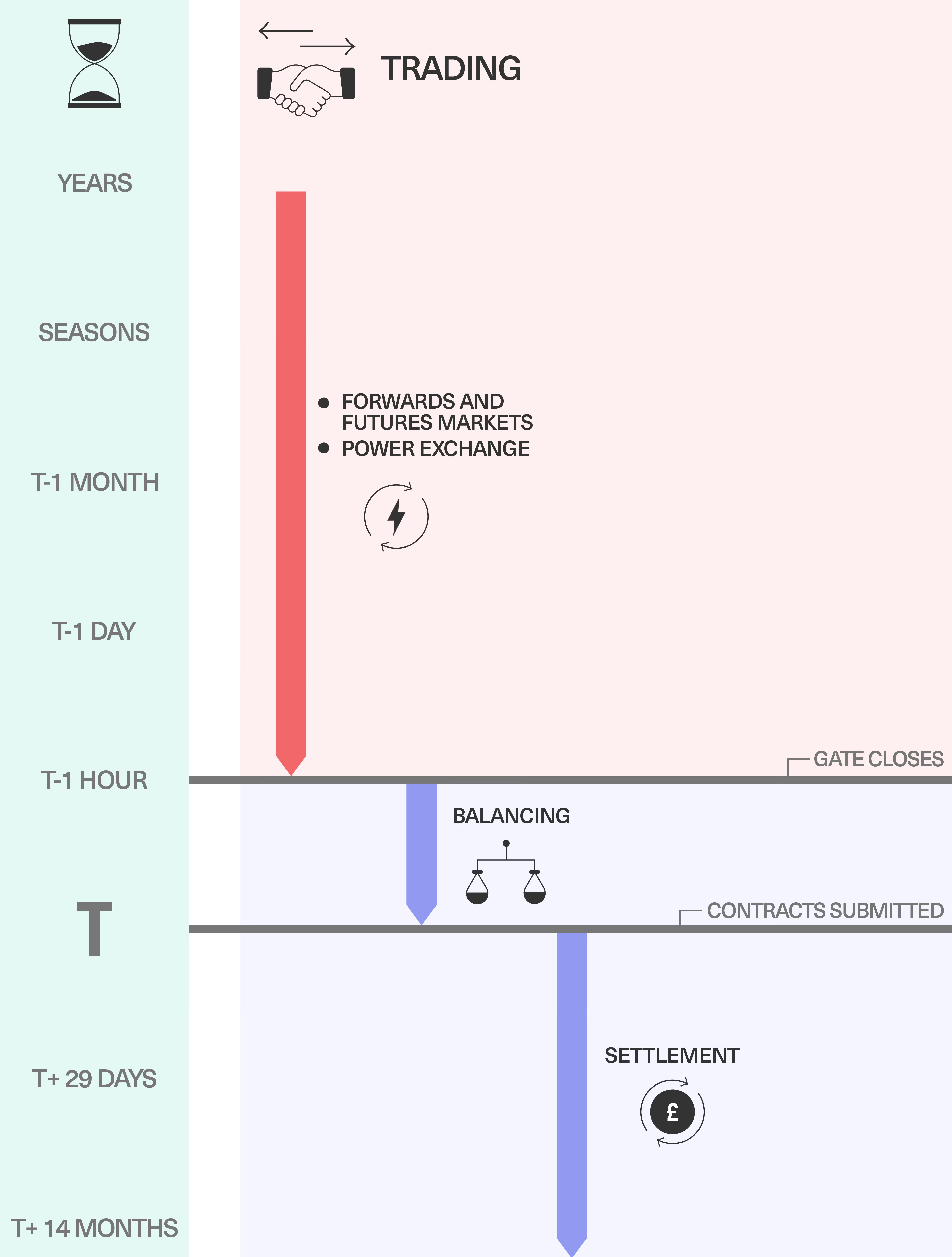

The principle of the wholesale market is to arrive at a single lowest-cost clearing price for the required 30-minute power trading period. Generators negotiate contracts with electricity retailers to provide power in these specific periods. Trading might begin years prior to actual “gate closure” — that is, 30 minutes before the power is to be delivered — but continues over days or even minutes up to this point. The ESO presides over this process to ensure supply is balanced with demand. There are also several other pricing mechanisms to balance the system and ensure power frequency is maintained within a precise threshold following gate closure. A simplified illustration of the market process is summarised in Figure 2 below.

[.fig][.fig-title]Figure 2: How the Wholesale Market Works Over Time[.fig-title][.fig]

[.notes]Source: Common Wealth visualisation based on Elexon.[9][.notes]

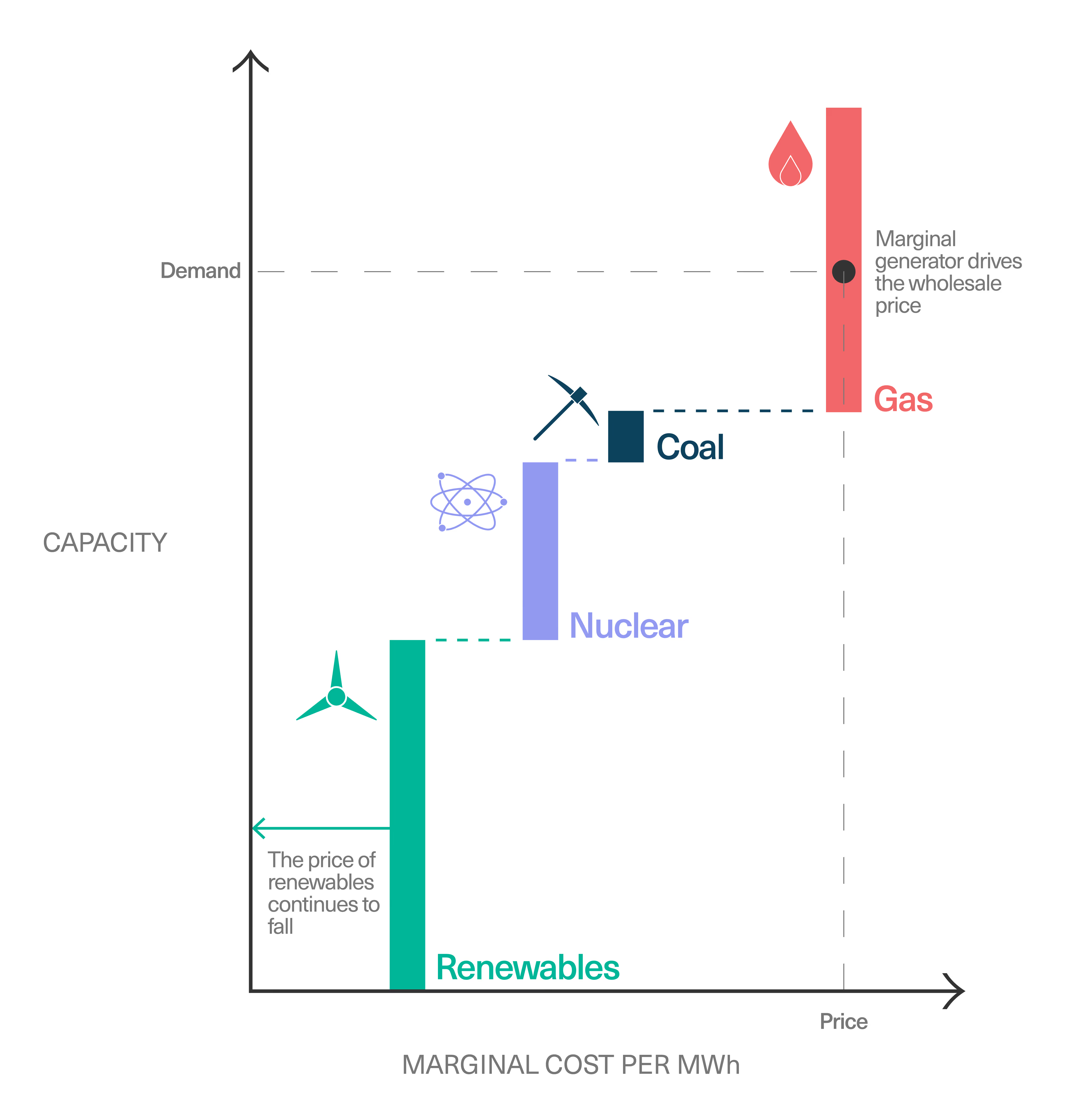

Wholesale power prices are set by the “marginal unit” i.e., the last and most expensive unit of generation required by the system to ensure demand is met. [10] This price “clears” across the whole market, such that all generators (unless separately contracted) receive this price regardless of their running costs, resulting in a single overall market price for power for each thirty-minute interval throughout the day. Different generation sources are used in order from least to highest running cost according to a “merit order”, illustrated in Figure 3. A recent government review into the electricity market described its current operations as “designed for a fossil fuel-based electricity system”. [11]

[.fig][.fig-title]Figure 3: Illustrative “Merit Order” of Generators[.fig-title][.fig]

In general, prices are lower when it is windy or sunny, or when demand is low. But when gas prices are extremely high, any potential for renewable energy or nuclear power to reduce power prices tends to be overwhelmed by the very high price of gas.[12] Over the past several months, the combination of these factors, from low renewable generation to soaring gas prices, has resulted in very high but also volatile electricity prices, as shown in Figure 1, above.[13]

Because the current wholesale market price is largely driven by the marginal unit price, generators that can produce power for substantially less than this, namely nuclear or renewable generators, are currently experiencing large windfall profits. With coal generation largely gone from the system, these windfall profits are primarily being channelled to the UK’s ageing nuclear fleet, owned by the French state-owned EDF; to renewable generators delivered through the Renewables Obligation programme (RO, explained in further detail below), which accounts for the majority of the UK’s renewables projects; and to the two Drax biomass units. While a precise estimate of the windfall profits being made by renewable and nuclear generators is not yet available, the scale of generation being delivered by nuclear and renewables over this period of exceptionally high wholesale prices suggests the profits are likely to be substantial. Precisely how much of the exceptional revenues over this period will have been cashed out in the form of windfall profits will depend on the cost profiles of these plants, with renewable plants enjoying much higher margins than nuclear generators.[15]

While all new large renewable projects are built using the Contracts for Difference (CfD) mechanism (explained in Box 1), most existing large scale renewable energy projects are remunerated through the RO programme. Closed to new entrants since 2017, the RO has driven the construction of the majority of the UK’s existing onshore wind capacity and its larger solar farms. Under the RO, retail suppliers are obligated to source a proportion of their electricity from renewable generators. The obligation is met by purchasing Renewables Obligation Certificates (ROCs) either from generators or the ROC market.[16] Where suppliers do not meet their obligation, they must pay into a buy-out fund at a set cost, which for 2021-22 was approximately £50 per ROC.[17] Depending on the type of generation, different renewable producers receive a fixed number of ROCs per MWh. The result is that renewable projects under the RO receive the value of their electricity as determined by the wholesale market, plus an additional subsidy of the ROC payment per MWh.[18]

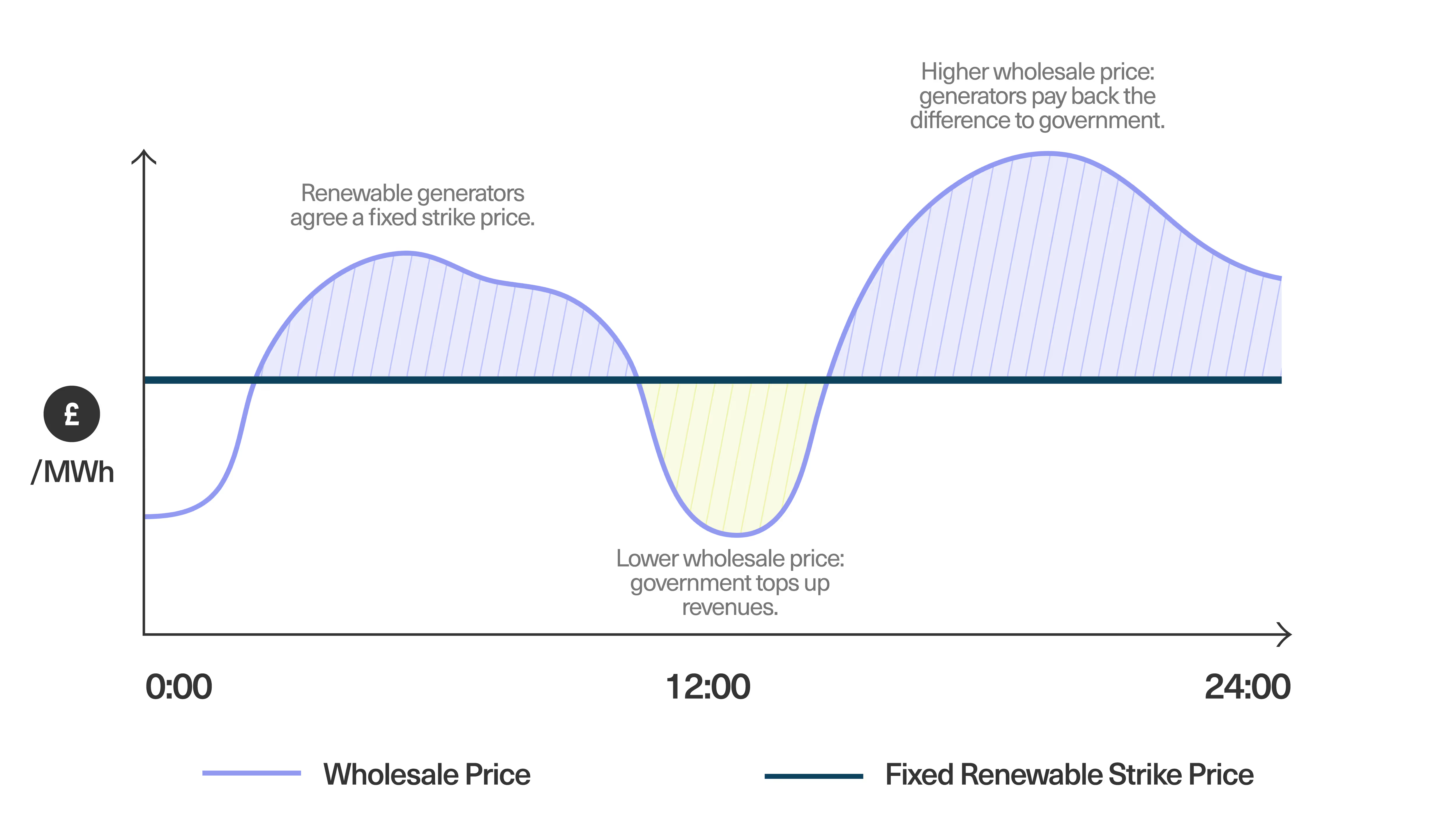

[.box][.box-header]Box 1: Contracts for Difference (CfDs)[.box-header][.box-paragraph]Renewable projects developed since 2017 are remunerated through a scheme called “Contracts for Difference” (CfDs). CfDs will also be applied to the new nuclear power station under development at Hinkley Point and forthcoming renewables schemes. Under the CfD arrangements, generators receive a subsidy if wholesale power prices are lower than an agreed “strike price”, but pay back to consumers via a government-owned company when prices are higher than the strike price. The scheme was devised to reduce risks for investors by guaranteeing them a price, but it also helps to stabilise bills, since the CfD pays a fixed price to generators that is independent of the prevailing wholesale market price of electricity. For operators with a CfD, the arrangement largely breaks the link between gas prices and the price they are paid for the electricity they produce, with most CfD projects expected to pay back to consumers under the current price conditions. For now, only a small fraction (about 6 GW, or roughly 15%) of the total fleet of operational renewable energy projects have a CfD, so the savings on consumer prices remain quite small.[.box-paragraph][.box]

When the business plans for sites under the RO were developed, the average wholesale power price was expected to be £50 or £60/MWh.[19] However, the recent surge in gas prices saw the average day-ahead price for April to August 2022 reach £201.55/MWh, with the average for the month of July reaching £282.54/MWh.[20] Consequently, these legacy projects are now receiving revenues that far exceed their operating costs and expected profit margin. A similar logic applies to existing nuclear, although nuclear generators do not receive the ROC payment. On the back of these anticipated “extraordinary” profits, the government has implemented an Energy Generator Levy on renewable generators, with a 45% levy to be charged on receipts from electricity sold above £75/MWh.[21]

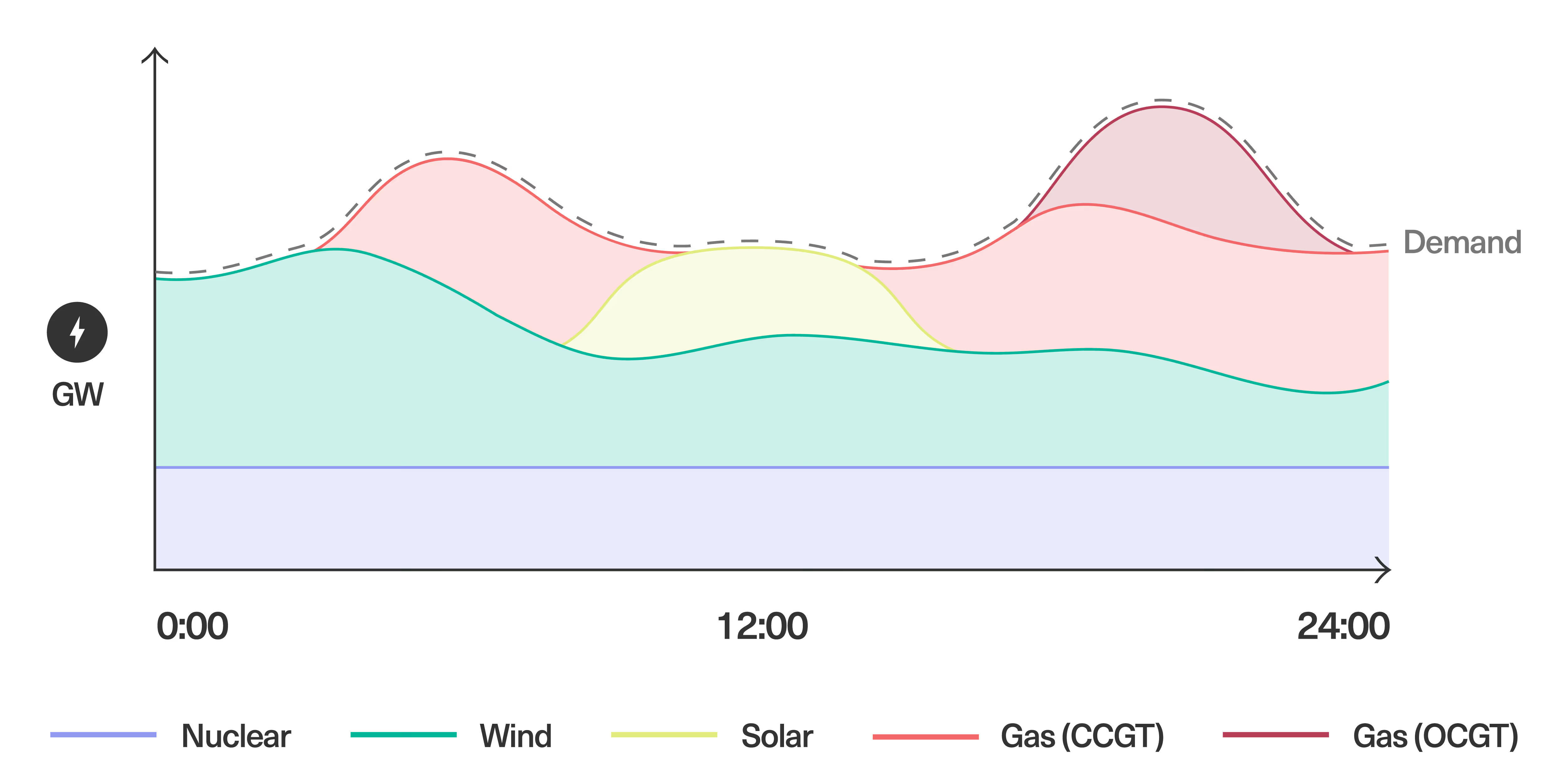

In Figure 4, below, we show an illustrative hypothetical day of electricity production during which gas power is required for most of the day, with a surge in solar generation enabling all power to be produced by low carbon sources for a brief period around noon. An illustrative wholesale market price dynamic that could correspond to this day is shown in Figure 5.[22] It should be noted that in practice, on a single day the complexity of trading means the wholesale price can vary significantly between each half hour interval; in our diagram we have smoothed the price line for ease of interpretation. Throughout the remainder of this report, all diagrams are purely illustrative and intended to demonstrate how different alternative models would function relative to the current wholesale market. For consistency of comparison, all are based on the illustrative day shown in Figure 4.

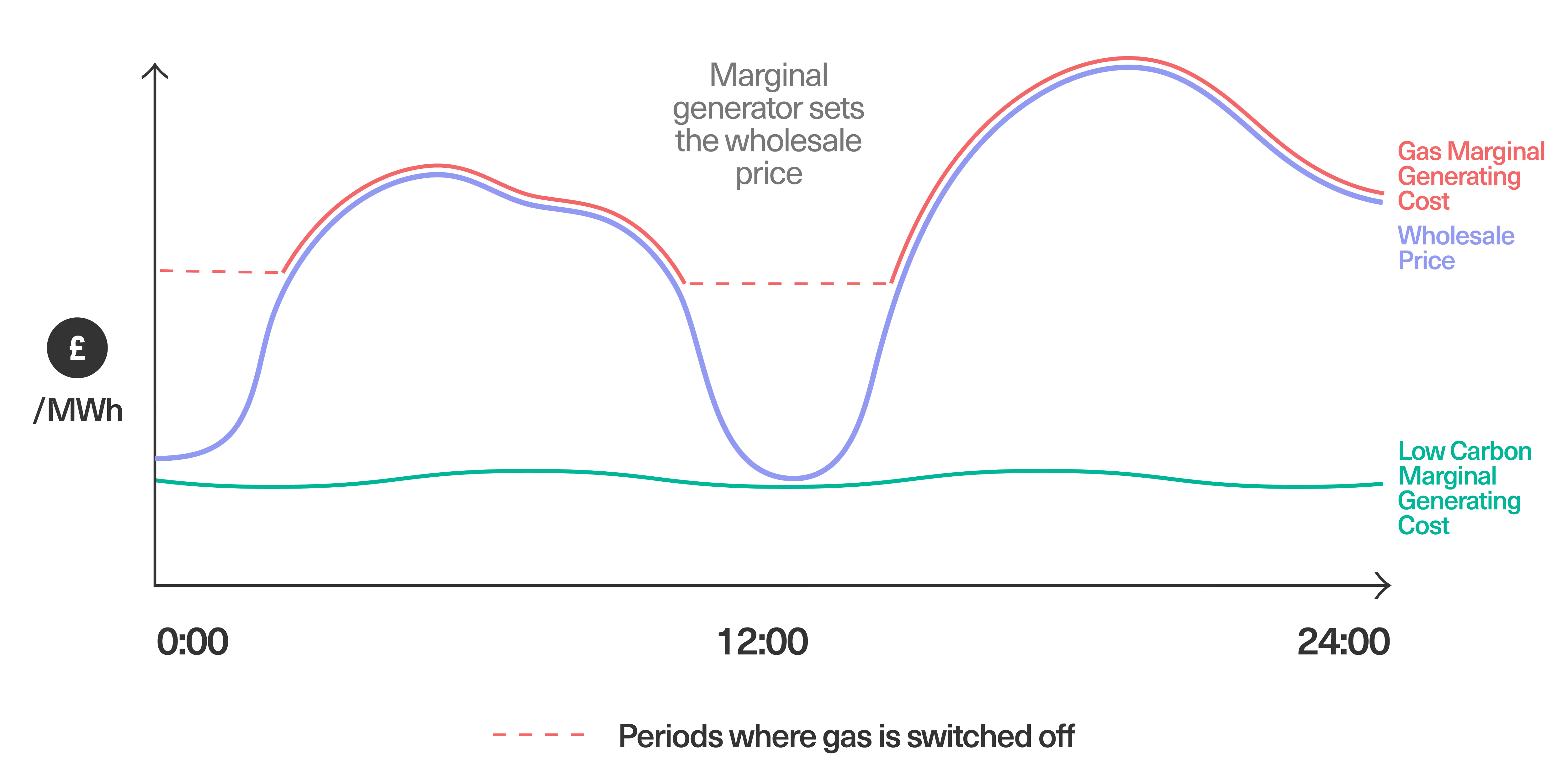

As Figure 5, below, highlights, within the current wholesale model, gas overwhelmingly drives the wholesale price due to its typical position as the marginal generator. In times of peak demand, when less efficient open-cycle gas generators may be required (see Figure 4), these costs are even higher. It is only when renewable and nuclear generation are sufficient to meet total demand that these low-cost, zero-carbon sources set the wholesale price.

[.fig][.fig-title]Figure 4: Energy Production: Illustrative Day[.fig-title][.fig]

[.fig][.fig-title]Figure 5: Current Wholesale Market[.fig-title][.fig]

Government agencies, industry commentators and think tanks have recently set out a range of proposals to reform the wholesale market. In the remainder of this report, we review these proposals for wholesale market reform, which include:

[.num-list][.num-list-num]1[.num-list-num][.num-list-text]A wholesale market price cap for low carbon generators[.num-list-text][.num-list]

[.num-list][.num-list-num]2[.num-list-num][.num-list-text]A windfall tax on generator profits[.num-list-text][.num-list]

[.num-list][.num-list-num]3[.num-list-num][.num-list-text]Shifting low carbon generators (voluntarily) to a CfD[.num-list-text][.num-list]

[.num-list][.num-list-num]4[.num-list-num][.num-list-text]Splitting the power markets into a clean power and a fossil fuel market[.num-list-text][.num-list]

[.num-list][.num-list-num]5[.num-list-num][.num-list-text]A single buyer of electricity, which would imply nationalising the retail sector.[.num-list-text][.num-list]

We add to these proposals:

[.num-list][.num-list-num]6[.num-list-num][.num-list-text]The establishment of a publicly owned generating company, which would purchase legacy low carbon generating assets and invest in rapid build-out of renewable capacity to sell power at a discounted rate into the market or directly via long term contracts.[.num-list-text][.num-list]

We compare the merits of these proposals before briefly outlining how a public generator could work in practice.

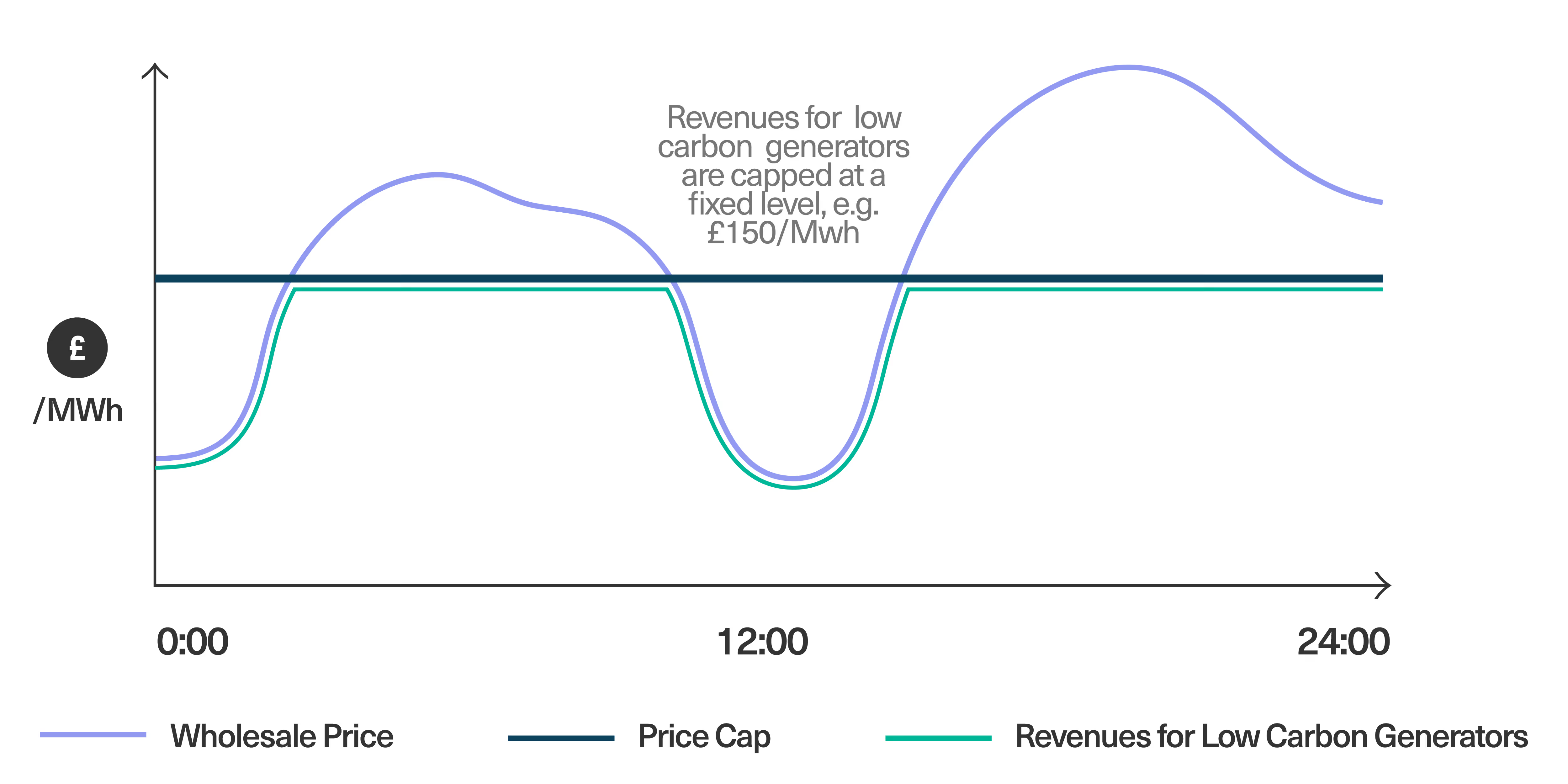

Through a price cap, the government or regulator intervenes in the wholesale market to ensure that some generators do not receive (or are unable to charge) the wholesale price for power above an agreed cap, based on a fixed £/MWh. Because gas generators currently set the high market prices (and therefore these generators are not receiving a windfall), most of these proposals exclude gas generators from the cap mechanism. Instead, the model is designed to cap the revenues of other generators (especially renewables and nuclear not covered by a CfD) in the wholesale market, who are receiving windfall revenues due to exceptional gas, and by extension wholesale, prices. The basic operation of such a price cap is shown in Figure 6 below.

[.fig][.fig-title]Figure 6: Wholesale Market Price Cap[.fig-title][.fig]

On 10 October 2022, the government announced that it would implement a Cost Plus Revenue Limit (CPRL)[23] for low carbon generators not covered by a CfD contract — essentially a wholesale market price cap for low carbon generators. The government’s press release suggested implementing a reasonable cap near pre-crisis expectations of the wholesale price. As sustainability firm Afry notes, “the government has stated that generators will be allowed to retain a proportion (as yet unknown) of revenues above the cap so that they are still incentivised to maximise output when prices are high.”[24] Afry also notes that the proposed approach appeared relatively complex, with generators required to declare their actual revenue before paying back the applicable difference in actual revenue obtained from what would have been obtained at the cap level.[25]

The EU is proposing a similar approach, which would impose a cap at €180/MWh on solar and wind generation.[26] Because this mechanism caps the maximum wholesale price, it assumes the savings are passed on to consumers, theoretically meaning any retail price freeze subsidy is reduced. However, because there is no explicit revenue generation for government, the proposal is distinct to a windfall tax. Intended to be temporary, the model includes no distributional dimension and trusts the market to redistribute the savings.

[.pros-box][.pros-header]Pros[.pros-header][.pros-list-item]Quick to implement.[.pros-list-item][.pros-list-item]Comparatively simple to legislate, as cap can be based on historic revenue profile.[.pros-list-item][.pros-box]

[.cons-box][.cons-header]Cons[.cons-header][.cons-list-item]Temporary — assumes the market will eventually correct windfall profits.[.cons-list-item][.cons-list-item]Likely to have a modest impact on bills (for further detail, see Comparing the Alternatives below).[.cons-list-item][.cons-list-item]No explicit distributional dimension — assumes that energy suppliers will pass on savings and that prices will be reduced across the board.[.cons-list-item][.cons-list-item]Does little or nothing to address long term faults in the wholesale pricing system, nor drive investment in low-cost, low-carbon alternatives.[.cons-list-item][.cons-list-item]Unlikely to prevent majority of windfall profits, as the cap is likely to be set well above the marginal cost of production.[.cons-list-item][.cons-box]

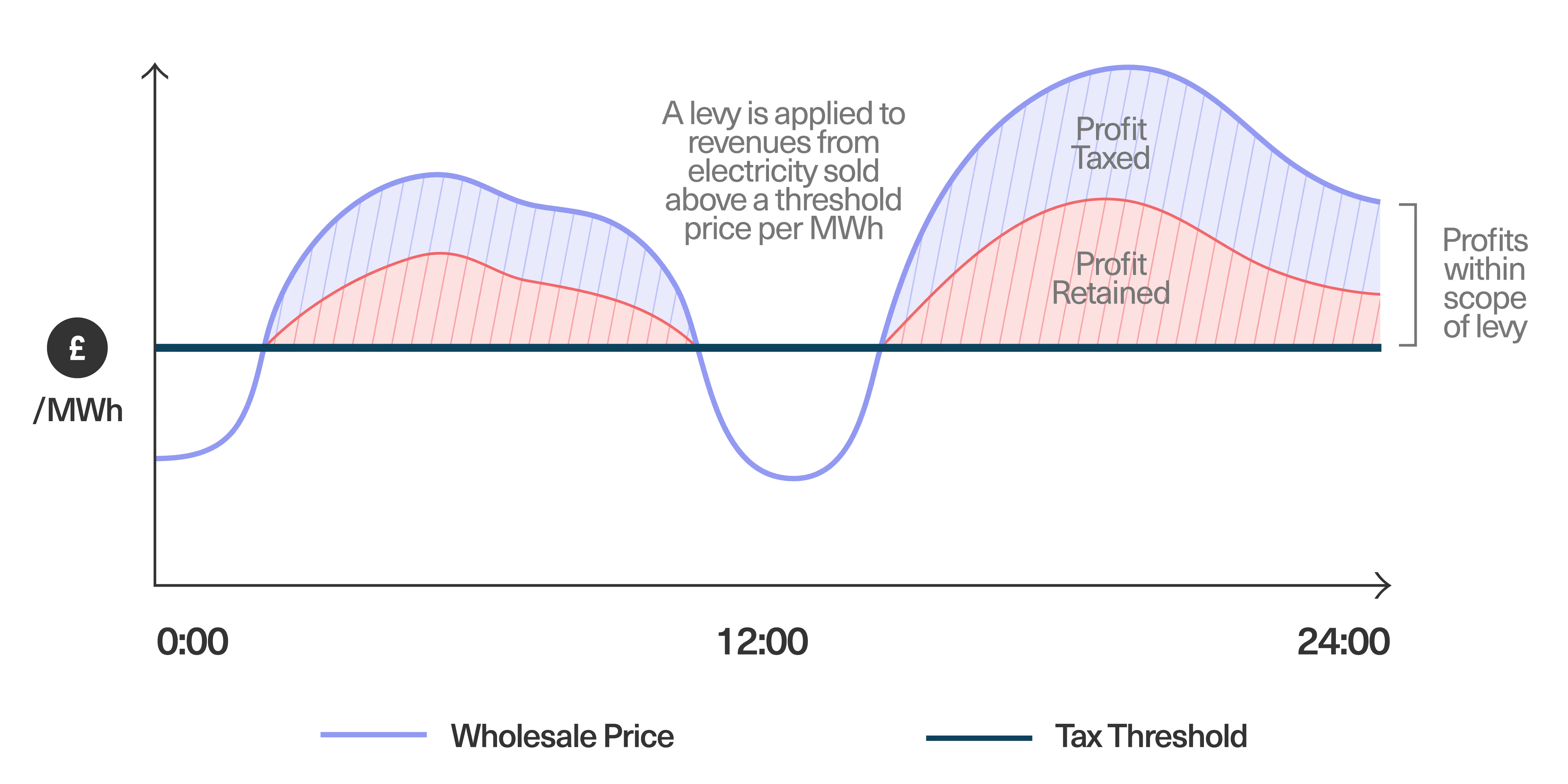

Unlike a price cap, a windfall tax targets profits after the fact. Upon collecting the tax, government would then choose how it redistributes these receipts to consumers. In this way, the windfall tax would help to pay for any price freeze mechanism directly while also allowing government flexibility in how it chooses to distribute these revenues. Because such a tax would target all revenues above a certain level, it would be difficult to disentangle where profits are excess between different generators, although a windfall tax is considered to be simpler to implement than the price cap. There is also a risk that the tax is set too high or low relative to the actual windfall.

[.fig][.fig-title]Figure 7: “Windfall Tax” on Renewable Generators[.fig-title][.fig]

Having initially rejected a windfall tax in favour of a price cap, as of 1 January 2023 the government has enacted the Energy Generator Levy, in place until 2028, which effectively operates as a windfall tax on renewable generators.[27] The tax imposes a 45% additional levy on revenues from electricity sold at higher than £75/MWh (albeit with a group allowance of £10 million per firm).[28] The Financial Times had previously reported that internal Whitehall estimates suggested such a measure could raise £3 bn to £4 bn from power generators.[29] As per Energy UK, a key argument against both the wholesale price cap and windfall tax is that they “could delay and increase the cost of [renewable energy] investments, at a time in which the UK needs to dramatically improve security of supply and rapidly expand the UK’s low carbon infrastructure to provide clean, cheap, and domestically sourced electricity.”[30] Importantly, a windfall tax is a temporary measure, and proposes no durable or more fundamental improvements to the operation of the wholesale market. The basic operation of a windfall tax on renewable generators is shown in Figure 7, above.

[.pros-box][.pros-header]Pros[.pros-header][.pros-list-item]Quick to implement owing to relative simplicity.[.pros-list-item][.pros-list-item]Could be used to help cover costs from policies already applied to energy bills including the Energy Price Guarantee, removal of levies, VAT cuts etc.[.pros-list-item][.pros-list-item]Allows policymakers, in theory, to redistribute revenues to the most vulnerable.[.pros-list-item][.pros-box]

[.cons-box][.cons-header]Cons[.cons-header][.cons-list-item]Temporary — assumes that the market will eventually correct windfall profits.[.cons-list-item][.cons-list-item]Does little or nothing to address long term faults in the wholesale pricing system, nor drive investment in low-cost, low-carbon alternatives.[.cons-list-item][.cons-list-item]Challenging to set tax at appropriate level for diversified businesses with multiple profit sources.[.cons-list-item][.cons-list-item]Unlikely to prevent majority of windfall profits.[.cons-list-item][.cons-box]

An alternative option would be to shift all existing low carbon generators onto CfDs either voluntarily[31] or through a mandatory requirement. This proposal was explored in depth in a recent report by the UK Energy Research Centre (UKERC).[32] By shifting some generators into a CfD arrangement, the scheme would effectively remove those generators from the marginal price mechanism. Therefore, the remaining market price would be dominated by gas and other forms of flexible generation, shown in Figure 8, below.

[.fig]Figure 8: Voluntary Shift to CfDs[.fig]

The UKERC proposals[33] envisage a voluntary shift to CfDs, with the implication that the range of projections for savings on household bills would be very wide, depending on the degree of uptake. For instance, as per UKERC, if 50% of eligible wind and solar power were to join, and the CfD price were to clear at £100/MWh, according to their model, the savings would total approximately £4.9 bn per year, representing a reduction in wholesale costs of 7.2%. This would reduce household bills by an average of £69 per year. By comparison, if 100% of the eligible wind and solar power were to join and the CfD price were to clear at £50/MWh, UKERC’s model suggests the savings would be nearer to £12.8 bn per year. If the scheme was extended to Drax Units 2 & 3 (the large biomass power station) currently receiving RO payments, and the strike price was set at £50/MWh, UKERC suggests savings could reach £14.8 bn per year.

If, in addition, all of Britain’s recently constructed and operating nuclear power stations were to participate, UKERC’s model finds overall savings could total an impressive £22.4 bn annually, representing savings in household bills of £316 per year.

A key disadvantage of this proposal is that, if voluntary, the likelihood of achieving the high uptake outlined in the latter scenarios, and by extension the larger savings on household bills, is low. This is particularly true in the case of the legacy nuclear stations because they are close to the end of their operating lives. Indeed, it is understood that a shift to 15-year CfDs was the preferred option for government in the recent negotiations that ultimately led to the wholesale price cap being introduced, as generators indicated a clear reluctance to sign up to CfDs voluntarily.[34] If made mandatory, several commentators have indicated that a cap would be subject to significant legal challenge, which would likely be won by the private generators, due to longstanding contractual guarantees surrounding the RO and access to the wholesale market.[35]

[.pros-box][.pros-header]Pros[.pros-header][.pros-list-item]Potentially more significant bill savings than with either a tax or price cap.[.pros-list-item][.pros-list-item]If voluntary, it would not undermine investor confidence.[.pros-list-item][.pros-list-item]Creates incentives for existing wind farms looking to repower [36] to enter CfDs to access stable revenues.[.pros-list-item][.pros-box]

[.cons-box][.cons-header]Cons[.cons-header][.cons-list-item]More complex to implement than a tax or price cap.[.cons-list-item][.cons-list-item]Retrospective changes to the terms and conditions set through government policies are generally considered ill-advised, as retroactive rule changes are likely to discourage future investors, not just in renewable energy but in other sectors. Therefore, if transfer to a CfD were made mandatory, major legal challenges would be likely to follow, alongside a possible cooling of investment in the sector.[.cons-list-item][.cons-list-item]Precise impact and savings are unclear and ultimately dependent on the extent of voluntary participation.[.cons-list-item][.cons-list-item]There is a low incentive for old nuclear plants to adopt CFDs due to end of life and decommissioning.[.cons-list-item][.cons-box]

In a more fundamental departure from the existing market design, the International Renewable Energy Agency (IRENA)[37] and Michael Liebreich,[38] founder of Bloomberg New Energy Finance, have proposed splitting the wholesale market in two, with one market for clean power and another for fossil fuel-based generation. The idea of dual markets is premised on the argument that the technological and economic characteristics of its two main components — intermittent renewable and flexible thermal generation — are substantially different. IRENA argues that this causes two inherent marginal pricing misalignments. The first is the revenue cannibalisation effect, whereby periods of high output and low demand produce very low marginal prices for variable renewable electricity, causing extremely low or negative market prices. The second, opposite case — which the UK is currently experiencing — involves periods of high demand dominated by very high prices, from, for instance, expensive gas generation.

Liebreich argues that a longer-term solution would be to establish a separate Clean Power Market (CPM) and Fossil Power Market (FPM). The CPM, pegged to the real cost of producing clean electricity, would cover approximately 60% of current UK power demand at a considerable discount to the current price of gas-power, providing significant immediate relief for UK energy bills. IRENA also emphasises that the FPM element would gradually be replaced by low carbon flexible generation (that is, zero carbon sources that can be deployed at will regardless of weather conditions) and by demand side responses (strategies for reducing overall demand for fossil fuel-based generation, for instance targeted incentives to reduce energy usage at peak times).

While these proposals have much theoretical merit there are several factors that call into question their near-term benefit or viability. First, the UK already has 5.8GW of operational low carbon generation through the CfD scheme, with another 16.7GW awaiting or under construction. These contracts are guaranteed for at least 15 years, with the first CfD-auctioned projects under contract until 2032 at the earliest.[39] A shift away from CfDs towards a more volatile market pricing model, if indeed this were to be the approach taken in establishing a CPM, is likely to be viewed negatively by investors and could therefore jeopardise the UK’s net zero goals if it remains committed to relying on private sector investment in renewable energy.[40]

A second concern relates to volatility in pricing. Per IRENA, in theory, prices could be highly volatile: during periods of low wind and solar generation, prices in the CPM would spike to prices approaching those offered by gas plants in the FPM, with the added cost of legacy RO subsidies. Unless this market was capped, it is likely that these prices would spike to just below the wholesale price in the FPM. By contrast, periods of extremely high production and low prices would be characterised by the opposite problem: plants not covered by an RO or CfD would make losses when prices fail to cover their operating costs, while projects covered by a CfD would require a top up from bill payers. It is for these reasons that the IRENA report suggests the ultimate goal should be to shift all forms of non-dispatchable generation to some form of long-term fixed contract rather than a marginal pricing model.

By comparison, Liebreich argues the critical issue is the likelihood that clean power would trade at equivalent prices to the fossil fuel market without a cap:

To make this work, you would also need to place a price cap on the clean market. Think about it: clean power may now be cheaper to produce than fossil-fueled power and indeed most of it has no fuel cost at all, so you might think it would clear at a lower price, but it won’t. If it did, since it provides essentially the same commodity, buyers would never buy fossil-based power, they would bid up the price for non-fossil until they were equal, and you have gained nothing. You need to put in place a price cap that is high enough for mature clean energy technologies to operate profitably, including the most expensive (most likely stored offshore wind), but no higher. When the market is tight, buyers will bid up the prices to the clean cap, but then have to turn to the fossil market, where prices will be set by gas-based power, which will be uncapped and likely to go much higher, as they do now. What this will do is ensure that the bulk of UK electricity trades at a price set by low-cost renewables, and not by high-cost gas.[41]

In our model of cost savings below we assume, in line with Liebreich, that all power in the CPM trades at the level of an established price cap.

[.pros-box][.pros-header]Pros[.pros-header][.pros-list-item]Means that gas sets the price only for that part of the market which is fulfilled by fossil fuels.[.pros-list-item][.pros-list-item]Reduced costs for clean power market feed directly into bill savings.[.pros-list-item][.pros-box]

[.cons-box][.cons-header]Cons[.cons-header][.cons-list-item]Complex to administer — would effectively require two system operators.[.cons-list-item][.cons-list-item]Retains periods of high volatility, requiring price caps.[.cons-list-item][.cons-box]

The penultimate model considered in this paper represents a fundamental break with the current wholesale market. The Single Buyer model moves toward a centralised approach to electricity pricing and supply. As outlined by the Florence School of Regulation, under a Single Buyer model::

One entity is the designated monopsony buying energy from independent power producers competing for long-term power purchase agreements. The Single Buyer is typically also responsible for securing supply by dispatching all generation assets in real-time at the minimum possible cost. In the US, the Tennessee Valley Authority is an example of a Single Buyer, which procures electricity and sells it to large business customers and distribution companies… The Single Buyer model is common in many African and Asian countries and often used in that context to promote investments in power generation through private ownership, whenever needed.[42] Many variants in the exact implementation of the Single Buyer model exist. In the EU, when introduced by the First Energy Package in 1996, the Single Buyer model was envisioned as a possible transitioning stage from vertical integration to wholesale competition. The EU Directive 1996/92 allowed for a Single Buyer to centrally handle the purchase of electricity as an alternative to a wholesale market with third party access for all generation to the transmission and distribution network.[43]

The single buyer model implies the most radical restructuring of the electricity system of any option listed. It would likely involve the complete nationalisation of the electricity retail market and elimination of the wholesale market, while leaving existing generating capacity in private hands. In this context, the single buyer could effectively set the purchase price from individual generators.

There are, of course, one-off fiscal implications with respect to bringing the UK’s retail electricity system into public ownership. While estimates vary, a recent proposal by the TUC estimated the cost of bringing the “Big Five” energy companies into public ownership at £2.85 bn.[44] By way of comparison, the government recently spent over £2 bn to bail out Bulb Energy, which supplied gas and electricity to 1.7 million customers.[45] Finally, depending how it was structured and implemented, the transition to a single buyer might not address the source of windfall profits in the generation segment of the value chain.

[.pros-box][.pros-header]Pros[.pros-header][.pros-list-item]Potentially significant reduction of overall costs and windfall profits via government monopoly buyer negotiating pricing directly with generators.[.pros-list-item][.pros-box]

[.cons-box][.cons-header]Cons[.cons-header][.cons-list-item]Risk that bi-lateral price renegotiations with existing generators could lead to legal challenges.[.cons-list-item][.cons-list-item]Significant and complex overhaul of electricity system design and market operation.[.cons-list-item][.cons-list-item]Private generating capacity remains largely private and for-profit.[.cons-list-item][.cons-box]

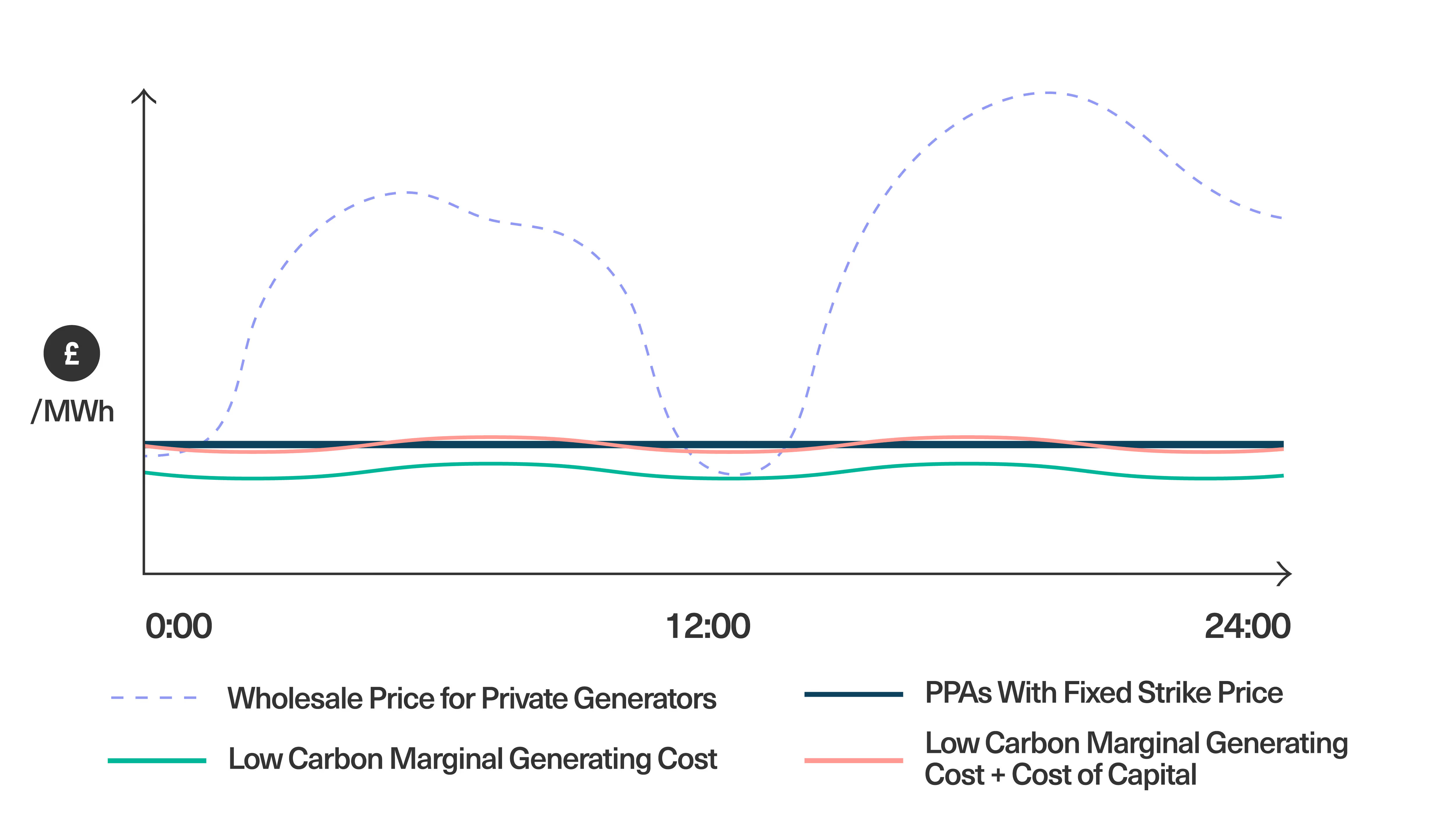

The final alternative explored in this paper is a publicly owned generating company, which could take ownership of legacy low carbon assets and invest in new low carbon capacity. Much like other publicly owned generators including EDF and Vattenfall, this company, acting in the public interest, would sell power into the market or directly via long term PPAs. Because this public generation company could operate on a not-for-profit basis, it could simply charge the marginal production cost plus its cost of capital for acquiring existing low carbon assets and building out new generating capacity. This would involve the effective nationalisation of parts of the electricity generating system, ranging from a small number of assets to total ownership of low carbon generation, depending on ambition. In doing so, the public generator could eliminate windfall profits overnight, and achieve comparable aims to the other models in a comparatively straightforward, if ambitious, manner. The operation of this model with respect to prices is demonstrated in Figure 9 below.

[.fig]Figure 9: Publicly Owned Low Carbon Generator[.fig]

Because the publicly owned generator would set the strike price, it would achieve a similar outcome to the CfD model but guarantee that all low carbon generators would be shifted to a price that simply covers their costs. It is for these reasons that a publicly owned generator is likely to provide overall savings of £20.8 billion annually, representing a reduction in household bills by an average of £252 per year (detailed below).

The exact mechanism for how these legacy assets could be purchased and at what price requires further thought, and will be explored in a subsequent briefing, although traditional compulsory purchase[46] and “shares for government bonds”[47] options would be on the table, as in previous proposals for and implementation of public ownership in the UK.

Importantly, as explored in the final section below and in our prior report, depending on its scope and ambition, the public generator has the potential to accelerate the roll out of renewable generating capacity, acting as a national green energy champion.

[.pros-box][.pros-header]Pros[.pros-header][.pros-list-item]Highest potential for reducing consumers bills by eliminating windfall profits.[.pros-list-item][.pros-list-item]Moderate complexity to administer.[.pros-list-item][.pros-list-item]Leaves wholesale market intact, although dominated by remaining fossil fuel generators[.pros-list-item][.pros-list-item]Diversifies energy system ownership, supporting the expansion of public and community ownership.[.pros-list-item][.pros-box]

[.cons-box][.cons-header]Cons[.cons-header][.cons-list-item]Requires large capital outlay to establish a public energy company.[.cons-list-item][.cons-box]

In the below figure, we provide an illustrative estimate of the near-term reduction in electricity costs that could be achieved by each policy proposal. The details of our model can be found below. We source several assumptions from the authors of the proposals we evaluate. Here we assume:

The full details of our model, along with sources for assumptions, can be found in the Appendix.

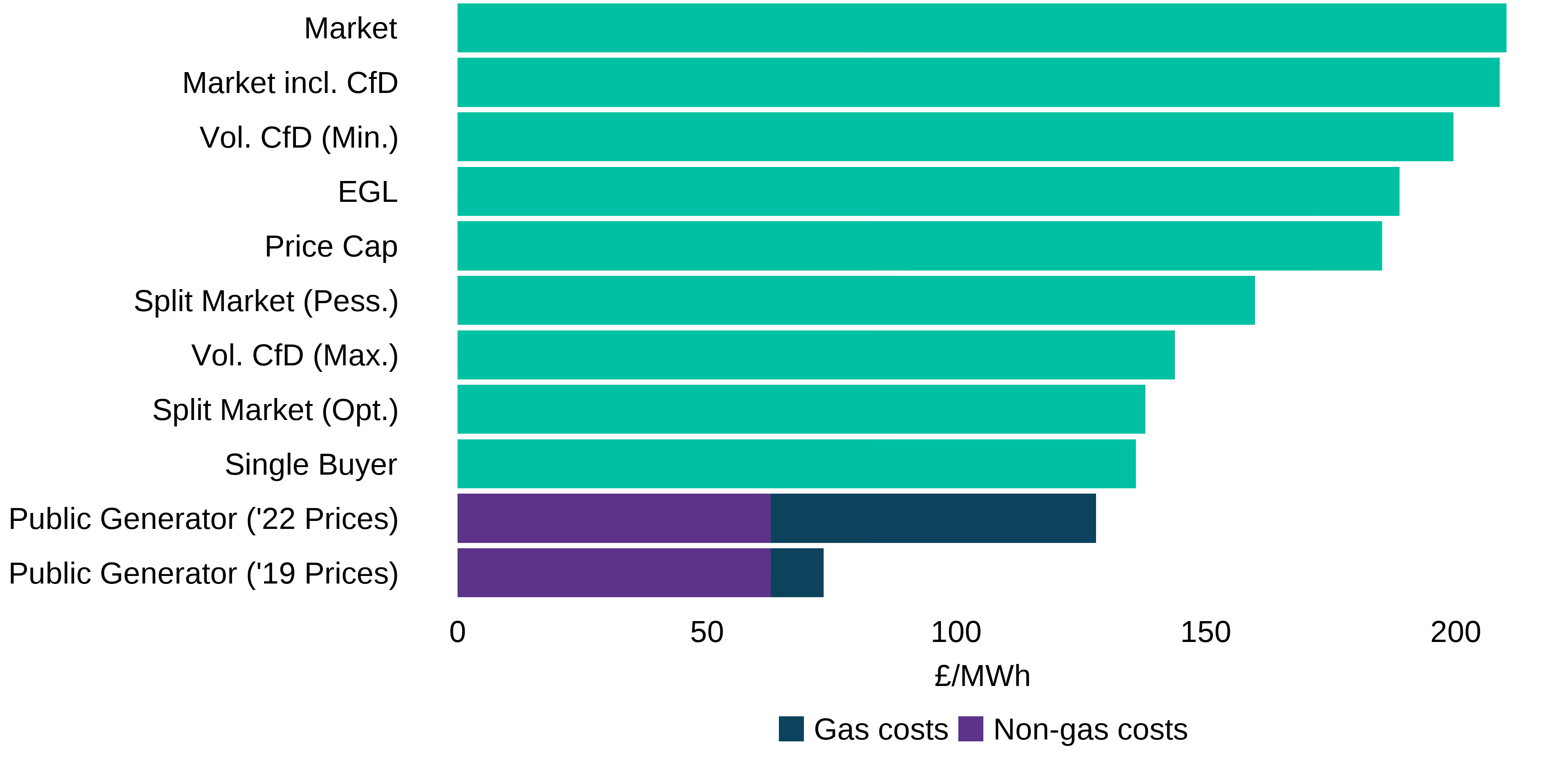

[.fig]Figure 10: Electricity Prices Under Different Policy Proposals, 2022 Averages[.fig]

As shown in the above figure, our model suggests a publicly owned generator offers the greatest overall savings, based on the two core assumptions that it takes ownership of all low-carbon energy (excluding CfD units) and sells that energy at cost to suppliers. Indeed, we find overall savings of £20.8 bn per year relative to prevailing wholesale prices. Noting that households account for approximately 34% of annual electricity consumption, this equates to savings of £252 per household per year on energy bills. However, if one assumes that businesses also pass on 100% of electricity cost savings to consumers, this could rise to savings of £741 per household per year.

We also note that our model finds smaller overall savings would derive from the transition to a voluntary CfD model than those implied by UKERC’s own modelling. Our estimates differ from UKERC’s partly because we calculate over FY 2022 whereas UKERC have calculated over October 2021 to March 2022.

In the table below, we compare the proposals based on key attributes, including and in addition to cost savings. While we consider the wholesale cap, windfall tax and voluntary CfD proposals to be relatively uncomplicated, both the split market and the single buyer model would involve the most fundamental break with the existing electricity market. The publicly owned generator would leave the wholesale market relatively untouched in terms of its operation, although it does require the creation of an entirely new public entity and could entail much of existing generating capacity moving from the wholesale market to power purchase agreements. While the wholesale cap and windfall tax both represent short-term fixes, the other three options would also represent long-term solutions to the issues of high wholesale prices. Further, while the first four options have a low capital cost for government, both the single buyer model and the publicly owned generator would require substantial public investment in the realm of several billion to bring the electricity retail market or low carbon generation asset base into public ownership, respectively. Lastly, we consider the goal of democratising ownership and governance of the electricity system, ensuring it is organised to meet societal and environmental needs rather than maximising private returns.[48] Only the latter two options support this objective, with the publicly owned generator scoring more highly due to the greater potential for it to support and expand local and community ownership of low carbon power.

[.fig]Table 1: Policy Proposals to Reform the Wholesale Market[.fig]

From the analysis presented in this briefing, we believe that a publicly owned generation company — comparable to the Great British Energy company proposed by the Labour Party and also by Common Wealth in a prior publication — represents a key under-explored option for addressing windfall profits, high electricity prices, and a wholesale market in need of reform for a clean energy future. Though there are multiple forms that such a company could take, we propose that this entity would purchase the portfolio of existing UK low carbon generation assets, which would enable it to eliminate excess profits and pass these savings directly on to households and businesses. Of the six policy options evaluated, our estimates suggest this option would deliver the greatest savings on electricity costs (up to £20.8 bn per year). Importantly, it also scores highly against our other criteria concerning complexity, whether a solution is long-term, accelerating the transition to clean energy, and building democratic ownership and governance in the energy system.

The primary challenge likely to be levied against to this proposal is the capital cost implied by purchasing these assets. While the costs and specific details for bringing the low carbon asset base into public ownership are beyond the scope of the present paper, we do not believe the scale of investment to be an insurmountable barrier. Indeed, renewable generating capacity would represent an asset on the government’s balance sheet, with interest on associated borrowing paid for through electricity sales, while also providing an operational asset base for further expansion into the build out of new low carbon generating capacity as well as higher risk renewable generation projects. Depending on its level of ambition and the nature of its role in the energy system, a publicly owned generator could deliver several benefits not offered by other proposals. We discuss these briefly here, but for further elaboration see our report, “Power to the People: The Case for a Publicly Owned Generation Company”.

Firstly, in contrast to the prevailing approach to building out renewable energy capacity, in which private financing, market-based governance and profit-focused goals guide development and pricing, GBE would build out a renewable future based on public financing, social governance and democratic planning to meet urgent climate and energy needs. This model follows the path of other leading low carbon economies who have public energy champions, including EDF (France), EnBW (Germany), and Vattenfall (Sweden).

Secondly, combined with reform of supply processes, either through changes to the wholesale market or by entering direct Power Purchase Agreements with a largescale publicly owned supplier, a public entity that owned existing low carbon generation assets and had an ambitious build-out programme of new clean energy assets would be able to effectively deliver on its core goals: accelerating the transition to a green, secure, affordable energy future, where the country’s shared energy resources are developed for common benefit. In a forthcoming paper, we will examine the cost savings for the transition to clean energy that can be achieved through a large-scale public vehicle; detail an investment pathway for accelerating the roll out of clean energy infrastructure owned by the public; and propose an institutional design for a public company that operates at a range of scales from community to the nations of the UK.

Thirdly, a public generator could also contribute to the growth of a more democratic energy system by supporting the expansion of community ownership and governance. By purchasing existing privately held wind and solar farms, the company could offer community shares to local residents and other stakeholders, helping to build community wealth and democratic forms of ownership and governance in the process. This is likely to strengthen the social contract surrounding local renewables projects while providing a strong basis for the expansion and repowering of these ageing sites with local communities in the future. It could also act to support local authorities and City Mayors accelerate the roll-out of municipal green energy generation, that would be integrated into a wider public system of clean power.

Fourthly, a public generating company can also play an anchoring role in any wider green industrial strategy, helping to onshore high-value manufacturing and service roles associated with the energy transition, while adopting high quality terms and conditions of employment set by collective bargaining. Indeed, a public energy system could be the backbone of the wider industrial transition, while doing so on fundamentally different principles and goals than the status quo.

Perhaps above all, public ownership of existing and future renewable assets would mean common resources — the energy of the wind, waves, and sun — would be developed for public benefit. Unlike the development of the UK’s oil and gas resources, this would ensure the wealth of the commons would be stewarded for all our benefit, a permanent enlargement of the common wealth.

If pursued with ambition, a publicly owned clean energy generator can be a powerful tool for building a decarbonised future that works for all. With respect to setting the level of ambition for a “Great British Energy” style public generator, there is a clear political analogue with the creation of the NHS: if the post-war government had pursued an incrementalist approach to its creation, taking only a handful of clinics into a public health system while leaving the majority of the sector in private hands, there is little doubt it would not have grown into the service it became. It would also have lacked the institutional heft and public support needed to enact and embed reform and resist rollback. Likewise, today, an approach to energy system reform that does not go to the root of the upstream problems in our energy system, that does not build out at scale and instead remains a marginal actor in the transition, will be unable to deliver on its potential or, in the case of Great British Energy, its stated goals. In this context, timidity and incrementalism are the greatest risks, and ambition the safest path forward.

To estimate the savings on energy costs that could derive from each proposal, we use a backward-looking model that recreates the hourly generation profile of 2022 with the corresponding wholesale price (IMRP), using data from Elexon BMRS and the University of Sheffield’s PV Live service.[49] The model matches this generation profile with BEIS DUKES data on aggregate and individual power station capacity, attributing hourly generation and wholesale revenue to plants on a proportional basis relative to capacity.[50] Daily generation by and payments to and from CfD units are incorporated into the model, using data from the Low Carbon Contrast Company (LCCC).[51] The costs of all plants are estimated using the assumptions underpinning BEIS’s own LCOE estimates.[52] Taking the gross outcomes of the marginal pricing auctions as given, we then calculate the backward-looking impact of each policy proposal on the effective price – that is, net of caps, levies and CfD payments – for each generator at each hour, and then the ensuing average wholesale price facing suppliers, assuming that 100% of these levies and CfD payments etc. are passed through to the supplier. Combining with marginal cost estimates, we are also able to calculate operating profits at the generator- (and likewise firm-) level. The idiosyncratic effect of the Ofgem price cap means that we do not calculate its effect on household bills.

Our estimates instead describe the amount that each policy redistributes away from generators down the supply chain. The estimates for the single buyer and public generation models are sensitive to cost assumptions, and therefore come with the obvious caveat. As noted, in our model these are assumed to be in line with the BEIS LCOE estimates. Fixed and semi-fixed capital expenditure includes pre-development costs, construction costs, and infrastructure costs. Operating expenditure includes both fixed and variable operational and maintenance expenditure, as well as insurance, connection costs, fuel prices, transport and storage costs, decommissioning fund costs, heat revenues and carbon costs. We do not account for financing costs or project-specific hurdle rates.

For the other policy proposals, these cost assumptions do not impact on our estimates as these are based on prevailing wholesale prices and policy assumptions such as strike prices, price caps and levy thresholds, as per the policy proposals evaluated.

[1] Rob Davies, “Gas Price Hike of More than 30% Stokes Home Bills Fears for Europe”, The Guardian, 04/01/2022. Available here. See also.

[2] Digest of UK Energy Statistics (DUKES) 2022”, Department for Business, Energy & Industrial Strategy, July 2022. Available here.

[3] UK homes losing heat up to three times faster than European neighbours”, Tado, 20/02/2022. Available here.

[4] Alex Lawson, “Great Britain’s Electricity at Record High in 2022 but Gas Use Up Too”, The Guardian, 06/01/23. Available here.

[5] Ronan Bolton, “The History of Electricity Markets in Britain and Europe, UKERC, 03/03/2022. Available here.

[6] Peter Pearson, Jim Watson, “UK Energy Policy 1980-2010”, The Institution of Engineering and Technology, and Parliamentary Group for Energy Studies. Available here.

[7] As of October 2022, six company groups hold the fourteen distribution licences. For further detail on the DNOs, see Joseph Baines and Sandy Brian Hager, “Profiting Amid the Energy Crisis: The Distribution Networks at the Heart of the UK’s Gas and Electricity System”, Common Wealth. Available here.

[8] Following a government announcement, the ESO is to become an independent publicly owned body. For a detailed analysis of National Grid plc’s business segments, see Sophie Flinders, Chris Hayes and Adrienne Buller, “National Grid: Ownership and Key Financial Indicators”, Common Wealth. Available here.

[9] See “Trading and Settlement”, Elexon. Available here.

[10] Tom Jones, “What drives wholesale electricity prices in Britain?”, Ofgem, July 2016. Available here.

[11] “Review of Electricity Market Arrangements: Consultation Document”, Department for Business, Energy and Industrial Strategy, July 2022. Available here.

[12] Rob Gross, Callum MacIver and Will Blyth, “Can Renewables and Nuclear Help Keep Bills Down this Winter?”, UKERC, April 2022. Available here.

[13] James Smith, Gerben Hieminga, “UK Power Price Spike Exposes the Challenges of Net Zero Electricity, ING, 29/09/2021. Available here.

[14] We note that from October 2021, when wholesale prices surpassed £100/MWh, to the end of 2022, 26% of the UK’s 214TWh of non-fossil-fuel energy generation came from EDF’s nuclear plants, while wind accounted for 46% of generation (8% of which is owned by Ørsted and a further 7% by RWE) and bioenergy for 11% (of which 3.6% is owned by Drax).

[15] Based on EBIT(DA) margins.

[16] “The Renewables Obligation Explained”, E-ON Energy. Available here.

[17] “Renewables Obligation (RO) Buy-out Price, Mutualisation Threshold and Mutualisation Ceilings for 2021-22”, Ofgem, 09/04/2021. Available here.

[18] “Calculating Renewable Obligation Certificates (ROCs)”, Department for Business, Energy & Industrial Strategy and Ofgem, 22/01/2013. Available here.

[19] Rob Gross, Callum MacIver and Will Blyth, “Can Renewables and Nuclear Help Keep Bills Down this Winter?”, UKERC, April 2022. Available here.

[20] Tom Faulkner, “From Zero to Hero: Can CfDs Split Markets and Reduce Cosgts this Winter”, Cornwall Insight, 11/10/2022. Available here.

[21] “Policy Paper: Energy Generator Levy”,Gov.UK, 20/12/2022. Available here.

[22] For a further illustrative example of this dynamic see here.

[23] “Government introduces new Energy Prices Bill to ensure vital support gets to British consumers this winter”, Gov.UK, 11/10/2022. Available here.

[24] Ali Lloyd, “The Cost Plus Revenue Limit: some initial reflections”, Afry, 18/10/2022. Available here.

[25] Ibid.

[26] Beatriz Santos, “EU proposes €0.18/kWh price cap on solar, wind”, PV Magazine, 14/09/2022. Available here.

[27] “Electricity Generator Levy”, HM Customs, 20/12/2022. Available here. “Electricity Generator Levy: Everything you need to know”, Bird & Bird, 29/11/2022. Available here.

[28] “Electricity Generator Levy”, Bird & Bird. Available here.

[29] George Parker and Nathalie Thomas, “Windfall tax on UK electricity generators would curb investment, warns Labour”, Financial Times, 05/06/2022. Available here.

[30] “Impact of a Generators’ Windfall Tax on Investment”, Energy UK, 08/06/2022. Available here.

[31] “Reducing the impact of gas on retail power prices through Voluntary Contracts for Difference”, Energy UK, 01/09/2022. Available here.

[32] Rob Gross, Callum MacIver and Will Blyth, “Can Renewables and Nuclear Help Keep Bills Down this Winter?”, UKERC, April 2022. Available here.

[33] Based on April 2022 prices.

[34] Nathalie Thomas and Jim Pickard, “British Low Carbon Generators Face de Facto Windfall Tax”, Financial Times, 11/10/2022. Available here.

[35] “UK Energy Prices Bill: A Windfall Tax for Low Carbon Generation?”, Allen & Overy, Jd Supra, 17/10/2022. Available here.

[36] “Repowering” describes replacing old generating infrastructure, i.e., replacing aging wind turbines with newer technology.

[37] “Potential Limitations of Marginal Pricing for a Power System Based on Renewables”, IRENA, September 2022. Available here.

[38] Michael Liebreich, “UK Energy Crisis – Time to Split the Power Market?”, published on LinkedIn here.

[39] Common Wealth analysis of “Renewable Energy Planning Database: quarterly extract”, Department for Business Energy and Industrial Strategy, October 2022. Available here.

[40] Anjie Fan et al., “Performance Comparison Between Renewable Obligation and Feed-in Tariff with Contract for Difference in UK”, 2018 China International Conference on Electricity Distribution. Available here.

[41] Michael Liebreich, “UK Energy Crisis – Time to Split the Power Market?”, published on LinkedIn here.

[42] More information about the African context can be found in “Revisiting Reforms in the Power Sector in Africa”, African Development Bank Group, 2019. Available here.

[43] “Regulatory Models in the Power Sector”, Florence School of Regulation, 03/08/2022. Available here.

[44] See “A fairer energy system for families and the climate”, Trades Union Congress, July 2022. Available here.

[45] Jillian Ambrose, “Bailout Process for Collapsed Bulb Energy Will Rely on Public Funds”, 22/11/2021. Available here.

[46] “Guidance: Compulsory Purchase and Compensation Guide 1 Procedure”, Gov.UK, 17/12/2021. Available here.

[47] “John McDonnell: Labour Public Ownership Plan Will Cost Nothing”, BBC, 10/02/2018. Available here.

[48] For further elaboration of these arguments, see Mathew Lawrence, “Power to the People: The Case for a Publicly Owned Generation Company”, Common Wealth, September 2022. Available here.

[49] “Generation by Fuel Type”, Balancing Mechanism Reporting Service (BMRS). Available here. “PV Live”, Sheffield Solar. Available here.

[50] “Digest of UK Energy Statistics (DUKES) 2022”, Department for Business, Energy & Industrial Strategy, July 2022. Available here.

[51] “Datasets”, Low Carbon Contracts Company Data Portal. Available here.

[52] “Electricity Generation Costs 2020”, Department for Business, Energy & Industrial Strategy, August 2020. Available here.