Corporate earnings announcements are no longer confined to the pages of the business press. Instead, they now feature as leading headlines and sources of public debate, particularly for sectors like energy. Last week, BP and Shell again posted chart-topping profits and committed eye-watering sums to shareholder payouts. In the case of Shell, for every £1 the firm invested in their “Renewables and Energy Solutions” segment (which, it should be emphasised, includes gas trading), they spent £6 on fossil fuel investment £14 on shareholder payouts. Shell’s buyback commitments for the first half of 2023 alone total £6.4 billion.

In response, calls have resurfaced for policies with the teeth to curb these exceptional profits and payouts and accelerate the sluggish transition to clean energy, including Labour’s renewed call for a windfall tax on the industry without the subsidy to oil and gas producers found in the government's Energy Profits Levy. Criticisms of such proposals are just as wide-ranging, but among these, one argument is repeated ad nauseum: that the true beneficiaries of shareholder payouts are the pensions of ordinary people; to rein them in is therefore an attack on their income.

As the argument goes, we all need to save for retirement, and our pension funds have to invest our savings somewhere. It is therefore naive to regard exorbitant shareholder payouts as upwards redistribution. Rather, the workers and consumers who could have enjoyed that surplus through higher wages or lower prices are largely the same people who will enjoy those payouts through their pension pots. The final corollary — less often made explicit — is that if we ever try to restrain corporate excesses, then ordinary people stand to suffer the consequences.

The political implications of this argument are disturbing. Taking them seriously, any action to restrain lavish payouts ceases to be means of recapturing and more fairly or productively distributing these cash flows. Instead, the welfare of pensioners both today and tomorrow becomes tethered to these payouts and their frequent bedfellows: higher prices, lower pay, and low investment in productive capacity. The policy space shrinks dramatically as a result. Indeed, within this framework, where the shareholder interest is taken to be the same as the public interest, the only viable policy option is to do nothing. The argument clearly has intuitive appeal. But to what extent is it true? Who, really, are the main beneficiaries of shareholder payouts.

The argument that interventions to restrain corporate profits and payouts are detrimental to UK pension holders relies on two implicit premises.

If these two implicit premises are false, it becomes difficult to defend the case that interventions that aim to redirect how corporation’s use their surplus away rewarding shareholders would be more harmful to pension holders than the benefits that might accrue from progressively designed policies, such as lowering energy or food prices or increasing investment or wages.

The two-trillion pound question, then, is: do these premises hold? To answer it, we need to trace the path of corporate profits and payouts from individual shares through to pension funds and their ultimate beneficiaries.

This article addresses each of these premises in turn. We begin by documenting the UK pension sector’s overall very low exposure to UK listed equities, acknowledging somewhat higher exposure among the younger defined contribution (DC) schemes that comprise only 19% of pension assets. We follow by noting the similarly extremely small proportion of UK listed stock held by UK pension funds both directly and indirectly through pooled funds. Both trends are consequences of rising diversification in financial intermediation. We follow up by highlighting the highly unequal distribution of private pension wealth among UK households, underscoring the regressive dimension to the meagre portion of shareholder payouts that do land in our pensions. We conclude by arguing that whatever entwinement does persist between corporate excess and the fates of UK pensioners is itself a wholly avoidable policy mistake, contributing to the irrational dysfunction of our political economy.

UK pension funds have transformed over the past several decades, both in the proliferation of defined contribution (DC) participants and gradual closure of defined benefit (DB) schemes and through major changes in portfolio allocation strategies.

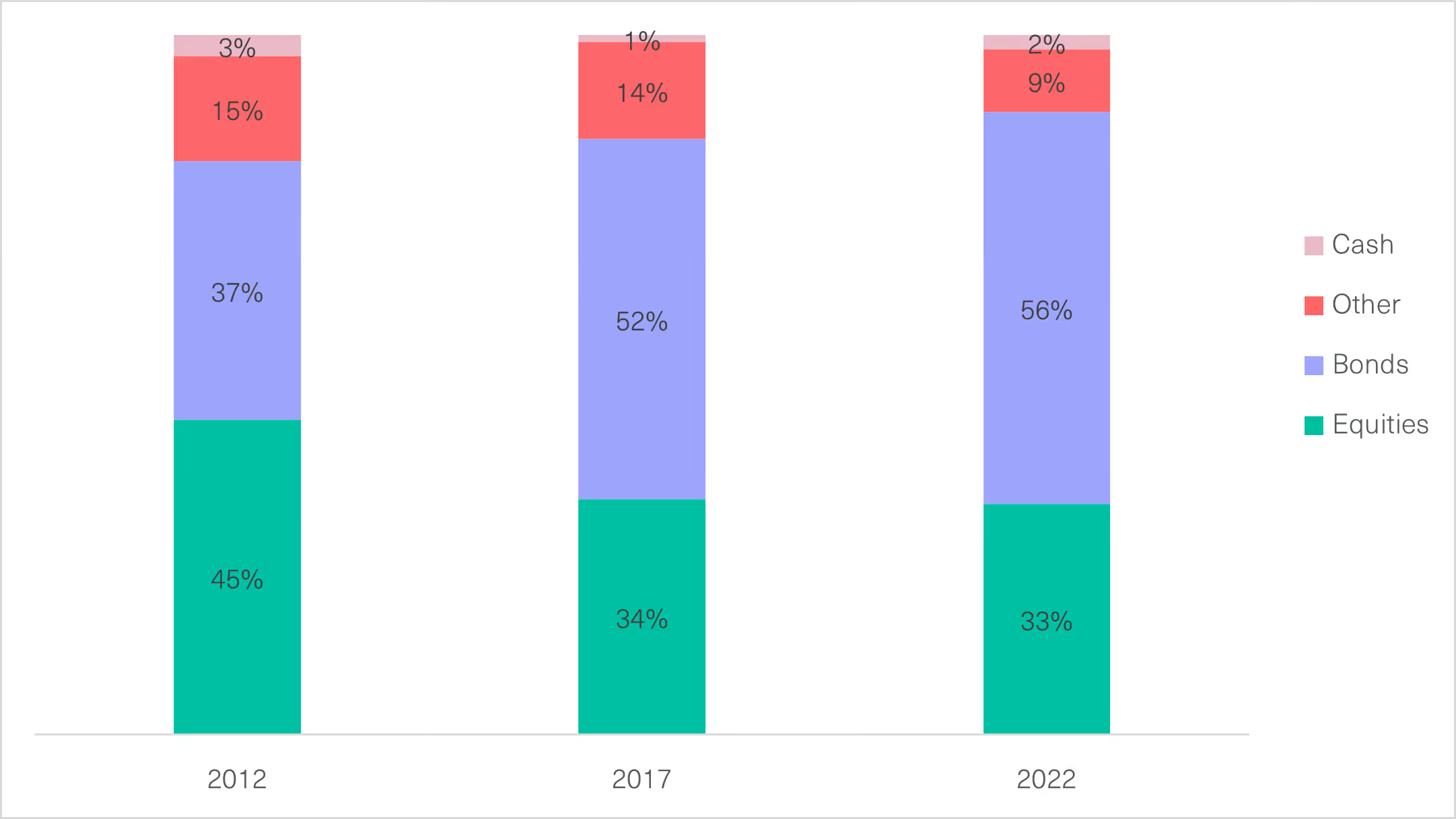

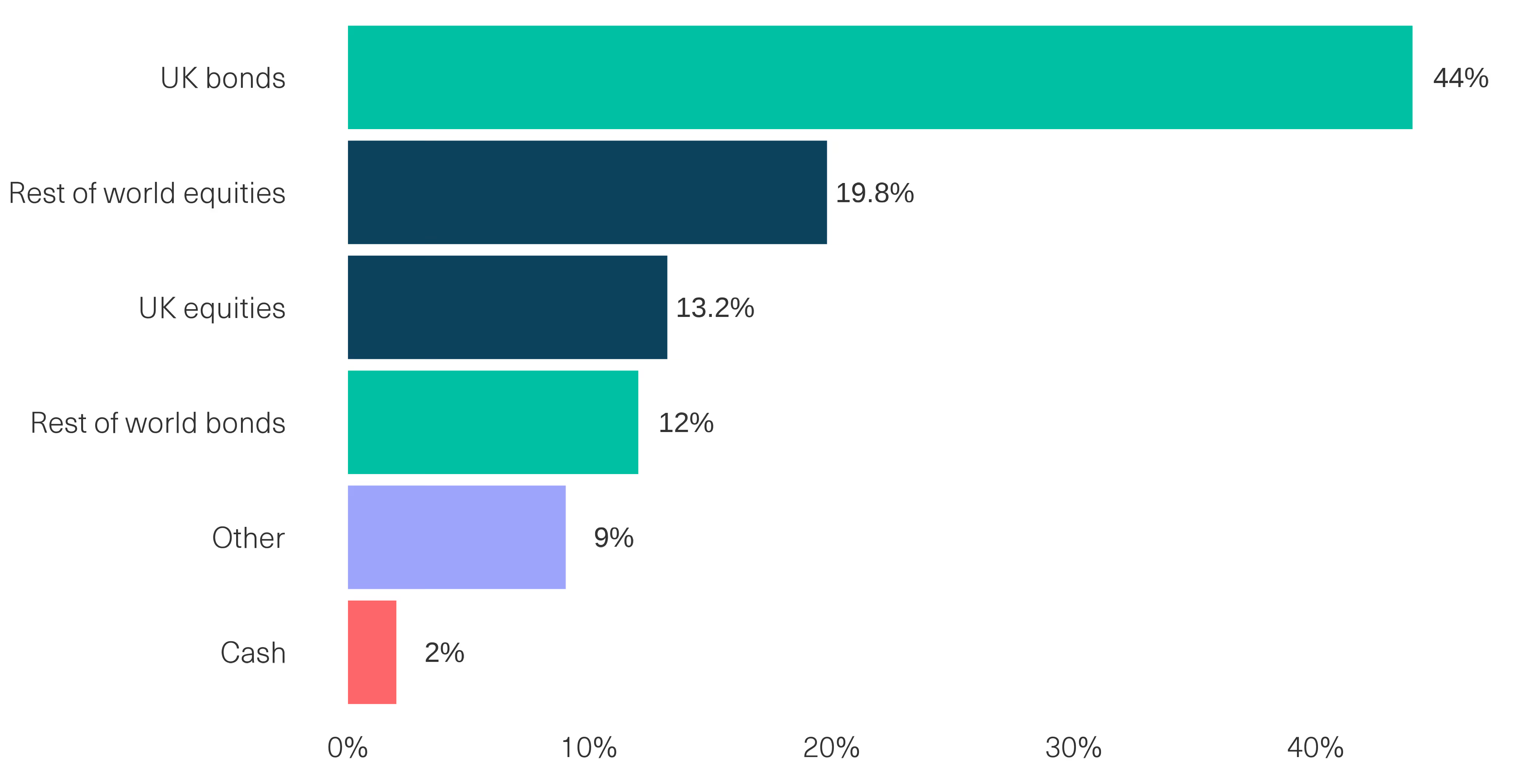

Taking UK pension portfolios as a whole (both DB and DC), exposure to UK equities sits at the intersection of two striking trends over the last two decades or longer: declining equity exposure, and declining “home bias” within their equity allocation. As per the most recent Global Pension Assets Study from the Thinking Ahead Institute, aggregate exposure to equities was 33%, down 12 percentage points from 45% as of 2012. 56% was allocated to bonds and the remainder to cash and other forms of investment (Figure 1). Meanwhile, their holdings of domestic equities fell from approximately 70% of their overall equity allocation in 1999 to roughly 35% by 2016, stabilising thereafter and rising to 40% in 2022. Taking these two figures together, UK pension fund exposure to UK-listed equities — that is, the firms that stand to be affected by policies such as a windfall or buyback tax — sits at roughly 13% (see Figure 2).

[.fig][.fig-title]Figure 1: UK Pension Fund Allocation Over the Last Ten Years (DB and DC)[.fig-title][.fig]

[.notes]Source: Common Wealth based on Thinking Ahead Institute[.notes]

[.fig][.fig-title]Figure 2: UK Combined DB and DC Pension Fund Allocation, 2022[.fig-title][.fig]

[.notes]Source: Common Wealth based on Thinking Ahead Institute[.notes]

How does this translate to exposure to any given UK public company, namely the oil majors at the centre of this debate? If we assume that pension funds allocate roughly in keeping with the relative size of companies in an index or a market, then based on Shell and BP’s relative positions in the FTSE All Share (the index of all companies listed on the London Stock Exchange), UK pension funds’ exposure to these two firms would be approximately 0.9% and 0.5% of their aggregate portfolios, respectively, for a combined allocation of 1.4% (see Table 1, below). [1]

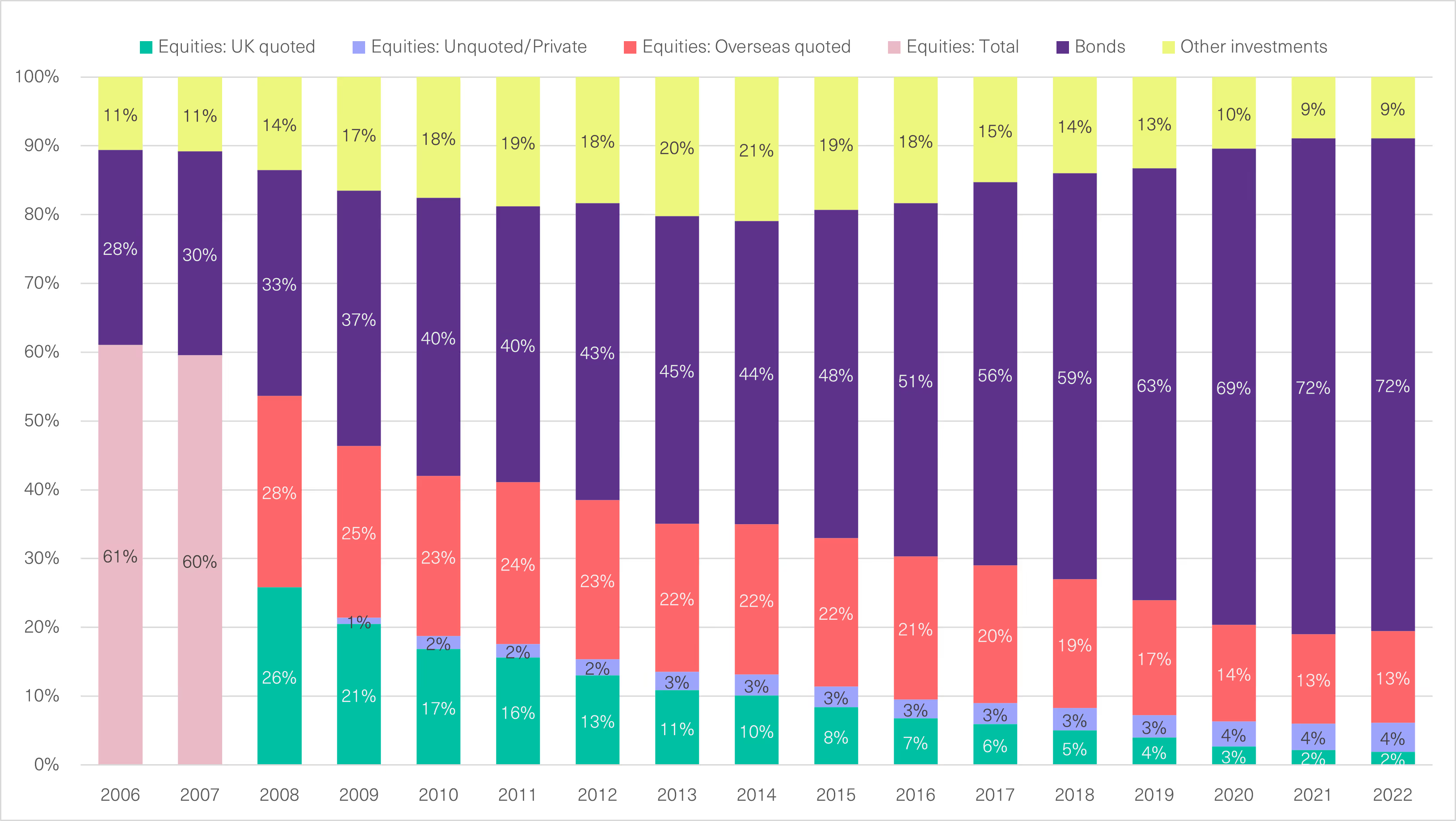

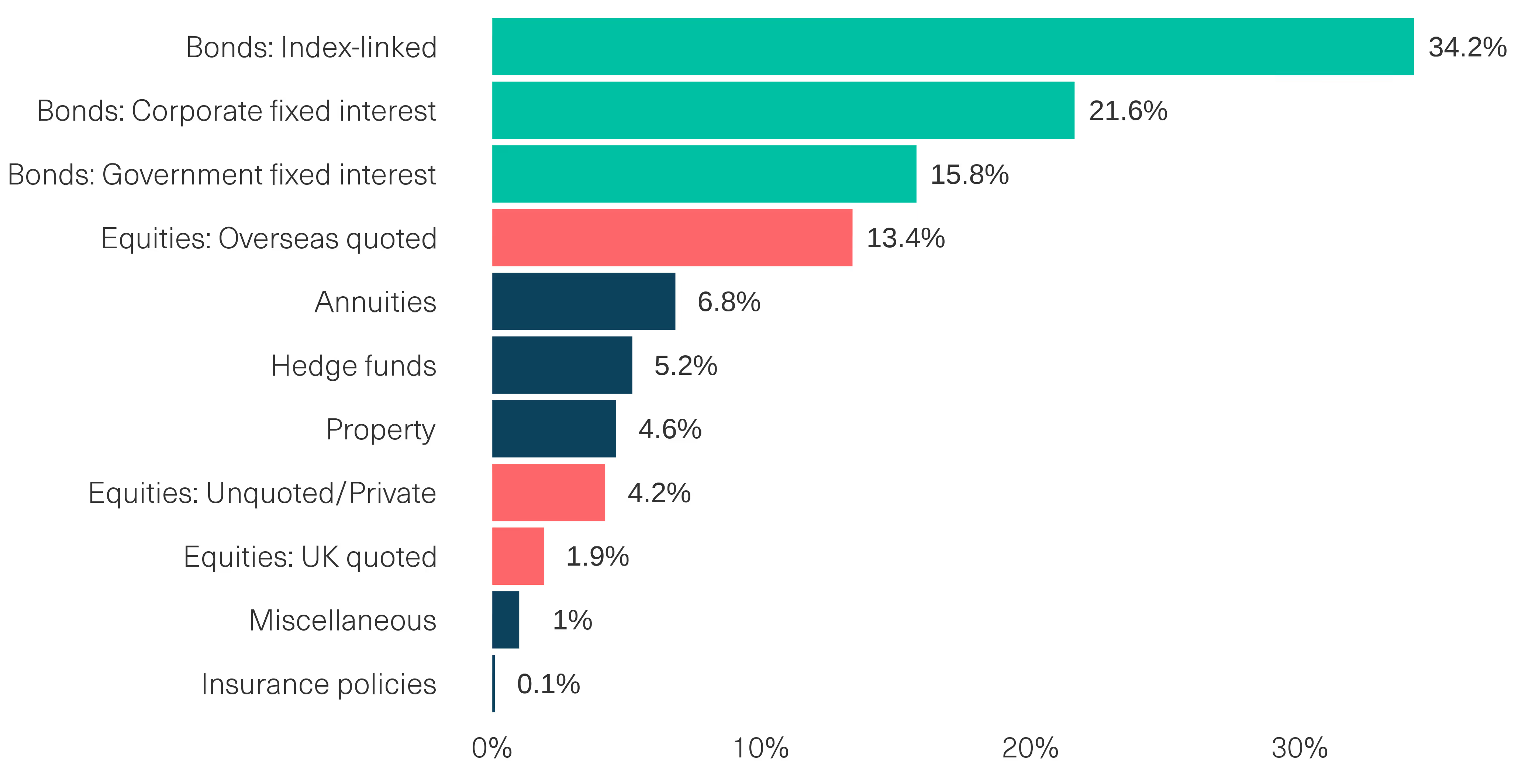

For DB pensions in particular, allocation to equities is just 19.5% — down markedly from 61% in 2006 (see Figure 3). DB fund allocation to UK-listed equities in particular is just 1.9% (Figure 4). Thus, by the same calculation as above, the average DB portfolio would have exposure to Shell and BP of just 0.13% and 0.07% respectively — a small fraction of their total assets. Critically, despite the ongoing closure of many DB schemes to new entrants and to additional accrual, DB pensions still hold 81% of UK pension assets, meaning the vast majority of pension assets are in schemes that conform more closely to this allocative breakdown.

[.fig][.fig-title]Figure 3: UK Defined Benefit Pension Fund Allocation, 2008-22[.fig-title][.fig]

[.notes]Source: Common Wealth based on Pension Protection Fund[.notes]

[.fig][.fig-title]Figure 4: UK Defined Benefit Pension Fund Detailed Allocation Breakdown, 2022[.fig-title][.fig]

[.notes]Note: Values do not sum to 100% because of 8.8% cash deficit. Source: Common Wealth based on Pension Protection Fund[.notes]

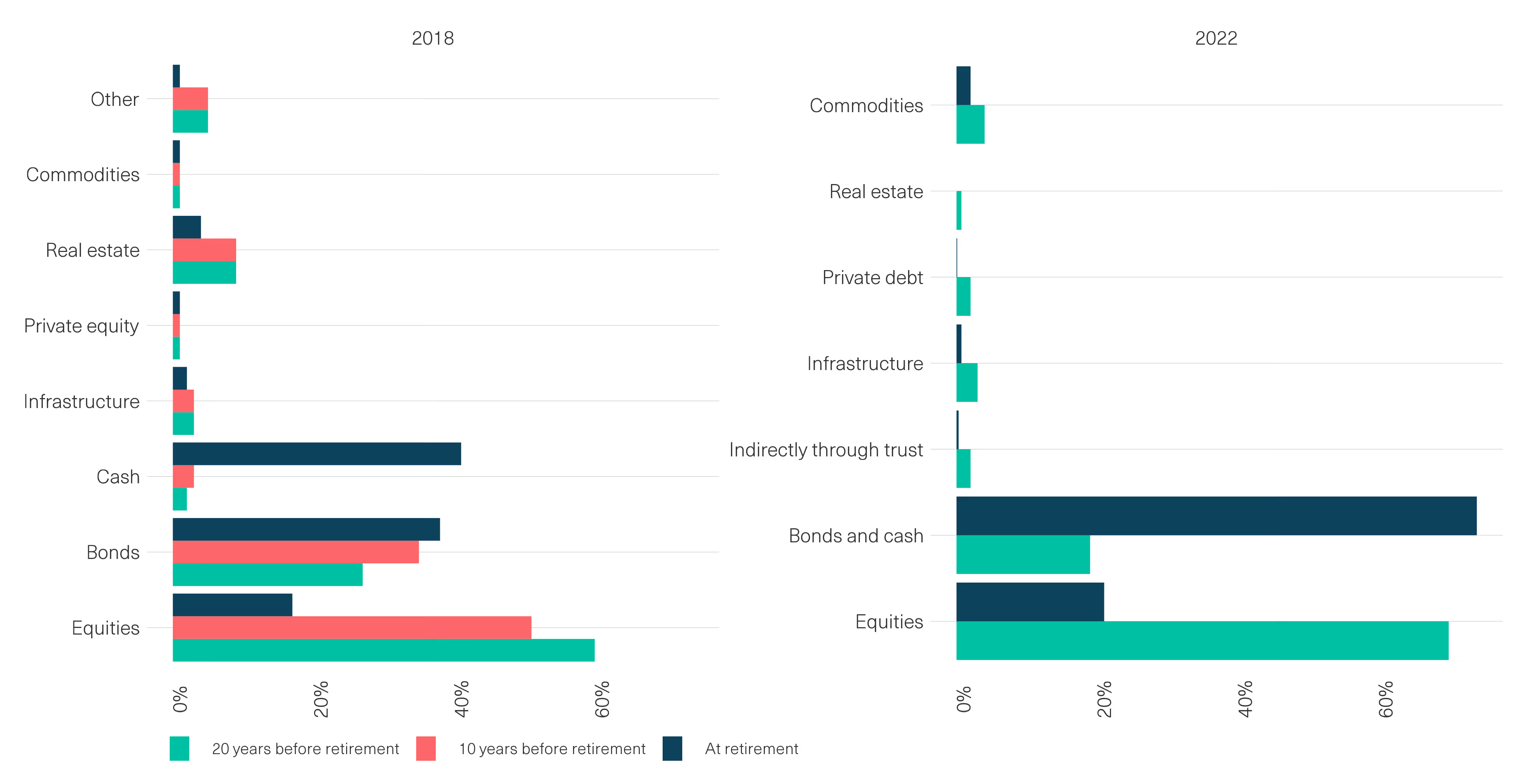

Demographic differences help to explain the drop in exposure to UK-listed equities between DB pensions specifically and UK pension schemes as a whole (both DB and DC). DB pension schemes in the UK tend to skew toward older participants, in part because many DB schemes have closed to new entrants or additional benefit accrual. According to the most recent figures from the Pension Protection Fund, 43% of members of DB pension participants are already receiving pension payouts, with just 10% still actively contributing and accruing benefits. [2] Because individual portfolios pivot over the life cycle away from high-risk high-return assets during the earlier accumulation stage to lower-risk instruments as the payoff period approaches, allocation tends to move away from equities as a beneficiary ages and toward lower-risk bonds. In general, the greater the urgency, the lower the exposure. (Figure 5, below, illustrates this life cycle dynamic starkly for a snapshot of DC portfolios.)

We note that while the Pension Protection Fund publishes a dataset specific to DB pensions, an equivalent publication for the DC sector is not publicly available [3] and available timely estimates are partial. This is particularly important because it is DC schemes where the return on the portfolio does dictate retirement income, such the payouts of Big Oil companies are more consequential for the beneficiary. Chiefly, a study by the Pensions Policy Institute found that “master trust” DC pensions in the UK — which, we calculate, control over three quarters of DC assets — allocate approximately 18% of assets to UK equities for beneficiaries twenty years away from retirement, [4] with this allocation falling steeply over subsequent years until retirement. These figures provide only a snapshot for a particular age of pension contributor, but imply an average DC fund exposure to Shell and BP of 1.9% at the twenty years from retirement mark (Table 1).

[.fig][.fig-title]Table 1: Estimated UK Pension Fund Allocation to Shell & BP, 2022[.fig-title][.fig]

[.notes]Note: *6.86% of FTSE All Share by market capitalisation. **3.63% of FTSE All Share by market capitalisation. ***Common Wealth calculation assuming geographical distribution of equity allocation is same before and upon retirement, and that all UK equities held are listed. Source: Common Wealth based on Thinking Ahead Institute, Pension Protection Fund, Pensions Policy Institute, Refinitiv[.notes]

[.fig][.fig-title]Figure 5: DC Portfolio Allocation at Retirement Vs 20 Years Prior[.fig-title][.fig]

[.notes]Source: Pensions Policy Institute[.notes]

Thus, whichever way you slice UK pension allocation, the first premise on which the argument against windfall taxes and other interventions often rests — that the companies in the sightlines of these policies constitute a major portion of UK pension portfolios — is difficult to defend.

Some argue that the low average exposure we describe above might obscure high exposure among a small number of specific funds or pots, for instance an early-stage DC pot. Even if we then to the extent that a tax on supernormal profits is a tax on supernormal pension returns, a windfall tax is just that: the elimination of a windfall rather than the active inflicting of damage. Moreover, portfolio returns is a function not just of the rate of return, but of the size of the portfolio, determined in turn by the size of contributions. Evidence is beginning to emerge that contributions are faltering under the strain of the cost of living crisis, with many employees requesting to reduce their contributions or cease them altogether, and others drawing down savings prematurely to meet their needs.

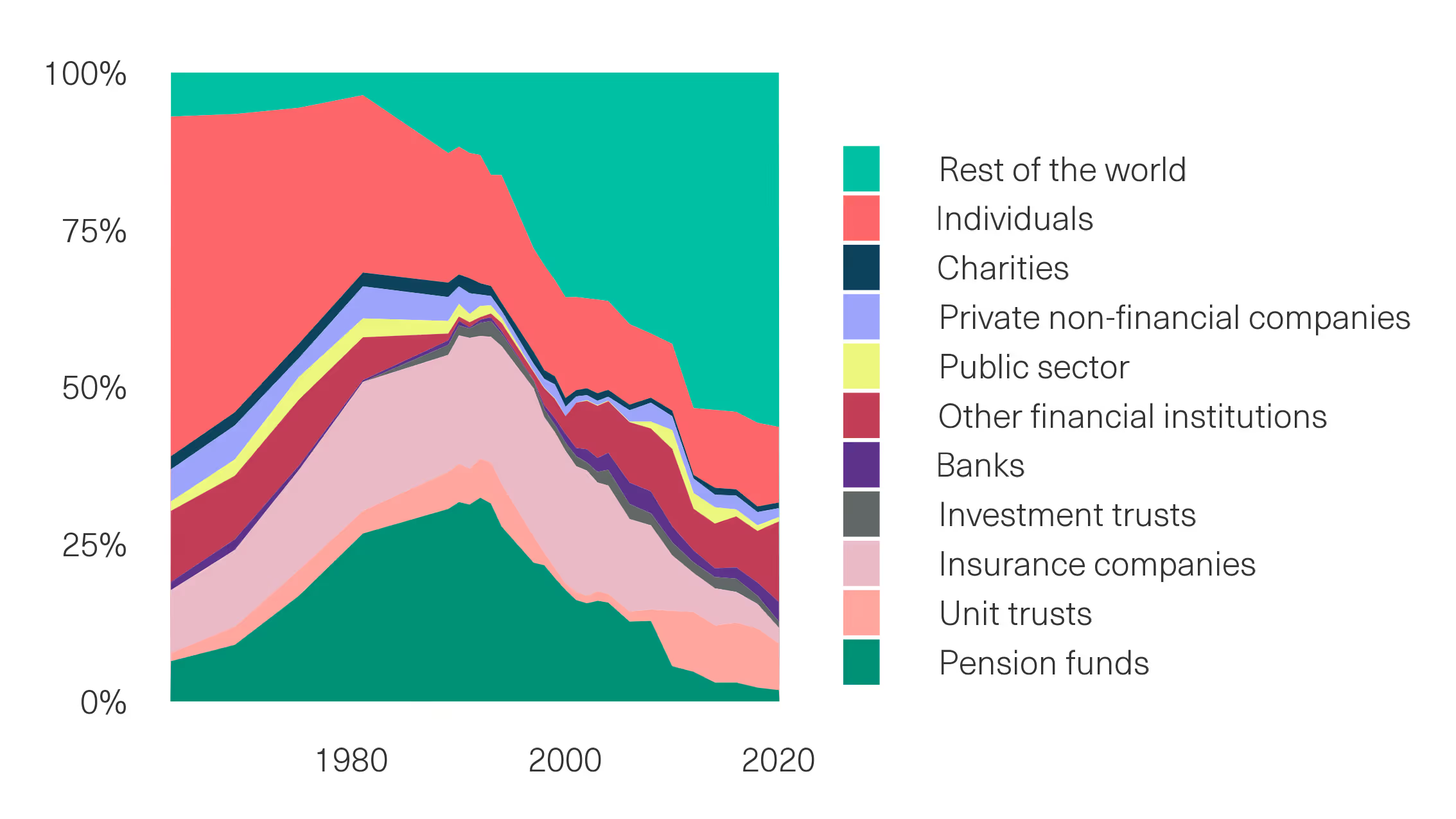

What, then, should we make of the second premise: that UK pension funds are major shareholders in UK-listed firms? Here, again, a brief survey of available data paints a different picture. In our recent report with the TUC and High Pay Centre based on a new dataset from the Office for National Statistics, we highlighted how the proportion of UK shares directly held by UK pension funds fell from almost one in three in 1990 to less than one in 25 by 2018, representing a decline of over 90%.

[.fig][.fig-title]Figure 6: Who Owns UK Quoted Shares? 1963-2020[.fig-title][.fig]

[.notes]Source: Common Wealth representation of data from ONS[.notes]

Granted, investment strategies have changed significantly over this period. Up until the late 1990s, pension funds often invested directly as shareholders. Today, many pension funds instead allocate their assets via asset manager intermediaries, with the result that the size of pension funds’ stakes in these firms is underestimated by Figure 6, above. To address this, the same report estimated that UK pensions together own less than 6% of all UK shares whether directly or indirectly through intermediaries. Of this total, we calculate an upper bound of 69% is attributable to DC schemes, assuming that the 18% UK equity exposure is entirely to listed stocks.

The ONS data does not appear to confirm suspicions that pensions’ equity exposure skews towards so called “large cap” firms such as BP and Shell. UK pension funds directly own FTSE 100 stock in exactly the proportion as they do other smaller companies (1.8%), likewise the insurance companies through which some individuals may invest self-administered pensions. Unit trusts and investment trusts skew more towards smaller companies.

Importantly, the decline of UK pension funds’ direct ownership of UK equities has come with a major internationalisation of UK share ownership, with “Rest of World” accounting for more than half of all UK share ownership by 2020 (and skewing more towards the large caps), as shown in the chart above. To be clear, even among domestic owners only, the pension sector’s decline is dramatic.

Taken together, it is clear that UK pension funds are, collectively, small minority shareholders in UK plc, undermining the second premise of the original argument. Indeed, no matter which end of the telescope one looks through, the picture is one of increasing diversification, both of pension portfolios and of the shareholder structure of major firms.

However, even if both the above premises held, there is another critical issue too often ignored in the debate over these policies: the question of how pension assets themselves are distributed, and the implications of this distribution for the effectiveness and fairness of policies. The UK's private pensions replicate labour market inequalities by design. For DC schemes this is particularly acute, with the value of contributions pegged to a percentage of an individual’s salary. Thus, even where two colleagues in a company may both receive a 6% contribution from their employed, the lower-earning worker receives a proportionately smaller contribution than their higher paid colleague.

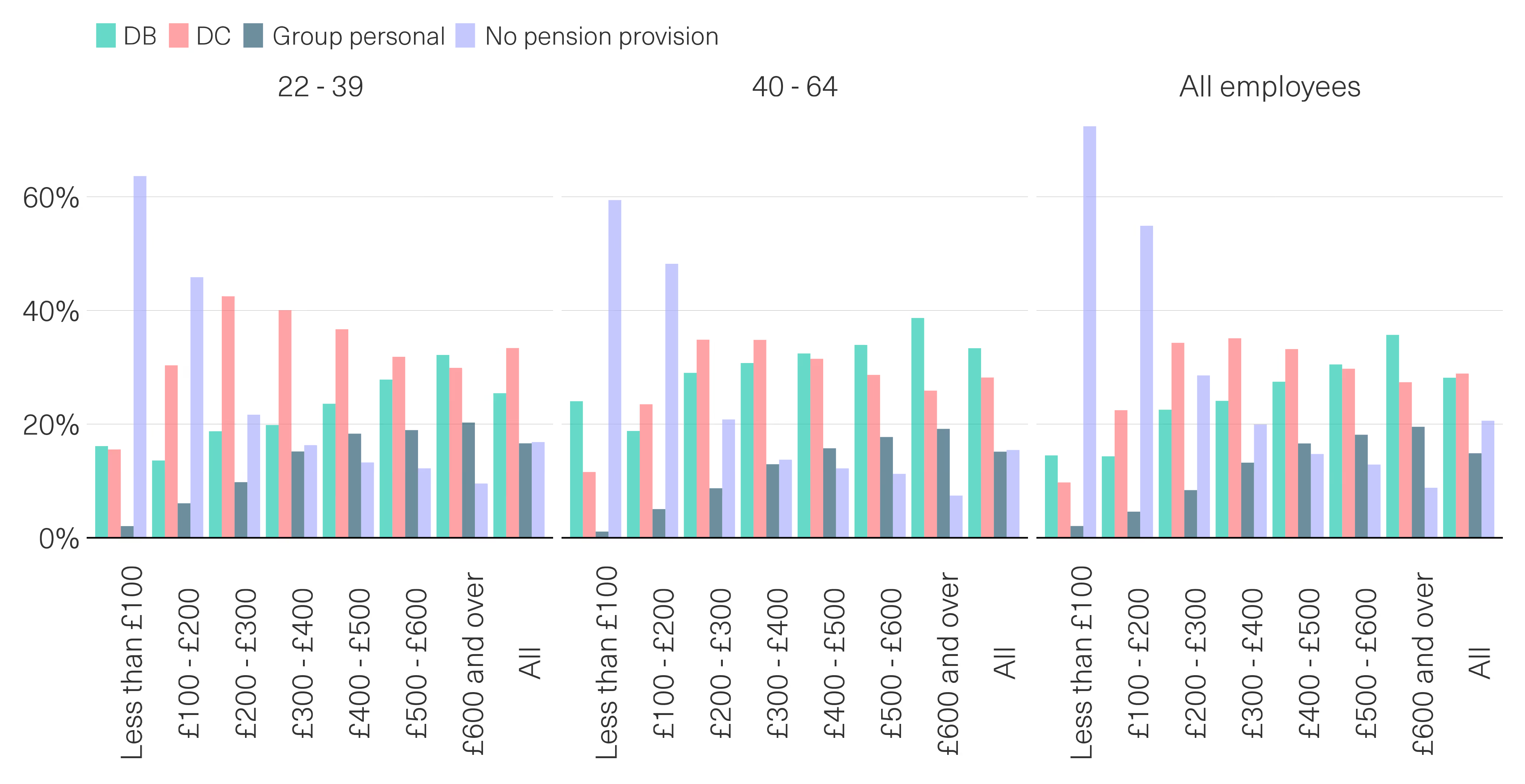

Figure 7 below compares the distributions of pension wealth by income decile, based on 2018 ONS data, the latest available for this statistic. Notably, the top 10% of UK households by income hold 30% of all private pension wealth. Nearly half of all UK pension wealth is held by those in the top two income deciles. This is on top of the £195 billion of UK share wealth directly owned by UK households, of which 39% is owned by the top 1% (by income). Combining these distributions, we calculate that the top decile’s share of both direct and pension-mediated UK equities is 35%. It should also be noted that one fifth of working age private sector employees — some 3.5 million people — do not make any pension saving in a given year, and this is particularly so for the lowest earners, who may fall below the threshold for auto-enrolment. (Figure 10 further illustrates the continuing prevalence of employees without pension provision.)

We note moreover that this highly unequal pattern is mirrored in other countries whose funded pension schemes are likely to own FTSE shares, such as notably the United States.

[.fig][.fig-title]Figure 7: Distribution of UK Private Pension Wealth by Income Decile, 2018[.fig-title][.fig]

[.notes]Source: Common Wealth representation of data from ONS[.notes]

When the UK population is instead broken down into deciles by wealth, the picture is even more stark: as of 2020, one tenth of the population held more in private pension wealth than the other 9 deciles together (Figure 8). [5] Shockingly, median pension wealth for the first three deciles was £0.

[.fig][.fig-title]Figure 8: Distribution of UK Private Pension Assets by Wealth Decile, 2020[.fig-title][.fig]

.avif)

[.notes]Source: Common Wealth based on ONS[.notes]

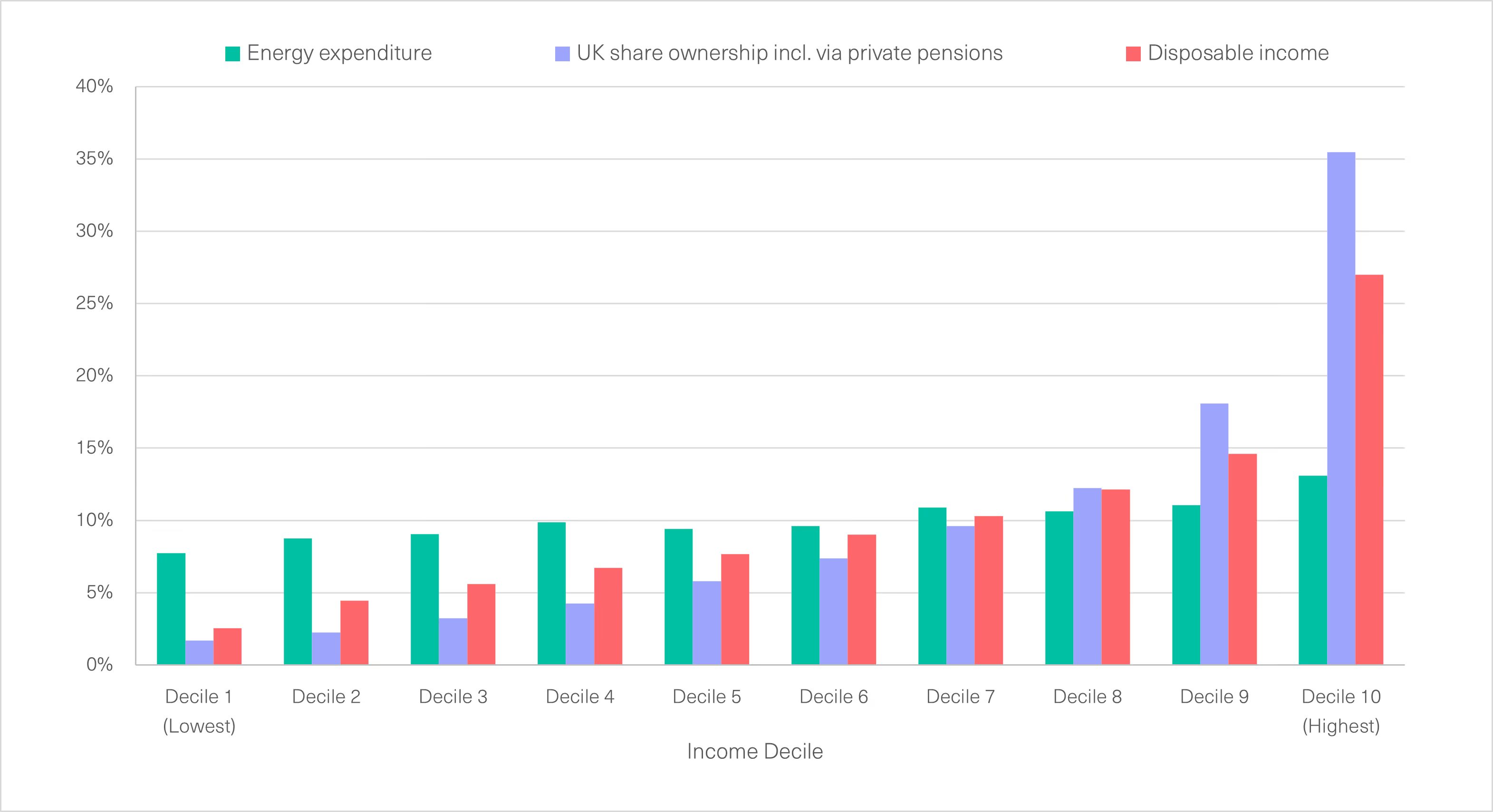

A rough calculation suggests that the average household in the highest income decile would have received a pension boost worth £55 from BP and Shell’s Q1 2023 payouts, versus £7 for a household in the poorest half (including those shares held indirectly by the scheme). The argument against a windfall tax or any other dampener on shareholder payouts for the sake of pensions implies a concern with the relative distributional implications of policy alternatives. Figure 9 below puts the highly unequal distribution of UK share ownership by income in context, including the equivalent distributions in disposable income (after benefits and taxes) and, crucially, household expenditure on electricity, gas and other fuel. [6] Viewed in this context, to argue that sky high shareholder payouts represent a more progressive distribution of cash than targeted support for energy bills funded by a windfall tax on the profits of oil and gas producers is inaccurate and unserious.

[.fig][.fig-title]Figure 9: Distribution of UK Private Pension and Shares Wealth, Disposable Income and Energy Expenditure by Income Decile[.fig-title][.fig]

[.notes]Note: Energy expenditure is for April 2019 to March 2020. Source: Common Wealth calculations based on ONS and Thinking Ahead Institute[.notes]

[.fig][.fig-title]Figure 10: Pension provision among employees by weekly earnings, 2021[.fig-title][.fig]

[.notes]Note: Excludes group self-invested personal pensions, group stakeholder pensions, and unknown pension provision, which together account for 7.4% of employees. Source: Common Wealth calculations based on ONS[.notes]

Furthermore, pension portfolios also include the securities of an array of other corporations, many of whom, in one way or another, form a major component of the oil majors’ customer base and whose margins — as our research with IPPR documented last year — are being squeezed by higher input costs on the one side and lower demand due to falling real household incomes on the other. Somehow, the lower return on these other equities fails to be invoked in the virtuous web of financial interconnectedness so lauded by the celebrants of Big Oil’s super-profits.

What remains of the argument with which we began — that dividends and stock buybacks pay our pensions and that, by extension, any policies to curb exceptional corporate profits or shareholder payouts are an attack on ordinary people’s incomes and long-term economic security?

To begin, it is worth separating out the implications of targeted versus general policies (i.e., a windfall tax on fossil fuel companies versus a generalised tax on dividends and buybacks), and the policy impacts for individuals versus pensions in the aggregate. The case against the target policy we have focused on here, namely a windfall tax on the UK profits of fossil fuel producers buckles fairly quickly under the weight of the evidence, both for individuals and for UK pension schemes in the aggregate. First and foremost, as we have shown using Shell and BP as proxies, the companies to whom this policy applies constitute a small fraction of UK pension fund assets overall. For DB schemes, the impact of reduced payouts is mostly relevant to overall financial stability of the fund, as by definition payouts to beneficiaries are pre-defined. Because DB schemes have much lower equities exposure overall than DC schemes, shareholder payouts are far less material to them than the performance of other forms of investment.

By contrast, in the case of DC schemes, reduced shareholder payouts in theory matter first and foremost to the individual beneficiary, whose payments from the scheme will vary based on the final value of their pot. Because exposure to equities falls over the lifetime of the average pension plan, the average profile of someone with high exposure to UK equities will be a younger individual in the early stages of a DC scheme, and therefore, likely, with a comparatively small pot. When combined with steep inequalities in the distribution of pension assets relative to income, the individualised impact of a hypothetical dip in supranormal shareholder payouts would likely be trivial for most, particularly those on lower incomes, particularly when compared with potential benefit of a well-designed windfall tax with progressive redistributive outcomes, for instance directly targeting energy costs, which could be profound.

It should also be emphasised that there is no guarantee that a windfall tax or comparable policy would have any impact on shareholder payouts. Notably, despite their being subject to the UK windfall tax, Shell and BP have maintained vast dividend and buyback programmes, including £8.2 billion in dividends and buybacks in Q1 2023 alone.

That said, while relatively low exposure to UK equities may insulate pensions from this kind of targeted policy, it does not necessarily insulate them from lower shareholder payouts in the aggregate. Changes to tax laws or corporate governance rules that decrease these across all sectors would undeniably be more significant to pension pots than a sector-specific policy, much more so for DC schemes.

Importantly, however, that such a policy would have a more substantial impact on DC pension participants constitutes a compelling argument against this kind of system, rather than a defence of it. Indeed, the arguments we have examined here point strongly toward more fundamental questions about the design of the UK pensions system. For instance, why tether an institution ostensibly meant to ensure economic security and dignity in old age to the whims and volatility of financial markets? Indeed, as commentators railing against the windfall tax themselves argued, falling shareholder payouts would not, for example, impact the guaranteed final salary pensions enjoyed by MPs. Instead, as the Institute for Fiscal Studies argues, while the ongoing transition to DC pensions may offer a greater degree of “flexibility” to participants, this comes at the rather significant cost of individualised risk: the risks of financial market downturns are no longer shared with one’s employer, other members of the scheme or other generations, but instead fall totally on the individual.

There are other reasons, too, why our financialised pensions are less than ideal. For instance, rather than encouraging investment, research for the Bank of England found that 80% of UK public companies cited financial market pressure for short-term shareholder returns as an obstacle for investment. [7] This pressure to “disgorge the cash” is also likely to affect wages, with the irony being that the argument for raising payouts “for the sake of pensions” could be directly applying downward pressure on the wages of the very same workers to whom those pensions belong. Though a causal link cannot be drawn, our research last year found that dividends at UK companies (not including buybacks) had grown six times faster than labour compensation between 2000 and 2019. For many, this is unlikely to be a worthwhile trade-off.

What, then, are the alternatives? This is a question of growing urgency for the UK economy, with commentators including Martin Wolf increasingly decrying the “crisis” of UK pensions. By Wolf’s account, the problem with UK pensions is that they are “incoherent, fragmented and risk-averse”, plagued by regulation that piles it into low-risk assets rather than higher-yielding investments such as venture capital or infrastructure. For him, the solution is to pool existing pensions into a small number of much larger DC funds and, crucially, to relax the rules around how pensions can and cannot invest to unleash this capital and enable larger returns. While this may address issues related to low returns, it addresses neither the fact that paltry DC pension pots will continue to leave many facing economic insecurity in retirement, nor that the liquidity constraints on DC schemes’ investment strategies are in large part inextricable from the flexible individualisation of provision. Nor does it consider, as Brett Christophers outlines, that pension funds are not necessarily the desirable “long term investor” for infrastructure projects that they are so often presented.

Others, like Benjamin Braun, advocate a more radical approach: the shift from funded pensions to a PAYGO system. Common across many European countries, a PAYGO system, Braun argues, “redistributes money from the young to the old, at a fraction of the cost of the pension-asset-management complex, and without demand-depressing, financialising consequences.”

What is clear is that for most, UK pensions currently fails on far more points than they succeed. The current system serves as a roadblock to urgently needed policies that could reduce inequality and drive forward the green transition; is increasingly threatening to or actually failing to meet people’s needs in old age; and drives forward a corporate governance regime so oriented around shareholder payouts that it erodes wages and productive investment.

To build an alternative we need to start from first principles, asking what pensions should do, rather than be constrained by how they are currently designed. There are many answers to this question, which we will explore in a programme of research over the coming year, but at the very least they should not serve as a smokescreen against much needed measures to end the cost-of-living crisis and building a fairer, more equitable economy.

[#fn1][1][#fn1] Based on Refinitiv Workspace index data as of 3 May 2023.

[#fn2][2][#fn2] The remaining 47% of pension participants are “‘Deferred”’ pension members, meaning those who are no longer accruing benefits in the scheme but who are not yet receiving payments from the scheme, for instance because they left service in the job with which the scheme was associated. Pension Protection Fund, “The Purple Book 2022”, December 2022 Available here.

[#fn3][3][#fn3] A 2016 estimate by Schroders, an investment management firm, suggested that DC pensions allocated roughly a quarter of their assets to UK equities, on average. Although their period documented unfortunately stretches only from March 2013 to 2016, they also observed similar twin trends of declining equity allocation and — from 2014 onwards — declining home bias. Available here.

[#fn4][4][#fn4] Those subsample of survey respondents who broke down their equity allocation geographically allocated 19% out of their 74% equity exposure to the UK. We apply the same geographical distribution to the larger sample of respondents’ smaller aggregate equity exposure to reach 18% for UK equities in aggregate.

[#fn5][5][#fn5] Note that sorting deciles by wealth rather than income places further up the distribution older people who have accumulated pension assets for longer, as ought to be expected.

[#fn6][6][#fn6] N.B. The distribution of share ownership does not consider the tax payable on dividend and buyback income received thanks to those shares (although these tax schedules are more regressive than that on labour income), whereas disposable income is net of tax and energy expenditure includes VAT. Unfortunately distributional data does not on energy expenditure since the energy crisis began, so we use 2019/20 data.

[#fn7][7][#fn7] Sir Jon Cunliffe, Are firms underinvesting – and if so why? Speech to the Greater Birmingham Chamber of Commerce, 17 February 2017. Available here.