Is the UK welfare system skewed toward its oldest citizens? It would not be unreasonable to think so. Analysis shows pensioners[1] were the only group to gain from the changes to working-age benefits and the state pension made by successive governments in the last decade.[2] Compared to 2010, pensioners now receive around £500 more per year in benefits, while £1500 per year has been cut from support for infants and children.[3] At the same time, policies with the potential for wide societal benefit and progressive distributional outcomes, such as windfall taxes, are often challenged, weakened or altogether abandoned on the basis that they will harm pension funds and pensioners’ incomes.[4] Importantly, these trends are more than just electorally motivated cynicism. They are also a result of the unique dysfunction built into the design of the UK’s pension system.

Far from gilded support, most people in the UK have very poor pension cover, and the distribution of pension assets is steeply unequal, with lower average cover for women and other disadvantaged groups. The vast, state-subsidised private pension assets built up by a rich minority are increasingly invested via globally diversified financial portfolios managed by third-party asset management firms, which invest on behalf of asset owners such as pension funds and charge often substantial fees for the service. In the process, these firms capture substantial rewards for themselves, boasting average profit margins of 35 per cent despite regularly failing to outperform market benchmarks.[5] The result is that rather than pensions investing directly and/or wholly into the UK economy — a concern the Chancellor has recently committed to address through the Mansion House Reforms[6] — this pool of money is distributed in pursuit of higher returns throughout the global economy, to the benefit of large investment firms. Indeed, far from simply allocating investment resources to maximise returns for members, asset managers impose a heavy cost on the pensions system. The large volumes and concentration of pension assets under management in the industry have also enabled leading asset management firms to accumulate significant influence over investment allocation, corporate governance, and even politics.[7]

Finally, the UK’s increasingly financialised pensions system reinforces financial instability and short-termism. By trying to fund pension provision through investments in financial markets, pension funds must prioritise the extractive principles of shareholder primacy and maximum returns while at the same time generating new risks, such as the “LDI crisis” that followed the UK’s Autumn 2022 mini-budget. Through this system, the wellbeing of pension holders — both those in receipt of payments and those still paying in — has become tethered to financial returns, placing both real and political restrictions on policymakers and pressure on firms and infrastructural projects to maximise profit and shareholder payouts, potentially to the detriment of service quality, real investment, wages, sustainability or other urgent demands.[8]

Resolving these problems means reckoning with two essential points. First, all pensions entail a cross-generational social and economic contract between employers, workers, residents and government to distribute money from those who currently work to those who no longer do so. How long people live after retirement, what costs people face as they age, and how well an economy performs over generational stretches all involve deeply uncertain projections about the long-term future and involve society-spanning challenges. There is nothing individualistic about these processes, which raises the second essential point about pensions: the risks associated with providing them are inherently collective, and therefore easiest to manage when shared collectively. As scholar Craig Berry states, “all forms of pensions provision are collective in practice”; our pensions system should reflect this.[9]

The incremental reformist agenda that has defined pension policy debate for the last three decades has failed to adequately engage with these two critical points. Decisions regarding distributional choices — which should be as transparent as possible, not least for the sake of democratic legitimacy — have been lost in the complexity of modern financial solutions. As key economic indicators have lagged — namely business investment, profitability, productivity and wages — asset managers have stepped forward as modern-day alchemists to promise the production of return from nothing. And critically, the narrative of “personal responsibility” has undermined the social contract, and in so doing has created serious problems concerning distributional justice.

This report explores several critical challenges gripping the UK pensions system and problems in its design, before making a series of recommendations for addressing these. With respect to more moderate and readily implementable incremental changes, these include:

More fundamentally, however, we question the justifications for and underlying principles of our prevailing approach to providing economic security and dignity in old age. In place of the inadequacy, instability and financialisation that defines the current model, we argue for a radical reimagining to build a system that is fit for purpose.

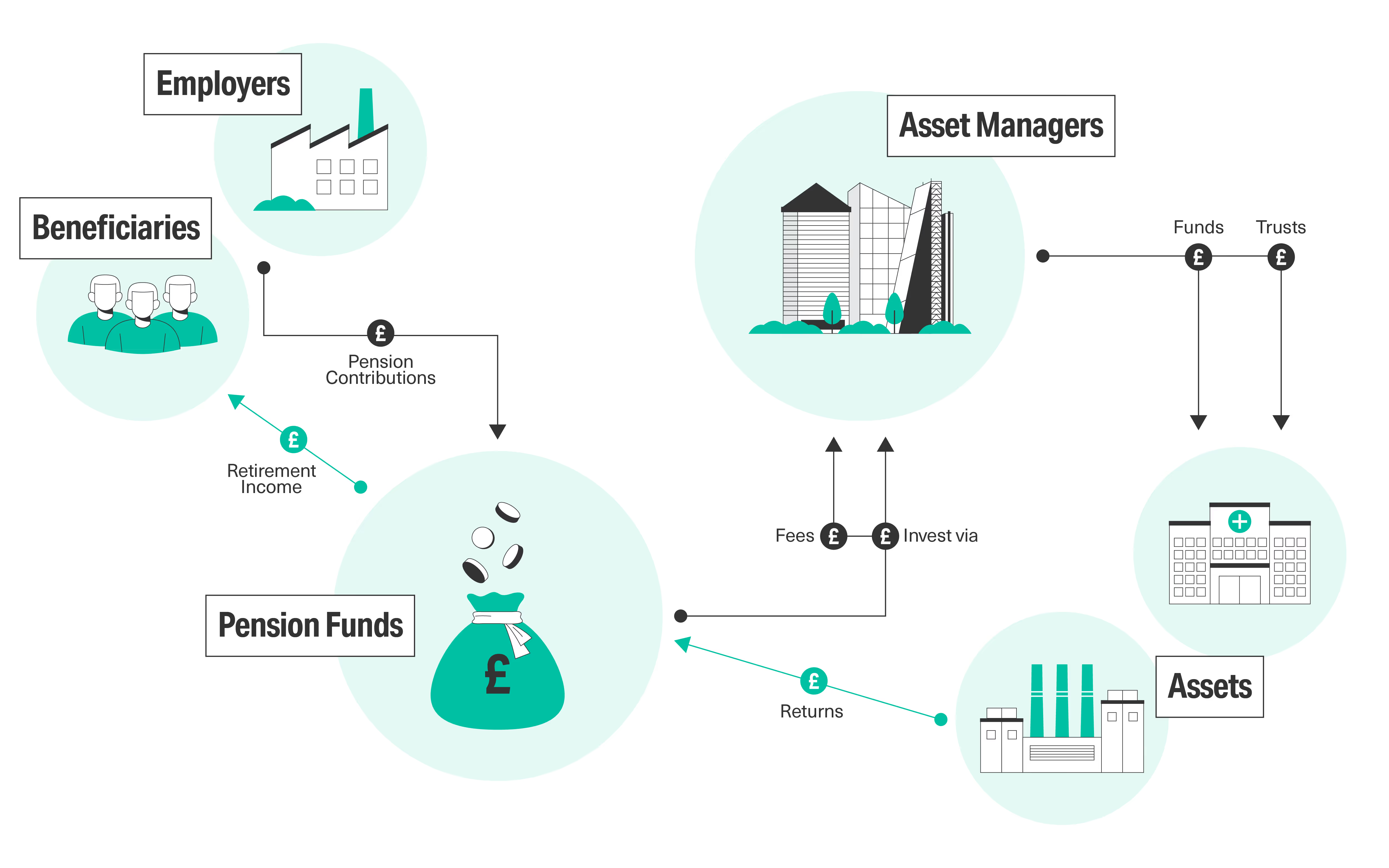

Pension provision in the UK involves several pillars, from public transfers to individuals with private pots. Here we consider two primary components: the state pension, which follows a “Pay-as-you-go” model in which current contributions (via National Insurance and other forms of taxation) finance current pension payments, and “occupational” or workplace pensions, which use what’s called a “funded” model.

[.fig]Figure 1: How Funded Pensions Work[.fig]

As the diagram above shows, under the “funded” approach, pension contributions are taken from workers’ pay in the form of deductions (visible on pay slips) before tax. Employers make additional contributions on top of salaries, set at an agreed percentage of a worker’s salary. Rather than using these income streams to directly finance pensions for current retirees, these contributions enter a pooled fund, where they are used to purchase financial assets. These assets then generate inflows to the fund, for example through dividends, interest payments on bonds, or capital gains from re-selling assets. In this way, the fund's assets are used to finance pension payments.

Occupational pensions can be divided into two main approaches. Defined Benefits (DB) pension schemes commit to provide members with a specific retirement income based on salary and years of membership. Defined Contributions (DC) schemes, by contrast, guarantee only the rate of contributions to be paid in by employees and employers, with the end benefit depending on the financial performance of the fund. Following the introduction of auto-enrolment in 2012, many more individuals have been enrolled into a DC pension, which has been driving an overall shift in the type of coverage people have from DB to DC schemes.

The UK is an international outlier in terms of the responsibility it places on the individual to secure their income in retirement.

The full UK state pension for 2023/24 is £203.85 per week, or just over £10,600 per year. To place this in context, the adequacy of retirement income can be measured in terms of a “replacement rate”, which compares a year of pension income with a year of average working age income (gross) prior to retirement.

Compared with many other countries, the UK has among the lowest replacement rates, with pension incomes averaging just over 20% of pre-retirement gross income.

[.fig]Figure 2: The UK Has One of the Lowest Replacement Rates Among Peer Countries[.fig]

[.notes]Note: Figures measured by the OECD as basic pension income as a proportion of average working income. Source: OECD.[.notes]

And, while many other countries also share the “multi-pillar” approach of both state benefits and occupational or private personal pensions, the UK stands out with respect to the very low income provided by the state pension, and thus our comparatively high dependence on other sources of income.

For reference, the Pensions and Lifetime Savings Association documentation on retirement living standards suggests that £12,800 p/a is the baseline for an absolute minimum living standard in retirement, and £23,300 p/a for a “moderate” living standard. Under current projections, just over half (51 per cent) of current workers (aged between 22 and retirement age) are not projected to achieve even the “moderate” retirement living standard. Over four million of those currently working are projected to fall below the minimum living standard.

Importantly, it should be noted that these projections are based on very optimistic assumptions. For example, in determining adequate standards of income, the assumption is also made that all people in retirement will be living rent and mortgage free. The actual picture is very different, and housing tenure is a key indicator in the likely adequacy of retirement income: one in four renters are projected to not meet minimum retirement living standards, compared to only eight per cent of owner-occupiers.

[.fig]Figure 3: Pensioners Receive Less Retirement Income from Public Transfers[.fig]

[.notes]Source: OECD. Note: 2018 data.[.notes]

When compared with peer countries, the UK’s direct government expenditure on pensions in 2019 (the most recent comparative data available) was relatively low, at just over 6% cent of GDP. However, rather than a reflection of cost-efficiency, this figure hides several other public costs required to sustain basic standards of living for many in retirement age. As measured by the Office for Budget Responsibility (OBR), these additional costs include Housing Benefit, Pension Credit and Winter Fuel Payments.

Pension Credit is a benefit for qualifying recipients who fall below a poverty line (for example because they do not qualify for the full state pension, which has strict rules related to the number of years an individual has paid in). Pension Credit in 2021 added a further £5 billion to the £104 billion in direct pension expenditure, while Housing Benefit for those over 65 was £6 billion, and Winter Fuel Payments £2 billion.

The costs associated with Housing Benefit are expected to rise due to changing patterns of home ownership for younger generations, with substantially fewer households at retirement age anticipated to be outright owners of their homes than today.

[.fig]Figure 4: The UK Spends Comparatively Little on the State Pension as a % of GDP[.fig]

[.notes]Source: OECD. Note: Comparative government expenditure on basic state pension (2019).[.notes]

However, by far the most significant cost beyond the state pension is the tax relief paid on pension contributions. In 2020/21, the net cost of this tax relief was estimated at £48.2 billion. Critically, the level of tax relief an individual receives is higher for higher income taxpayers and is therefore distributionally regressive by default. In a 2016 report, the Resolution Foundation calculated that 63 per cent of this relief went to the top fifteen per cent of tax earners.

Importantly, pension wealth in the UK is enormously unequally distributed, whether we consider distribution by wealth or by income decile (breaking the population down into ten groups). This inequality is a significant consequence of relying on occupational pensions to “top up” basic state pension provision, because occupational schemes reproduce and even exacerbate the income inequalities that exist between working-age people.

As the figures below highlight, median pension wealth for the top ten per cent (tenth decile) is about £550,000, with this decile owning around 60 per cent of the total. The corresponding figures for the middle (fifth) decile of the distribution are just £550 and three per cent. Even more strikingly, deciles one through four have zero median pension wealth and 0 per cent of the total. In other words, almost 40 per cent of the population has no (occupational) pension wealth at all.

[.fig]Figure 5.1: UK Pension Wealth is Very Unequally Distributed (Distribution by Income Decile, 2018)[.fig]

[.notes]Source: Common Wealth based on ONS.[.notes]

[.fig]Figure 5.2: UK Pension Wealth is Very Unequally Distributed (Distribution by Wealth Decile, 2020)[.fig]

[.notes]Source: Common Wealth based on ONS.[.notes]

The state pension is by nature highly redistributive. Because it does not attempt to replace earnings, the link between the size of contribution and benefit is loose, with the replacement rate higher for those who were on lower incomes prior to retirement. It has a credit system that allows those working outside the formal labour market on qualifying caring activities to build up national insurance contributions. By contrast, there is a much tighter link between contributions and benefits for occupational pensions, whether DB or DC. In short, those with higher incomes will make higher contributions, receive higher contributions from employers and have higher benefits.

Embedded social structures in the labour market, such as differences in pay between gendered and or racialised groups, are thus recreated at the level of retirement income. The nature of engagement with the formal labour market also affects access to occupational schemes. Employers only have to auto-enrol workers above a minimum level of pay; as a result, workers who engage in low paid work across several different jobs can therefore miss out and not receive employer contributions. Finally, those who are self-employed lose out on employer contributions and have substantially lower coverage than those with an employer, adding an extra dimension of concern for the growing adoption of “gig economy” norms across many sectors.

[.fig]Figure 6: Major Inequalities in Pension Wealth Persist Between Different Groups[.fig]

[.notes]Source: Authors’ elaboration based on ONS. Note: The figures show the median pension wealth for workers with current or retained rights in DC or DB pension schemes, by gender and by occupational social class (NS-SEC). Data for the latest round (2018-2020) in £.[.notes]

Finally, the ongoing shift from Defined Benefit to Defined Contribution pensions raises further concerns about economic insecurity in retirement for many, with pension benefits tethered to the performance of financial markets. As pensions try to meet demand for ever-higher returns, they have turned to financial products and management strategies from intermediary asset management firms, which comes at the cost of substantial fees. Recently, the Chancellor’s “Mansion House Reforms” have pledged to encourage large pension funds to invest in higher-return and higher-risk areas like private equity and venture capital, selling this as a "win-win" for pension-holders and for the British economy.

[.fig]Figure 7: UK Pension Fund Allocation Has Moved Substantially Over Time Away from Equities[.fig]

[.notes]Source: Authors’ elaboration. Note: Figures are expressed as percentages of total assets (net of derivatives). The 2018 gap and jump to subsequent years reflects a change in the survey methods by the ONS.[.notes]

However, there are serious reasons — explored in depth in the attached report — to question whether either outcome is likely as a result of these reforms. Instead, it’s likely the biggest beneficiaries of these changes will be asset managers themselves, whose principal clients are pension funds and who charge substantial fees for these “alternative” investment approaches.

As this report argues, a much bolder vision is required to transform the current system — which has inequality, instability and increasing insecurity for many in its blueprint — into one that can guarantee economic security and dignity for all in old age.

[#fn1][1][#fn1] Defined here as individuals currently in receipt of pension payments following retirement.

[#fn2][2][#fn2] Molly Broome, Sophie Hale, Nye Cominetti, Adam Corlett, Karl Handscomb, Louise Murphy, Hannah Slaughter & Lalitha Try, “An intergenerational audit for the UK”, Resolution Foundation, 2022, p.38.

[#fn3][3][#fn3] Ibid.

[#fn4][4][#fn4] Adrienne Buller and Chris Hayes, “Perspectives: Will Restraining Corporate Excess Harm Pensioners?”, Common Wealth, 23/05/23. Available here.

[#fn5][5][#fn5] Asset Management Market Study, Financial Market Authority, 2017, MS15/2.3, p.34.

[#fn6][6][#fn6] “Chancellor’s Mansion House Reforms to boost typical pension by over £1,000 a year”, HM Treasury, 10/17/2023. Available here.

[#fn7][7][#fn7] Adrienne Buller and Benjamin Braun, “Under New Management: Share Ownership and the Rise of UK Asset Manager Capitalism”, Common Wealth, 09/07/2021. Available here. Adrienne Buller, “The Limits of Privatized Climate Policy”, Dissent Magazine, 2022. Available here.

[#fn8][8][#fn8] Adrienne Buller and Chris Hayes, “Perspectives: Will Restraining Corporate Excess Harm Pensioners?”, Common Wealth, 23/05/23. Available here.

[#fn9][9][#fn9] Craig Berry, Pensions Imperilled: The Political Economy of Private Pensions Provision in the UK. Oxford University Press: 2021, p.37.