The return of Trump to office and the unraveling of Biden’s climate agenda demand a sober assessment of the latter’s structural limits, particularly as the Iran war and the market-driven buildout of electricity-intensive data centers reshape the domestic and global energy landscape. The Inflation Reduction Act’s central blind spot was the failure to reckon with the legacy of fracking and the extent to which it has fundamentally transformed the political economy of US energy governance. Fracking has altered foreign energy trade relations, diversified hydrocarbon commodity chains, and restructured onshore energy workforce dynamics, all of which have enabled fossil capital to thrive amidst growth in renewable energy. Joe Biden’s administration prioritized investments in renewable energy buildout and consumer demand, via things like rooftop solar subsidies and electric vehicle tax credits, in turn assuming that market-mediated capital reallocation was sufficient to slow down fossil fuel investments. Yet even as the administration pursued clean energy goals more aggressively than any of its predecessors, the oil and gas industry not only survived but became even more integral to both the domestic economy and global production and trade networks, despite employing a shrinking workforce.

If the decarbonization of the US economy is to proceed effectively and expediently, it is incumbent on green industrial planners to grapple with the extent to which the fracking boom has fundamentally reshaped the political-economic terrain on which any energy transition must develop. This briefing considers the shifting frontiers of fossil capital and what these mean for future green industrial planning. In particular, it assesses:

The sheer abundance of oil and gas reserves unleashed by fracking arrived at a time of sluggish growth in US energy demand. These constraints incentivized the development of new outlets for fossil fuel consumption, including the massive buildout of export-oriented crude oil and LNG infrastructure, as well as the further diversification of hydrocarbon commodity chains through an increased production of NGLs, which are feedstock for plastics.

The fossil fuel industry was able to circumvent the formidable efforts at capital reallocation pursued by President Biden’s climate agenda. Not only did industry executives successfully lobby against the imposition of more punitive measures, such as a carbon tax, but the industry as a whole ultimately stood to benefit from numerous aspects of the administration’s signature climate legislation, including the massive boost to 45Q carbon capture tax credits included in the 2022 Inflation Reduction Act and the Regional Clean Hydrogen Hub initiative.

Fossil fuel industry executives tout fracking as an economic blessing for rural America following the 2008 financial crisis. While it is true that fracking initially led to a sectoral spike in employment, it also signaled a massive increase in capital intensity which has since led to chronic job loss across the industry. Despite the relentless efforts of industry figures to portray decarbonization as a “jobs killer,” then, the truth is that the industry is already hemorrhaging its own workforce. Its grand promises to revitalize rural America have already been broken.

Investigation of these shifting frontiers points toward three interrelated policy interventions:

For a decarbonization policy framework to be effective, it must face fossil capital head-on. Above all, this entails a real plan for fossil fuel phaseout, one which does not rely on the whims of private energy firms and their investors but is instead durably accountable to socioecological needs both within and beyond the United States. Policy design must shift from disorderly, ineffective market-coordinated decarbonization policies to an integrated system of democratic planning anchored by tools of public ownership and investment.[6]

This briefing assesses the new frontiers of fossil capital across three sections.

First, it analyzes how fracking successfully circumvented two economic hindrances to its expansion — saturated domestic demand and renewable energy buildout — through the massive increase in exports of crude oil, LNG, and NGLs. From a decarbonization policy perspective, this substitution of exports for domestic consumption not only complicates national emissions reductions commitments, but also reveals the need to address new relationships of dependency fostered between the onshore oil and gas industry and developing countries.

Second, it shows how the onshore industry adapted to the Biden administration’s green industrial policy by intensifying investments in a variety of complementary or otherwise non-competitive hydrocarbon-based products, such as blue hydrogen and petrochemical feedstocks. Because the commodity chains of the latter are inherently intertwined with ongoing oil and gas development as a whole, they have made delinking US energy policy from fossil capital all the more difficult.

In addition to confronting fossil fuel supply chain disruptions caused by the US and Israel’s war against Iran, policymakers must now address the exorbitant power needs of the data center boom, which is mobilizing massive new investments in natural gas infrastructure.[7] Combined with the steady growth in petrochemical feedstock production — US ethylene production, for instance, has increased by over 50 percent since 2015, supported by over a dozen new ethylene cracker plants constructed across the country[8] — this fresh domestic source of demand is testament to the ability of fossil capital to thrive in spite of growth in wind and solar power. Not only will the fossil fuel industry continue to resist market pressures to contract (e.g., lobby vigorously against any new tax burdens) then but, moreover, such pressures often create new opportunities for investment, innovation and industrial symbiosis. The only chance to ensure fossil fuel production and investment decisions align with the goal of decarbonizing the US economy necessitates bringing them under public control.

Finally, this briefing shows how the growing precarity of oil and gas labor has counteracted any economic benefits attributable to sharp GDP growth in heavily fracked counties. Fracking has neither revitalized post-2008 rural America nor proven to be a durable jobs boom. Rather, it has hastened the transformation of rural energy communities into zones of extraction, doing nothing to address long-term trends of population loss, dwindling job opportunities and worsening health outcomes. At the policy level, these trends have unfortunately been exacerbated by the separation of public investments in clean energy from those in rural healthcare and education following the collapse of the Build Back Better proposal. A future decarbonization push must reverse this policy drift and recognize that industrial employment cannot be pursued at the expense of social reproduction, and hence that the energy and services sectors are deeply intertwined.

In the mid-2010s, a crisis of overproduction ricocheted across global energy markets. This was precipitated by the abundance of unconventional oil development in North America, compounded with falling demand in East Asia and OPEC’s decision to maintain output to protect its market share against the new American frackers.[9] Crude oil and natural gas prices fell sharply. Because they were some of the most costly producers in the world, onshore US oil and gas producers suffered a deluge of bankruptcies, sell-offs, and mergers and acquisitions. The US alone shed some 100,000 oil and gas jobs, with global industry job losses reaching a total of 250,000.[10] Much press coverage of the energy glut at the time chronicled nervous energy investors convening with producers in order to demand they “pump less and profit more.”[11]

Amidst the doldrums, President Obama repealed the crude oil export ban, first enacted under Jimmy Carter’s administration. While this provided little in the way of immediate relief to US producers, it portended a fundamental reorientation of the onshore oil and gas industry toward export markets in order to overcome sluggish growth in domestic demand and to make opportunistic, geopolitical use of the country’s newfound energy abundance.[12] A massive, highly integrated petrochemical industry has long allowed the United States to shape the global supply chains of refined petrochemical products. But what distinguished the industry’s recovery after the 2014–2016 glut was that the US became a critical supplier of both “raw” fossil fuels as well as petrochemical feedstocks to refineries abroad. Indeed, since the mid-2010s US frackers have powered a massive new global petrochemical buildout, feeding into it not only crude oil and natural gas but also the natural gas liquids (NGLs) that commingle with them underground, such as ethane, butane, and propane. Obama’s repeal of the crude oil export ban was but the first tremor of a much deeper seismic shift. Since then, the United States has become a net energy exporter for the first time since the mid-twentieth century,[13] and by far the largest exporter of NGLs in the world.[14]

Immediately after the export ban lift, analysts tended to downplay the effect it would have. Jason Bordoff, who served on the Obama administration’s Council on Environmental Quality from 2009 to 2013, for instance, insisted that its primary purpose was not to catalyze a new export market for US oil but simply allow the onshore industry to more quickly recover from the mid-2010s glut.[15] According to this rationale, lifting the ban would allow the WTI benchmark price used in the US to better adjust to price movements in the global oil trade, which was expected to recover faster than the high-cost onshore fracking industry. Put differently, the repeal was intended to increase energy prices — to thus bolster oil and gas companies at the expense of everyday Americans — which had previously been driven down because of stalled growth in global demand.

[.fig][.fig-title]Figure 1: The 2010s Explosion of US Energy and Feedstock Exports[.fig-title][.fig-subtitle]Monthly average exports of crude oil and NGLs (thousands of barrels per day) and LNGs (millions of cubic feet per day)[.fig-subtitle][.fig]

[.notes]Source: Energy Information Administration.[.notes]

As Figure 1 makes clear, the repeal of the ban did introduce a massive new US oil export market. A key reason for this is that the quality of fracked oil tends to be lighter and “sweeter” (with a lower sulfur content) than the grades of oil typically handled by legacy US refineries. As domestic supplies waned, particularly by the 1980s, the latter adopted special equipment like hydrocracker and coker units to refine foreign sources of crude oil, which are often heavier and more sour (and therefore cheaper). In turn, however, they have become less efficient at refining light, sweet crude than foreign refineries, which tend to lack these sophisticated facilities. As a result, the Permian Basin, for instance, sees a majority of its crude oil exported overseas, by way of the Corpus Christi and Houston petroleum hubs. As a volunteer at the Big Bend Conservation Alliance observed, fracking has not brought prosperity to West Texas so much as transformed the region into an “extraction colony for the fuel resources for the rest of the world.”[16] Nationwide, 4 million barrels of crude oil are daily exported by the US, or roughly 30 percent of total production.[17]

Beyond oil, the growth of US LNG exports has also been particularly remarkable, given both the extreme technological complexity of transporting liquefied natural gas across oceans, and the substantially higher costs of producing gas in the US versus elsewhere, such as in the Middle East. As mentioned above, geopolitics played an important role in making US LNG a reality. When the export market was still in its infancy, the first Donald Trump administration threatened an “all-out trade war” if the EU did not, among other things, commit to buying more LNG.[18] President Biden then found further incentive for boosting LNG exports after the Russian invasion of Ukraine and the subsequent “weaponization of economic dependencies.”[19] Support for LNG indeed became a controversial blight on Biden’s climate agenda, hanging over him up until the LNG export terminal permitting pause he ordered late in his tenure — an order immediately revoked upon Trump’s return to office.[20] In either case, the growth of LNG exports over this time period is truly astounding (see again Figure 1): from 51,342 million cubic feet (mcf) per month upon Trump’s first inauguration to 414,951 mcf in the month of his return to office.[21]

While the LNG trade has therefore become a topic of great controversy among climate progressives, much less noticed has been the fact that, right alongside it, NGL exports have also increased dramatically, by 1,500 percent between 2010 and 2023 (Figure 1).[22] NGL imports to Europe have somewhat stagnated since then, but the abundance of cheap US NGLs, in particular ethane, was nevertheless a critical offramp for American frackers away from the mid-2010s energy glut.[23] The US remains a major exporter of NGLs to Canada, Mexico, and India, and, most notably, it supplies 100 percent of China’s ethane imports, a trade relation that unsurprisingly has become increasingly tense in light of Trump’s tariff putsch last year.[24] As discussed below, while the emissions associated with the conversion of NGLs into petrochemicals are only a small fraction of those resulting from the consumption of fossil fuels in total, the production of the latter is typically needed in order to extract the former. Hence, documenting both the rising global demand for US LNG and NGLs is indispensable for understanding the changing nature of investments in oil and gas and in particular the enduring problem of “carbon lock-in.”[25]

Put differently, servicing export markets entails corresponding investments in domestic fossil fuel infrastructure. Huge growth in oil, gas, and NGL exports has thus meant not only more wells but also more pipelines, fractionation facilities, export terminals, processing plants, and so on. These fixed investments deepen the political-economic inertia working against decarbonization by increasing the pressure to secure returns against even more sunk costs. This is what precipitates carbon lock-in: unlike infrastructure components like power transformers and high-voltage transmission lines, which can be integrated into fossil-linked energy systems but can also support the expansion of solar and wind power, any realization of a return on the former infrastructural investments is far more narrowly tied to the extraction, processing, and eventual consumption of fossil fuels.

With respect to US decarbonization strategy, the increasing export dependency of the onshore oil and gas industry makes carbon accounting much messier. The Biden administration’s targeted focus on reducing domestic fossil fuel consumption — for instance through EV subsidies — has not destroyed demand for US oil and gas, so much as outsourced it through new energy (and NGL) export markets. Nation-bound emissions reductions commitments of a future industrial policy regime will risk continuing to obscure the extent to which the US economy still depends on fossil fuels.

As will be discussed in the next section, the nascent “hydrogen economy” promoted by President Biden, first under the Bipartisan Infrastructure Law and then further amplified through the Inflation Reduction Act, is perhaps the purest expression of this contradiction. The IRA’s expansion of 45Q carbon capture credits was a central plank of the Biden administration’s effort to avoid directly contesting the economic power of fossil capital, and to instead align its growth imperative with national decarbonization goals. This was (correctly) interpreted by the industry as a green light for more unconventional oil and gas development. At the same time, with domestic demand growth in question, this also meant that the 45Q boost — and in particular the eligibility to obtain the credit while deploying sequestered carbon in methods of “enhanced oil recovery,” such as through carbon dioxide flooding — effectively subsidized oil exports and, hence, helped reduce national emissions only by moving them offshore. With this in mind, the real decoupling of concern for future decarbonization strategists should not be GDP from national emissions, but rather domestic fossil fuel production from countries of consumption. It is indeed essential to address how declines in domestic fossil fuel use have often been compensated by an increase in energy exports.[26]

Clearly, real decarbonization of the US economy must cap and draw down the carbon emissions embodied in these export markets. These emissions are attached to substantial relations of dependency between onshore oil and gas producers and LNG, oil, and NGL consumers overseas. It is essential that an energy transition in the US does not only avoid undermining energy infrastructure development abroad but also signals a transition in these relationships toward sustainable forms of trade and development cooperation.

This challenge becomes all the more acute as many countries already appear to be reassessing their dependency on the geopolitical and economic volatility of LNG markets and seeking refuge in safer, more reliable means of power generation, such as solar panels. The US and Israel’s war against Iran has indeed brought these dynamics to a head: even as Trump anticipates that supply disruptions instigated by the war will strengthen US LNG exports, countries like Thailand, the Philippines, and South Korea are accelerating renewable power permitting to help wean themselves off the LNG trade in the long run.[27] To the chagrin of the current administration, reckless military adventurism is not scaring other countries into submission so much as forcing them to seek trade relations elsewhere in order to meet their energy needs — particularly with China.

Yet existing US trade relations need not wither away, nor is waging endless war to shore up fossil capital the only option to maintain them. Rather, their very existence ought to compel recognition of the internationalist implications of energy transition in the US (as in every country). This interdependency is an inescapable fact of a global economy composed of highly integrated production networks. There is simply no solution to climate change that is not internationalist in scope: carbon emitted anywhere is an impact felt everywhere.

Perhaps the most ironic consequence of the fracking boom has been the extent to which it has afforded the onshore oil and gas industry the opportunity to capture public resources and support ostensibly directed toward decarbonization. At the federal level, the industry’s campaign to greenwash fracking was deeply embraced by President Obama, for instance in his infamous endorsement of natural gas as a “bridge fuel” in the 2014 State of the Union Address.[28] According to his rather partial reasoning, America’s newfound abundance of natural gas need not contradict climate goals. Given its consumption is ostensibly cleaner than coal — that is, if one ignores the vastly underreported increases in methane emissions[29] — gas-fired power generation could reduce emissions by phasing out aging coal plants in the power sector and, accordingly, buy time for solar panels and wind turbines to become more cost-effective.[30] While this did indeed occur, with coal-to-gas substitution accounting for a substantial share of the decline in emissions in the power sector from 1990 to 2020,[31] this “bridge” has now been exhausted: efficiency gains have begun to flatten as there are fewer and fewer coal plants left to shutter. Furthermore, any future emissions reductions owed to gas-to-renewables substitution are now being threatened by unprecedented increase in power demand driven by the data center boom.[32]

The characterization of natural gas as a “bridge fuel” nevertheless found real policy force, informing the Clean Power Plan (CPP) finalized late in Obama’s tenure.[33] In particular, the CPP’s emissions rate targets implicitly encouraged short-term fuel switching toward natural gas, with the implicit expectation that renewable energy sources would begin to replace natural gas by around 2030, as costs declined further.[34] At the time hailed by The Guardian as the “US’s strongest ever climate action,”[35] its arbitration via executive action meant the Plan was immediately legally challenged by red states and eventually stayed by the Supreme Court in 2016. Ultimately, it was repealed and replaced by President Trump’s “Affordable Clean Energy” (ACE) plan, which restricted the authority of states to regulate emissions in the manner mandated by the CPP.[36] Trump’s replacement plan also lightened the performance standards for new coal plants to thresholds well beyond what they were actually emitting.[37]

In either case the onshore oil and gas industry has successfully maintained a flexible role for itself across a variety of energy policy agendas. More recently, two commodity chains have become increasingly essential to this flexibility: first, the production of ethylene and other plastics feedstocks from NGLs and, second, blue hydrogen, or hydrogen conventionally produced via steam methane reforming, but with its associated emissions (ostensibly) captured and sequestered underground. Global plastics demand,[38] alongside limited substitution possibilities in pharmaceuticals, electrical insulation, and materials coating, has long helped to justify onshore oil and gas development. The recent shift toward “clean” hydrogen production promoted by the Biden administration shaped the latest episode of fossil capital’s greenwashing campaign. Decarbonization strategists should expect that the political strategy of the onshore oil and gas industry will increasingly depend on both a beleaguered defense of the irreplaceability of various petrochemical products for critical industries like computing, electronics and healthcare and an active reshaping of the demands of an “energy transition” through industrial advocacy for blue hydrogen.[39]

These two commodity chains will be handled in turn. First, the rapid expansion of NGL production in the United States is one of the most significant and understated shifts resulting from the fracking boom. An abundance of NGLs was not a direct objective of the onshore industry so much as a geological coincidence: many of the nation’s shale plays contain a lot of “wet” gas, meaning that the gas commingles with large amounts of heavier hydrocarbons and in particular NGLs. Thus, as fracking increased the overall production of shale gas in the country, more NGLs were also produced. At the beginning of the boom, their commodification was severely restricted by the limited “takeaway capacity” — the pipelines and other infrastructure required to transport these products from wellhead to market. Given the high cost of other forms of transportation (such as trucking), it was usually much more economical to leave otherwise commodifiable NGLs in the gas stream, a process known as “rejection,” as it flows into interstate (natural gas) transmission pipeline systems.

As more NGL infrastructure was built out during the 2010s, however, the economic geography of petrochemical production in the US shifted somewhat. In particular, the abundance of ethane associated with fracked oil and gas in the US led to the construction of at least seven new ethylene crackers between 2015 and 2022.[40] These newer facilities are designed to take only or primarily ethane as a feedstock, as opposed to heavier hydrocarbons like naphtha, which are more commonly used (in addition to NGLs) in older facilities along the Gulf Coast.[41] This has shifted the attention of the export market away from heavier petrochemical feedstocks toward ethane supplied by the “wettest” natural gas regions in the country, including the Permian Basin and Eagle Ford Shale in Texas, as well as parts of the Utica and Marcellus Shales in Appalachia. Moreover, because ethane is so abundant and cheap in the US, the country’s petrochemical industry as a whole has gained a competitive edge in the global petrochemical feedstocks trade.[42]

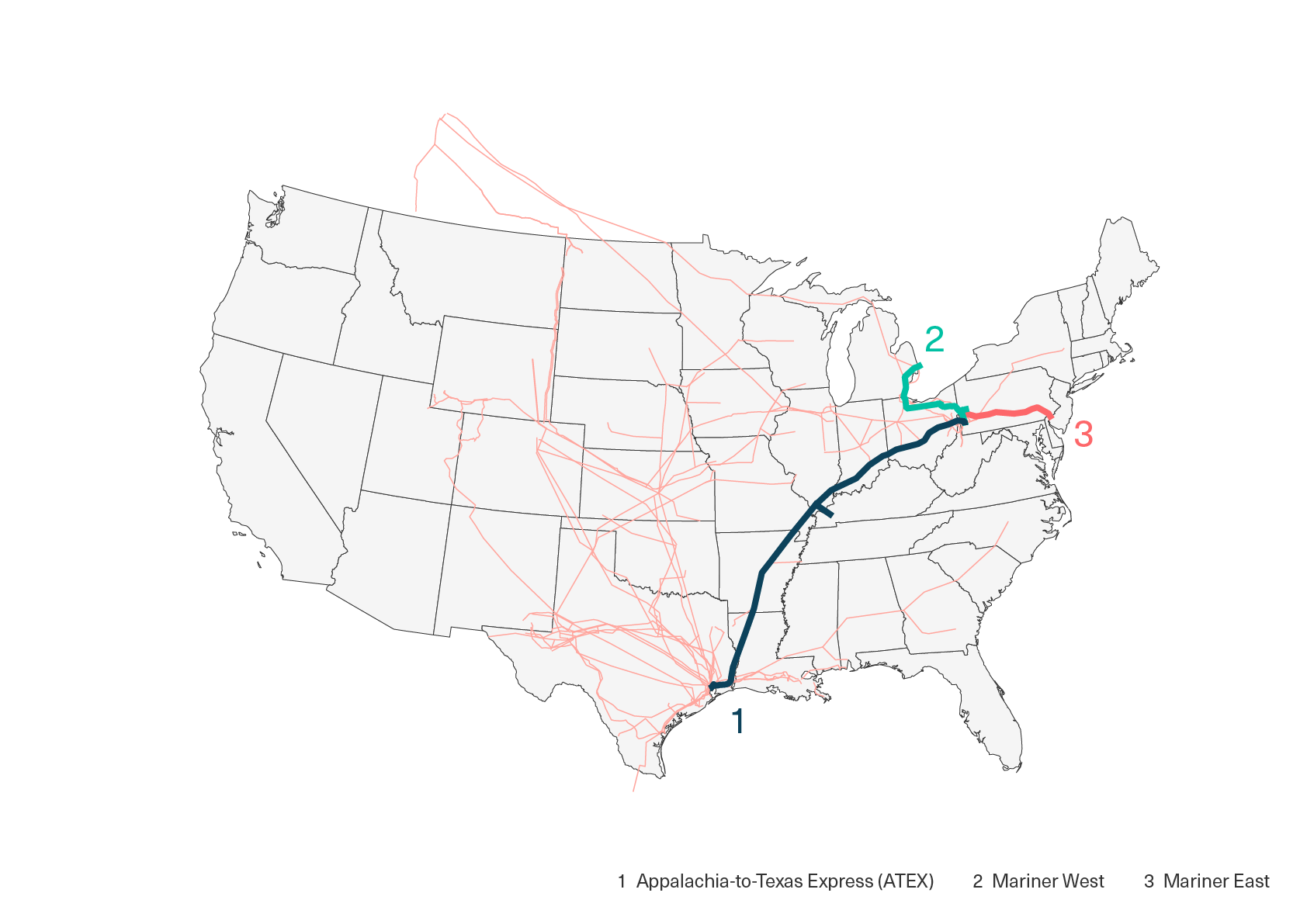

The construction of the massive Shell Pennsylvania Petrochemicals Complex in Beaver County, Pennsylvania, about 25 miles northwest of Pittsburgh, is one particularly notable consequence of this shift. Supported by a $1.65 billion tax break (the largest in Pennsylvania state history) it is by far the largest inland cracker plant in the country.[43] Even still, the bulk of refinement remains on the coasts, and Appalachia has thus seen much less petrochemical buildout than it has seen an expansion in NGL takeaway capacity, including the ATEX (Appalachia-to-Texas Express) pipeline system, which carries ethane from the Marcellus and Utica Shale region down to the NGL storage hub in Mt. Belvieu, Texas; the Mariner West pipeline, which transports Appalachian ethane into Ontario; and the Mariner East pipeline, which takes ethane into the Marcus Hook complex in eastern Pennsylvania (see Figure 2).

[.fig][.fig-title]Figure 2: NGL Pipeline Infrastructure[.fig-title][.fig-subtitle]Supply routes for petrochemical feedstocks to the global plastics industry, major Appalachian NGL pipelines highlighted[.fig-subtitle][.fig]

[.notes]Source: FracTracker.[.notes]

Through these pipelines, along with the many other systems spanning Texas and the Mid-Continent, the NGL feedstocks unlocked by the fracking boom have helped drive the global petrochemical buildout mentioned above.[44] Just as much as NGL exports, the problem of global plastic manufacturing likewise remains an understated point in US environmental policy discussions, which tend to narrowly focus on China as the world’s largest plastics producer.[45] The US continues to play an interdependent role in fueling the growth of new plastics demand abroad. Indeed, these dynamics persist in spite of the cooling of the global ethylene market since the early 2020s. The naphtha shortage caused by the US and Israel’s war against Iran, for instance, has recently pushed China to substitute its naphtha imports with even more US ethane, in turn allowing US exports to reach record highs.[46] Through the vicissitudes of petrochemical feedstock markets (and war), the US oil and gas industry has remained remarkably adept at securing avenues for profit.

Additionally, the tendency to reduce the climate crisis to the singular problem of carbon emissions obscures the relationship between ongoing onshore oil and gas development and rising global plastics demand. While it may be countered that focus on fossil fuels is warranted because the industrial processing of chemical and petrochemical products results in only a marginal proportion of global emissions (about 2.6 percent),[47] this ought to be challenged for two reasons. First, the process of refining constitutes a not-insignificant share of global carbon emissions and, precisely because of increasing demand for plastics, the volume of emissions associated with petrochemical manufacturing is expected to be one of the most significant drivers of industrial emissions in the US in the coming decades.[48]

Also, it is imperative for decarbonization strategists to address the plastics problem at the same time as fossil fuels, insofar as fossil capital is already leveraging the former’s absence in discussions of energy transition to deepen carbon lock-in. Indeed, insofar as satisfying global plastics demand means keeping the oil and gas industry as a whole profitable, it also means supporting the ongoing extraction of oil and gas in order to supply the requisite feedstock for the former. As the political economist Adam Hanieh has remarked, tackling the “petrochemical empire” is perhaps even more pernicious than tackling fossil fuels, for within it we are forced to confront the “basic materiality of our world,” which continues to rest upon petrochemical products.[49]

Increases in plastics manufacturing are coupled with another commodity pathway — hydrogen — which the onshore industry has been actively pursuing as a more direct political “derisking” strategy, in light of both the rising social opposition to fossil fuels and the encroachment of renewables into the power sector. It has long been recognized that many industrial sectors are not presently capable of eliminating their associated emissions through electrification alone, and in turn that wind and solar energy cannot serve as a 1:1 substitute for all fossil fuel inputs.[50]

[.box][.box-header]Obstacles to deep decarbonization[.box-header][.box-paragraph]Four of the most important hard-to-abate commodity chains also have a relatively high intensity of embodied carbon emissions: concrete, steel, plastics, and ammonia. Concrete is very difficult to decarbonize given the chemical reactions necessary for its production, which inherently release carbon dioxide. While steel production can be electrified, traditional iron smelting requires coke or coal as a means of reducing iron oxides, a process which likewise entails the release of carbon dioxide. The production of both plastics, as just reviewed, and ammonia, which is critical to modern fertilizers, also utilize hydrocarbons not just as a source of heat but as a feedstock, and hence they are likewise difficult to completely decarbonize.[.box-paragraph][.box]

The most prominent solution proposed to handle such hard-to-abate sectors revolves around replacing these remaining fossil fuel end uses with “clean” hydrogen.[51] Hydrogen is advantageous because it is capable of producing high-temperature process heat, and it can also be used as a feedstock for green steel and ammonia production. The Biden administration correctly identified the cultivation of a “hydrogen economy” as essential for industrial decarbonization, and policies to accomplish this were included both in the 2021 Infrastructure Investment and Jobs Act (IIJA) and the 2022 Inflation Reduction Act (IRA). First, the IIJA appropriated $8 billion for the development of a number of “Hydrogen Hubs” across the country. Subsequently, the IRA established Section 45V, a tiered tax credit for hydrogen production based on lifecycle emissions intensity.[52]

Nevertheless, the IRA’s aforementioned huge boost to 45Q carbon capture tax credits (from $17 to $85/ton for storage and $12 to $60/ton for EOR)[53] allowed the natural gas industry to take full advantage of large, uncapped subsidies to “blue” hydrogen. Tax incentives for blue hydrogen are critical for understanding why the onshore industry was so receptive to the IRA. To be sure, President Biden’s Department of Energy envisioned a host of regionalized “hydrogen economies” that were not completely dependent upon fossil fuels for hydrogen production but diversified in terms of both their sources of hydrogen as well as its end products.[54] Alongside blue hydrogen, the IIJA’s “Hydrogen Hub” program also deliberately targeted investments in green hydrogen and pink hydrogen.

But this source-agnostic approach to stimulating regional hydrogen economies implicitly favors legacy players and legacy infrastructures, for whom the cost to entry remains the lowest. Notwithstanding the questionable competitiveness of hydrogen in many of its proposed end uses,[56] these public investments have seen by far the most private investment in the lowest-risk, lowest-cost utilizations — most of which favor blue hydrogen. Exemplary are pilot projects made by pipeline operators intent on blending hydrogen, produced through steam methane reforming either on site or nearby, into existing natural gas streams.[57] This is a fossil fuel greenwashing move par excellence: on the one hand, the concentration of hydrogen necessary to meaningfully reduce carbon emissions is far higher than the low-percentage blends currently proposed, which are typically less than 20 percent. On the other hand, increasing the blend to higher concentrations will require either replacement or extensive retrofitting of existing natural gas pipeline systems in order to mitigate the corrosive properties and unique risks associated with the presence of so much hydrogen, such as embrittlement.[58] Efforts to develop regional hydrogen economies have not only been predominantly captured by fossil capital but, insofar as they remain left to existing markets to coordinate, are unlikely to actually bring about net emissions reductions.

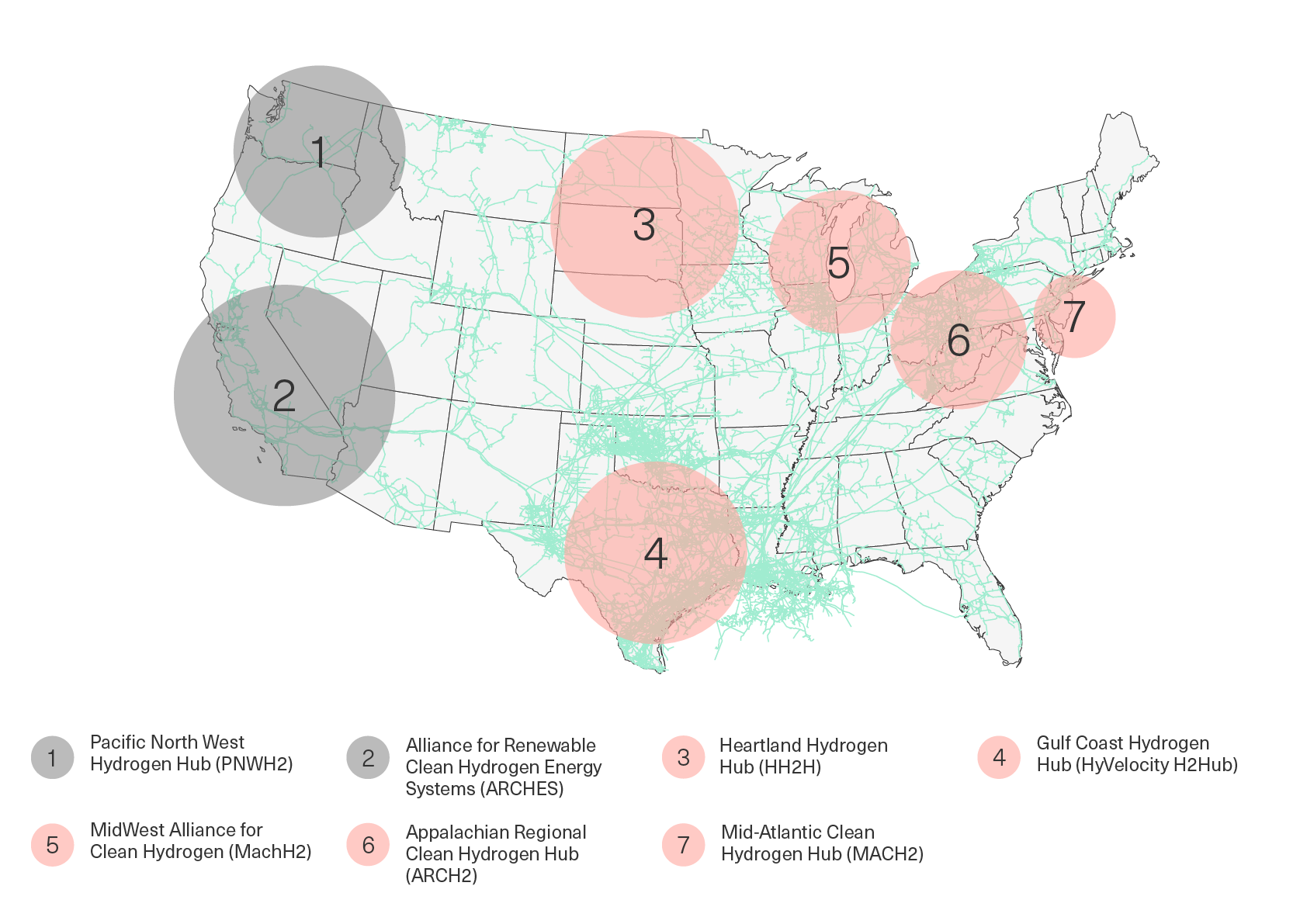

[.fig][.fig-title]Figure 3: Stacked Energy Landscapes in Rural America[.fig-title][.fig-subtitle]Proposed Hydrogen Hubs, superimposed above the existing US natural gas pipeline system[.fig-subtitle][.fig]

[.notes]Source: Department of Energy, FracTracker. Note: PNWH2 and ARCHES have been grayed out, as their IIJA funds have already been rescinded by the Trump Administration. See also: Tyler Harlan and Jennifer Baka, “Stacked energyscapes: Conceptualizing fossil fuel and renewable energy entanglements in low-carbon transitions”, Energy Research & Social Science, 2024, vol. 115, pp. 1-10.[.notes]

With Trump’s return to office in 2025, these contradictions have become more evident. Last summer, the Department of Energy initially proposed scaling back the Hydrogen Hub program, from seven hubs down to three, leaving only the Appalachian Regional Clean Hydrogen Hub, the Heartland Hydrogen Hub, and the Gulf Coast Hydrogen Hub, all of which are designed to take fossil fuels as their primary input (see Figure 3).[59] Then, last fall, the Department of Energy directly rescinded funding from two of the seven hubs: the Alliance for Renewable Clean Hydrogen Energy Systems (ARHCES) in California and the Pacific Northwest Hydrogen Hub (PNWH2),[60] with a DOE document reportedly circulating on Capitol Hill at the time suggesting the Department was preparing to cancel all remaining hubs.[61] Most recently, the Fiscal Year 2027 President’s Budget Request seeks to “permanently cancel” $3.25 billion of funding allocated by the IIJA’s Regional Hydrogen Hubs program and “repurpose” another $3.5 billion to support fossil fuel infrastructure (including coal) and artificial intelligence.[62] If last year’s One Big Beautiful Bill Act (OBBBA) is any indicator, the Republican Congress will likely oblige. While OBBA eviscerated many of the IRA’s investments in renewable energy and green infrastructure, 45V credits survived (albeit on a shortened schedule), and 45Q was expanded to bring EOR-utilized CO2 credits into parity with those for permanent geological storage.[63] Even if some hydrogen hub funding survives next year’s budget, then, this was already guaranteed to make clean sources of hydrogen, in particular electrolysis, even less competitive with fossil fuels.

Trump’s anti-green revanchism makes clear that the hydrogen push had primarily served as a hedge for the fossil fuel industry against the encroachment of renewable energy into the markets it dominates. In full compatibility with the exporting of fracked oil, gas and NGLs abroad and the associated investments in a global petrochemical boom, blue hydrogen has been a means by which the onshore US oil and gas industry has obfuscated its ongoing and indeed ever-expanding culpability for the climate crisis. Future decarbonization policy must support developing hydrogen to decarbonize hard-to-abate sectors. But market-mediated attempts to incentivize hydrogen development ignore that these relatively specialized end uses are unlikely to ever become either profitable or ubiquitous enough to support a full-fledged “hydrogen economy.” Once again there is a structural misalignment between the motivations of profit-seeking private capital investments and those of socioecological need. If hydrogen is to really assist in industrial decarbonization efforts, rather than simply serve as a hedge for fossil capital, it is imperative to bring decisions about its development under public control.

The recent push of AI data centers toward co-location with gas-fired power plants is the next frontier of these dynamics and will set the stage for any decarbonization strategy likely to be legislated and enacted by a progressive government in the 2030s. Stymied by yearslong queues to connect to regional electricity grids and an accelerating need for very large amounts of power beyond what renewable energy infrastructure can currently reliably provide, data center developers have increasingly looked toward behind-the-meter (and sometimes completely off-grid)[64] natural gas power generation as a near-term remedy.[65] This change in outlook for domestic natural gas consumption has been quite rapid: in 2025 alone, an additional 97 GW of gas-fired capacity has been proposed across the US strictly to power data centers.[66] This shift presents a potentially massive roadblock for future decarbonization efforts.

However, there are many reasons to be skeptical about the supposed extent of the data center boom. First, much of the planned capacity increases are motivated by big tech companies making interconnection requests at rates far greater than the data centers they actually end up building.[67] They do this for a variety of reasons, including to maintain bargaining leverage with utilities and to hedge development risks across multiple regions. Second, because this new demand has been increasingly met with newly proposed gas-fired power generation, gas turbine supply chains face huge bottlenecks, with utilities experiencing delivery backlogs extending to 2030.[68] This has forced developers to resort to more unorthodox approaches to supply power with very dubious prospects of long-term sustainability. For instance, some new project plans include repurposing large reciprocating natural-gas engines, traditionally used for backup power or peaking applications, for effectively continuous baseload power generation.[69] Third, a not insignificant amount of recent data center proposals are made by “colocators’, who supply cooling, power and network infrastructure to tenants, who then rent space in the data center and usually supply their own computing hardware. These marginal players, who are also often much more debt-burdened than hyperscalers like Google or Meta, maintain risky business models which may prove especially vulnerable if projected AI demand fails to materialize.[70] Finally local opposition to data center development is growing rapidly, already leading to 48 projects being stalled or blocked as of May 2026, in addition to construction moratorium proposals at municipal, county and state levels across the country.[71]

But even if the data center boom does fall short of current hopes, green industrial policymakers will still have to contend with the political-economic context already revealed by the utility- and grid-level response. Substantial load growth was going to be the case with or without data centers: deep decarbonization via industrial and mobility electrification implies not just switching out existing fossil fuel power generation for wind and solar but incremental power capacity growth and, accordingly, large new investments in grid infrastructure to support it. The data center boom has shown how woefully underprepared extant decarbonization policies were to accommodate this shift, inasmuch as one of the first major post-IRA tests of grid integrity has been met with rapidly increasing investments in behind-the-meter, gas-fired power generation. Future decarbonization efforts will be forced to grapple with two nascent faces of fossil capital at once: billions invested since the mid-2010s in export-oriented oil, LNG, and NGL infrastructure plus a looming risk of new domestic power needs, whether sourced through AI growth or simply industrial electrification, being met by burning more fossil fuels at home.

It is irresponsible to plan decarbonization around fluctuating energy needs beholden to unpredictable shifts in private capital allocation. Fifteen years ago, few “bridge fuel” climate boosters would have imagined having to contend with a robust US LNG market — which, as the Biden administration subsequently (and correctly) warned, would indeed drive up domestic energy costs.[72] Even fewer policymakers would have anticipated only a few years ago that data centers would now be at the forefront of a surge in domestic power demand after over a decade of the latter’s stagnation. Indeed, even after the arrival of ChatGPT model 3 upon which the upscaling of AI capital and data intensity has increased, the EIA’s 2025 Annual Energy Outlook continued to anticipate that US gas-fired generation would remain flat over the next decade.[73] Future policymakers simply cannot afford to once again be caught retrospectively bemoaning whatever new avenues of profit-making fossil capital manages to trailblaze in the coming decade. Decarbonization must involve the deliberate, coordinated phaseout of fossil fuel production and consumption.

The shale revolution is often portrayed as a godsend for rural America after the devastation brought by the 2008 recession.[74] Industry groups have touted the oil and gas sector as one of the most important employers in the country. The American Petroleum Institute (API), for instance, suggests that 10.8 million jobs, or 5.4 percent of total US employment, are “supported” by oil and gas.[75] This total is heavily inflated, as it includes millions of “induced” jobs only contingently (and hence by no means inherently) connected to oil and gas development, such as trucking and retail services. Removing these, the industry job total is closer to 2 million, half of which is comprised of low-wage gas station and convenience store attendants, which would not simply vanish with the electrification of the US fleet. As for the upstream sector more specifically, total core employment (NAICS 211) currently hovers around 120,000 jobs.[76]

That said, raw job counts do not encapsulate the full impact of the fracking boom on the labor market, which is better understood in terms of the effect of fracking and its corresponding technological improvements on the ratio of capital to labor expenditures. The onshore oil and gas industry has become much more capital intensive as a result of fracking, which has corresponded to large gains in labor productivity. In Ohio, for example, there were 59.5 oil and gas jobs per billion cubic feet (bcf) of natural gas extracted in 2008, the eve of the boom. By 2019, that number had fallen to less than three jobs per bcf.[77]

Capital intensity has allowed onshore oil and gas production to continue to increase despite declining job counts. As Figures 4 and 5 show, the early years of the boom saw a spike in overall upstream employment, broadly in parallel with productivity gains for oilfield services labor (NAICS 213, which includes fracking services). It was only during the mid-2010s energy glut that the difference fracking made to the oil and gas labor composition truly came to a head. While US rig count dropped to beneath pre-boom levels,[78] field production of crude oil only dipped from a peak of 9,648 million barrels per day (mbd) in April 2015 to 8,545 mbd in September 2016 — still much higher than before the boom.[79] Natural gas saw even less of a decline, from 2,300 bcf/m in summer 2015 to a bottom of around 2,000 bcf/m in February 2017.[80] As the industry eventually recovered, its employment rate did not: core oil and gas jobs (NAICS 211) plateaued around 140,000 — about as many as had existed in the mid-2000s — despite increasing productivity, and oilfield services jobs (NAICS 213) have been on a downward, albeit oscillating, trend ever since.

[.fig][.fig-title]Figure 4: Labor Productivity Has Stagnated in Support Activities Despite Productivity Gains Since the Start of the Boom[.fig-title][.fig-subtitle]Oil and gas labor productivity (%), 2008-2024 (2017 base period)[.fig-subtitle][.fig]

[.notes]Source: Bureau of Labor Statistics. Note: NAICS 213 includes employment in the traditional mining sector as well as the extraction of oil and gas. This is the best proxy for oilfield services work made available through the BLS.[.notes]

[.fig][.fig-title]Figure 5: The Rise, Fall and Precarity of Supporting Sector Employment[.fig-title][.fig-subtitle]Annual average number of workers (thousands) in Support Activities for Mining (NAICS 213) and Oil and Gas Extraction (NAICS 211), 1990-2025[.fig-subtitle][.fig]

[.notes]Source: Bureau of Labor Statistics. Note: NAICS 213 includes employment in the traditional mining sector as well as the extraction of oil and gas. This is the best proxy for oilfield services work made available through the BLS.[.notes]

Alongside other technological efficiency improvements like horizontal drilling and pad drilling, the productivity gains associated with hydraulic fracturing have led in the long run to drastically reduced job growth, and in particular relative to physical output. In turn, the labor share of the oil and gas industry’s GDP has fallen substantially. As the Ohio River Valley Institute reports for the Appalachian Region (Ohio, West Virginia, and Pennsylvania), oil and gas GDP grew by $18.5 billion from 2010 to 2017, while labor income only grew by $1 billion. But this worsening discrepancy between increased oil and gas activity and its shrinking material benefits for the oil and gas workforce most vividly came to a head during the onset of the COVID-19 pandemic. At the end of 2020, “shut-ins” wiped out 22 percent of the industry’s jobs, whereas US oil and gas production recovered by 2023[81] — with fossil capital, of course, quietly recouping the difference in costs from reduced labor outlays.[82]

While many of the remaining jobs are relatively high-paying, boom and bust cycles have become more frantic, such that the workforce has not only become leaner but more precarious. This trend can be seen, for instance, in the labor composition of regions that experience the most intense fracking activity, which typically include very high percentages of transient labor, both in the upstream and midstream (pipelines) sectors.

[.box][.box-header]Transient oil and gas labor within the fracking booms (and busts)[.box-header][.box-paragraph]The most extreme example of transient oil and gas labor is in North Dakota. During the boom in the early 2010s, tens of thousands of people flocked to sparsely populated northwestern North Dakota seeking employment in the oil-rich fields of the Bakken Formation.[83] As the boom turned into a bust by the mid-2010s, the region saw absolute population decline as laborers were forced to find work elsewhere. But in regions with higher pre-existing population density, such as Appalachia, the fracking boom has led to an influx of temporary and out-of-state labor to work the gas fields. A 2015 WorkForce West Virginia analysis estimated that 40 percent of the state’s pipeline workers were not residents of West Virginia,[84] for instance, and Ohio’s Department of Job and Family Services noted in 2021 that over half of the state’s shale gas employment was occupied by non-residents.[85][.box-paragraph][.box]

Future decarbonization policy initiatives should heed two important aspects of the increasing transience of the oil and gas workforce. First, it constitutes an insecure tax base, with little tying people to the region beyond their precarious employment. Out West, for instance, thousands of rig workers live housed in dormitory-style “man camps,” which isolates them from local communities and only further amplifies the temporary, fleeting nature of their work.[86] Alongside the massive tax preferences fracking already receives,[87] the lack of a secure tax base can make it difficult for state and municipal governments to diversify regional economies away from such dangerously heavy dependence on the booms and busts of oil and gas development. While West Texas’ oil and gas industry has proven somewhat more durable, particularly given the sizable anchor cities of Odessa and Midland, North Dakota’s Bakken region has proven much more volatile, with municipalities at one point needing to taken on millions of dollars in debt in order to accommodate rising demand for services that may once again vanish with another bust (as had already occurred in the mid-2010s).[88]

Secondly, the influx of transient labor into the onshore industry has coincided with the proliferation of more insecure forms of employment, particularly contracting.[89] Contractors are much more vulnerable to the boom-and-bust cycle of oil and gas drilling. During the 2020 oil price crash, for instance, operator employment saw an eight percent decline, while the contractor workforce saw a 33 percent decline.[90] Supporting contractors are also much more likely to incur workplace injuries compared to the core oil and gas workforce.[91] But the rising use of contractors has in fact made formal labor more precarious as well, as evinced in the rise of “misclassification” lawsuits, wherein oil and gas employers have (illegally) treated their full-time employees as contractors in order to deny them overtime pay and health benefits.[92]

In addition to its underwhelming impact in terms of direct employment, the influx of fracking activity has likewise accrued little economic benefit for those rural communities most directly impacted. The largest gas producing region in the country, the Appalachian Basin, is particularly demonstrative. As the Ohio River Valley Institute has reported, the major fracking counties in Appalachia saw an average GDP increase of 61.1 percent from 2008 to 2019, compared to 14.1 percent GDP growth across Ohio, Pennsylvania and West Virginia as a whole.[93] Yet, over this same time period, personal income across these counties only grew 14.3 percent (versus 21.9 percent nationally and 14.7 percent across Ohio, Pennsylvania, and West Virginia), and job growth only increased 1.6 percent (versus 9.9 percent nationally and 3.9 percent across the same states). Ohio’s major fracking counties fared particularly poorly: despite an average 88.7 percent increase in GDP, they saw an average 8.4 percent decline in total jobs. Only two counties in “Frackalachia” beat national averages for both personal income and job growth: Washington County, PA — anchored by sizable, wealthy suburbs of Pittsburgh and a relatively diversified economy — and Doddridge, WV — a county of less than 10,000 residents. By contrast, fracking in Belmont County, OH became one of the more appalling examples of fossil capital’s robbery of the region’s resources, seeing a seven percent decline in jobs despite a 110.5 percent increase in GDP.

[.fig][.fig-title]Figure 6: Fracking Has Mixed Economic Benefit to Fracking Counties[.fig-title][.fig-subtitle]Comparison of average growth in GDP, personal income and employment, 2008-2023 (%) between the US average, Appalachian states and fracking counties[.fig-subtitle][.fig]

[.notes]Source: Bureau of Economic Analysis, Bureau of Labor Statistics. Note: The “Fracking Counties” category adopts the methodology used by ORVI. See also: Sean O’Leary, “Appalachia’s natural gas counties: Contributing more to the U.S. economy and getting less in return”, Ohio River Valley Institute, 2021, p. 7.[.notes]

Figure 6 updates the percent changes of GDP growth versus local economic benefits to include the pandemic years following the end of ORVI’s study period (2008–2019). The disparities have only intensified: Appalachia’s original fracking counties saw an average 169 percent increase in real GDP from 2008 to 2024 (significantly skewed by huge ongoing fracking booms in several Ohio and West Virginia counties), while personal income saw only a 25 percent increase — slightly less than OH/PA/WV as a whole and substantially less than the national average (40 percent) over this same time period. Employment in the original fracking counties has also further declined since the COVID-19 pandemic by an average of 11 percent from 2008 to 2024. Hence, personal income gains are being spread across substantially fewer workers than they were before the boom. The total labor force in the fracking counties has likewise fallen steeply at 7.9 percent, from 482,061 available workers in 2008 down to only 428,916 in 2024.

A core element of the IRA and Biden’s climate agenda more generally was a de facto jobs plan targeting divested “energy communities,” in particular by encouraging the repurposing of brownfield and Superfund sites into solar and wind farms. It may seem that the above observations about the precarity of the energy workforce could have been addressed through the IRA, had it not been prematurely dissolved with Trump’s return to office. The IRA was, among other things, precisely the kind of “industrial policy” that Democrats envisioned could overcome the “economy vs. environment” narrative promoted by the fossil fuel industry and Republicans alike. It was supposed to appropriate huge sums of public funds in order to stimulate new demand for clean energy labor in the same communities that have borne the brunt of the deleterious consequences of historical energy extraction. Moreover, the IRA’s infamous binding of tax credit eligibility to stringent and pro-union labor requirements indeed attempted to address the worsening working conditions of the existing oil and gas workforce just reviewed.[94]

But this policy design fundamentally misapprehended the problem that fracking has revealed, a problem which does not just concern oil and gas, but the energy sector as a whole. First, the IRA situated the struggle to decarbonize on false ground, attempting to introduce a green industrial employment strategy into regions dominated by the extractive sector, which could thus compete with the fossil fuel industry’s ostensible economic benefits. The Biden administration thought it could thus win back rural red districts, namely, by presenting decarbonization and climate policy as a massive employment opportunity.[95] However, the fossil fuel industry has needed little more than its own internal drive toward increasing investments in fixed capital relative to labor outlays in order shed its own workforce. As the industry now eagerly inquires into how the adoption of AI, robotics, and automation might help it even further lower labor costs, it is imperative for an effective decarbonization campaign to clarify how fracking simply has not been an economic boon for rural America.[96]

The more fateful error in Biden’s pitch to “energy communities” is that these fracking-induced changes are but the canaries in the oilfield indicating a longer-term trend toward itinerancy and worsening working conditions across energy sector employment. Although solar and wind power are at present significantly more labor-intensive industries than fossil fuels, and indeed numbered amongst some of the fastest-growing occupations in 2024,[97] their working conditions can be just as precarious as their fossil fuel industry counterparts.[98] This is because the bulk of clean energy infrastructure employment is in solar and wind installation, a temporary form of work unlikely to bring stable employment or ancillary economic benefits to divested rural regions.[99] Moreover, even if onshoring wind and solar manufacturing successfully overcomes supply chain disruptions, geopolitical tensions with China, and Trump’s relentless attacks on renewable energy, it will be by far the most capital-intensive component of the clean energy value chain. As a result, the bulk of sectoral employment will remain in the most grueling, precarious, and itinerant jobs, which will inevitably wane over time. A more durable and place-based workforce will require robust public investment in other rural economic sectors alongside renewable energy development, in particular healthcare and education. The quality of energy worker livelihood must be better supported through a more holistic approach to rural economic revitalization.

One other dimension of fracking should be noted, which links oil and gas labor precarity to the financial restructuring of energy investing after 2008, with important implications for future decarbonization policy. As the geographer Gabe Eckhouse has argued, increased capital intensity in the onshore industry has dovetailed with a “short cycle revolution” in energy investing.[100] The technical and material properties of fracking offer a convenient solution to the swelling long-term risks of ongoing oil and gas investment, from political opposition and price volatility to the market encroachment of renewable energy. Because a fracked well can be brought to production much quicker than conventional drilling, and because the bulk of its lifetime output typically occurs within the first few years of its production, unconventional oil and gas producers have been able to secure greater volumes of credit among financiers who have otherwise grown reluctant to invest in long-term conventional oil and gas development projects. Ironically, the increasing uncertainty of fossil capital’s future has led to the perverse incentivization of more, rather than less, hydraulic fracturing — despite its higher average breakeven price — as its faster rate of turnover affords finance capital a way to hedge against the long-term risks of “stranded” oil and gas assets.[101]

Notably, most of these creditors were still unable to make a profit through the 2010s. This is in large part because OPEC maintained production levels in order to protect its market share from the American frackers, in turn pushing energy prices down further than expected through the 2010s. Not only did the West Texas Intermediate (WTI) benchmark price for crude oil dip well below fracking’s breakeven price — leading to the aforementioned bankruptcies and mergers and acquisitions by the end of the decade — but this weak pricing environment meant US refineries just kept buying OPEC’s cheap, sour crude. In other words, the US petrochemical industry was unable to fully capitalize on the light, sweet crude supplies otherwise now available to them domestically. Accordingly, fracking hardly made America more “energy independent”; rather, it further entrenched the fossil fuel industry’s dependency on demand from both refineries and petrochemical manufacturers abroad.

Two conclusions pertinent to future energy policy can be drawn from this so-called “short cycle revolution.” First, campaigns in civil society to pressure private financiers to divest from fossil fuel assets often have unforeseen consequences. The risk of “stranded assets” did not in the end reduce access to credit for upstream producers,[102] at least not overall, but simply shifted the risk assessment to favor projects with quicker rates of return. The uncontrollability of fossil capital is apparent: when left up to the market, fossil fuel investment decisions tend to find new paths of (potential) profitability that can veer quite drastically from the intentions of environmentally conscientious investors.

Secondly, and more broadly, the “short cycle revolution” is illustrative of the deleterious consequences of leaving rural economic development up to the whims of private capital. From the perspective of energy financiers, social welfare is at best a secondary concern, which will always be trumped by the need to make a return on their investment. The reevaluation of capital risk, after all, is what motivated a change in lending behaviors, regardless of the worsening labor conditions needed to sustain a quicker rate of turnover. Indeed, it is irrational to expect capital to behave otherwise and thus to depend upon the logic of profit-making to improve worker livelihoods, let alone decarbonize the economy in the name of socioecological wellbeing.

Fracking has dramatically reconfigured the frontiers of fossil capital in the US. The sheer abundance of hydrocarbons unleashed has, for one thing, pushed the onshore industry to secure more and more demand for domestic oil and gas through export markets. Simultaneously, increased investments in alternative hydrocarbon commodity chains like petrochemicals and blue hydrogen have become increasingly central to the industry’s derisking strategy, allowing it to continue to thrive despite rising political, economic and social opposition to fossil fuels. Additionally, rising rates of productivity have meant that employment opportunities in the onshore industry are dwindling, while the jobs that remain are growing increasingly informal, itinerant and precarious.

Three policy interventions follow from this analysis.

First, domestic decarbonization policy must become attuned to the global production networks forged by US oil and gas exporters — transforming those fossil fuel dependencies into green trade partnerships, rather than entrenching them through military intervention. Second, green industrial planning must counteract fossil capital’s relentless adaptation: rejoining the Clean Energy Transition Partnership, ending public financing for new oil and gas development, and rapidly building public alternatives for hard-to-abate sectors while also curtailing fossil fuel demand — including from data centers. Third, any federal jobs program must go beyond renewable sector employment to deliver the durable rural revitalization that fracking promised but failed to provide: coordinated public investment across energy, healthcare, and education that matches the scale of the damage private capital has wrought. Together, these interventions suggest a reorientation of climate policy design away from disorderly, market-coordinated decarbonization and toward an integrated system. Policy design must shift from disorderly, market-coordinated decarbonization to an integrated system of democratic planning anchored by public ownership and investment — one with a real plan for fossil fuel phaseout, durably accountable to socioecological needs both within and beyond the United States.

The stakes for US energy policy after fracking are clear: the fossil fuel industry is not being replaced by renewable energy but is adapting alongside it to a new political-economic terrain. An explicitly oppositional stance toward continued fossil fuel extraction is imperative for effective and expedient decarbonization. Punitive measures have been proposed by progressive climate legislation for decades now but have never stuck and have confined decarbonization policy to a narrow form of capital discipline.[103] Since the onset of the fracking boom the onshore oil and gas industry has proven remarkably inventive in finding ways to flourish across a variety of energy policy landscapes. While economic pressures, such as a carbon tax, certainly would pose new costs, there is simply no guarantee that, even if they are legislatively achieved, they can actually lead to divestment from fossil fuel infrastructure and development. The rapid growth in oil, LNG, and NGL exports, as well as rapidly increasing investments in diversified hydrocarbon commodity chains, underscore the unpredictability and uncontrollability of market-coordinated investment decisions.

Despite a long history of policy failures in opposing fossil capital, the industry’s ongoing expansion simply cannot be ignored. The onshore oil and gas industry has expanded despite recent climate policy changes. These policies sometimes have also fueled new opportunities for fossil capital to become more entrenched in both the domestic economy and global production networks. Whether it is President Obama’s characterization of natural gas as a “bridge fuel,”[104] President Biden’s promotion of LNG exports in the name of “securing” European energy supply,[105] or President Trump’s adoption of the mantra “drill, baby, drill,”[106] US energy governance has consistently acquiesced to fracking more oil and more gas for the sake of expanding its geopolitical and economic power.

The Biden administration’s failure made the limits of a market-coordinated energy transition for restraining fossil capital abundantly clear and, in turn, revealed the necessity of pursuing alternative forms of coordination. Even the most “fine-grained”[107] green investment targeting has left wide open numerous pathways for the flourishing of the onshore oil and gas industry. There is no other option than to deliberately, concertedly, and expediently schedule the phaseout of fossil fuel production and consumption.

Achieving this, of course, is easier said than done, and any such transition in energy governance will be brought about not just by new policies but also through popular, mass mobilization against fossil capital. To this end, it is imperative to develop an integrated approach to rural revitalization that combines robust public investments across green energy, healthcare, and education to fundamentally improve socioecological wellbeing in rural regions. Reducing financial stimulus of divested energy communities to “good green jobs” is insufficient as a basis either for durable local economic development or, moreover, the holistic improvement of quality of life in these communities. It must also be underlined that the oil and gas workforce itself has perhaps the most to lose in ongoing fossil fuel development — not only because increasing capital intensity means fewer jobs and worsening working conditions, but also because chronic exposure to the toxic materials released during oil and gas extraction are quite literally killing them.[108] Mining and oil and gas extraction workers continue to maintain the highest rates of suicide of any employment sector in the country.[109]

Any future climate policy agenda must therefore recognize that decarbonization means nothing less than wholesale socioecological transformation. Market forces are ill-equipped to bring about this kind of transformation: the “hidden hand” of the market serves to discipline the behaviors of individual, profit-seeking participants through competition and price signals; it is not conducive to collective, self-conscious, society-wide decision-making. Even well-intentioned climate policies cannot control how the market reacts. Buoyed by the energy abundance fracking has made possible, the fossil fuel industry has only become more adept at navigating the world’s changing political-economic landscape, leveraging geopolitical instability and the rapacious energy needs of AI to further deepen carbon lock-in. If policymakers are serious about decarbonization, deliberate public coordination of fossil fuel phaseout is indispensable.

[1] Mike Ludwig, “Trump’s war with Iran is a boom for the US gas export industry,” Truthout, 03/04/2026. Available here.

[2] Justin Mikulka, “Global LNG industry growth will be casualty of war,” Powering the Planet, 22/03/2026. Available here.

[3] See the policy toolkit recently published by AI Now: North Star Data Center Policy Toolkit, AI Now Institute, 04/01/2026. Available here.

[4] “Biden-Harris Administration announces nearly $430 million to accelerate domestic clean energy manufacturing in former coal communities,” US Department of Energy, 10/22/2024. Available here.

[5] Lauren Kaori Gurley. “Shifting America to solar power is a grueling, low-paid job,” Vice, 06/27/2022. Available here.

[6] Mathew Larence, “Planet vs property: On dismantling fossil capital,” Common Wealth, 01/16/2025. Available here.

[7] Molly Taft, “New gas-powered data centers could emit more greenhouse gases than entire nations,” Wired, 04/22/2026. Available here.

[8] Kiley Bense, “From fracked gas in Pennsylvania to waste in Texas, tracking vinyl chloride production in the US,” Inside Climate News, 12/05/2023. Available here.

[9] Art Berman, “OPEC set to play the waiting game in oil market,” Time, 06/08/2015. Available here.

[10] James Burgess, “Global oil and gas job losses: 350,000 and counting,” UPI, 05/12/2016. Available here.

[11] Bradley Olson and Lynn Cook. “Wall Street Tells frackers to stop counting barrels, start making profits,” The Wall Street Journal, 12/13/2017. Available here.

[12] As a result of industrial electrification and data center growth since 2020, however, this prolonged sluggishness may be transforming into more sustained growth in overall energy demand.

[13] “U.S. energy facts explained.” US Energy Information Administration, 15/07/2024. Available here.

[14] “The United States expands its role as world’s leading ethane exporter,” US Energy Information Administration, 02/05/2019. Available here.

[15] Ari Shapiro with Jason Bordoff, “Year-end budget deal lifts ban on American oil exports,” NPR, 12/17/2015. Available here.

[16] Kiah Collier, “As oil and gas exports surge, West Texas becomes the world’s ‘extraction colony’,” The Texas Tribune, 10/11/2018. Available here.

[17] “Petroleum & other liquids,” US Energy Information Administration. Available here.

[18] “Trump and EU’s Juncker pull back from all-out trade war,” BBC, 07/26/2018. Available here.

[19] Joseph Biden and Ursula von der Leyen, Joint Statement, European Union Archives. . Available here.

[20] President Donald Trump, “Unleashing American Energy,” The Trump White House, 01/20/2025. Available here.

[11] “Natural gas,” US Energy Information Administration. Available here.

[22] “Petroleum & other liquids,” US Energy Information Administration. Available here.

[23] Beth Gardner, “How the fossil-fuel industry’s pivot to plastic is polluting our planet,” Scientific American, 11/18/2025. Available here.

[24] “U.S. NGL exports hit record high despite China trade disruption,” Pipeline & Gas Journal, 05/08/2025. Available here.

[25] Karen C. Seto, Steven J. Davis, Ronald B. Mitchell, Eleanor C. Stokes, Gregory Unruh, and Diána Ürge-Vorsatz, “Carbon lock-in: Types, causes, and policy implications,” The Annual Review of Environment and Resources, 2016, vol. 41, pp. 425–52.

[26] “Taking Stock 2023: US emissions projections after the Inflation Reduction Act,” Rhodium Group, 2023. Available here.

[27] David Fickling, “The LNG shock isn’t driving Asia back to coal,” Bloomberg, 04/01/2026. Available here.

[28] President Barack Obama, “State of the Union Address,” The Obama White House Archives, 01/28/2014. Available here.

[29] Robert H. Howarth, “A bridge to nowhere: Methane emissions and the greenhouse gas footprint of natural gas,” Energy Science & Engineering, May 2014, vol. 2, no. 2, pp. 47–60.

[30] President Barack Obama, “State of the Union Address,” The Obama White House Archives. Available here.

[31] Emissions of Carbon Dioxide in the Electric Power Sector, Congressional Budget Office, December 2022. Available here.

[32] Naveena Sadasivam and Jake Bittle, “Data centers are scrambling to power the AI boom with natural gas,” Grist, 02/10/2026. Available here.

[33] “FACT SHEET: Overview of the Clean Power Plan,” US Environmental Protection Agency, 2015. Available here.

[34] Alison Cassady, “The Clean Power Plan: A critical step toward decarbonizing America’s energy system,” Center for American Progress, 04/15/2015. Available here.

[35] Adam Vaughan, “Obama’s Clean Power Plan hailed as US’s strongest ever climate action,” The Guardian, 3/08/2015. Available here.

[36] David Roberts, “The 6 things you most need to know about Trump’s new climate plan,” Vox, 08/19/2019. Available here.

[37] Umair Irfan, “Trump’s EPA just replaced Obama’s signature climate policy with a much weaker rule,” Vox, 08/19/2019. Available here.

[38] Monika Dokl, Anja Copot, Damjan Kranjc, Yee Van Fan, Annamaria Vujanović, Kathleen B. Aviso, Raymond R. Tan, Zdravko Kravanja, and Lidija Čuček, “Global projections of plastic use, end-of-life fate and potential changes in consumption, reduction, recycling and replacement with bioplastics to 2050,” Sustainable Production and Consumption, November 2024, vol. 51, pp. 498–518.

[39] In the European context, John Szabo has already written perceptively on this topic. See John Szabo, “Fossil capitalism’s lock-ins: The natural gas-hydrogen nexus,” Capitalism Nature Socialism, 2021, vol. 32, no. 4, pp. 91–110.

[40] Courtney Bernhardt, “Plastics industry boom brings flood of new ethylene ‘cracker’ plants, despite frequent environmental violations,” Oil & Gas Watch, 20/09/2022. Available here.

[41] “Fueling plastics: How fracked gas, cheap oil, and unburnable coal are driving the plastics boom,” Center for International Environmental Law, 2017. Available here.

[42] Michael Ratner, “Natural gas liquids: The unknown hydrocarbons,” US Congress. Available here. 10/26/2018. Available here.

[43] Kiley Bense, “Pennsylvania lured Shell to the state with a $1.65 Billion tax break. Now the company wants to sell its plant,” Inside Climate News, 08/22/2025. Available here.

[44] Eric de Place and Julia Stone, “Appalachia is fueling a global petrochemical buildout,” Ohio River Valley Institute, 08/29/2022. Available here.

[45] “China the world’s biggest plastic producer,” Barron’s, 08/07/2025. Available here.

[46] Stephanie Findaly and Haohsiang Ko, “Chinese demand spurts US ethane exports to record high,” Financial Times, 05/15/2026. Available here.

[47] Mengpin Ge, Johannes Friedrich, and Leandro Vigna, “Where do emissions come from? 4 charts explain greenhouse gas emissions by sector,” World Resources Institute, 12/05/2024. Available here.

[48] “Assessing the greenhouse gas emissions of the US petrochemical industry,” Rhodium Group, 02/12/2025. Available here.

[49] Adam Hanieh, “Petrochemical Empire,” New Left Review, August 2021, vol. 130, pp. 25–51, p. 51.

[50] “The hard stuff: Navigating the physical realities of the energy transition,” McKinsey Global Institute, 2024. Available here.

[51] “Department of Energy Hydrogen Program Plan,” US Department of Energy, 2024. Available here.

[52] There are four tiers of eligibility, extending from $0.60/kg for 2.5–4.0 kilograms of lifecycle CO2e emissions for every kilogram of “clean” hydrogen produced, to the full $3/kg if the hydrogen is produced with less than 0.45 kg/CO2e. Note that anti-stacking rules generally prevent hydrogen production facilities from claiming both 45V hydrogen production credits and 45Q carbon capture credits for the same process streams. See Zane Gustafson, “A climate advocate’s guide to calculating 45V and 45Q tax credits,” Ohio River Valley Institute, 01/22/2026. Available here.

[53] Angela C. Jones and Donald J. Marples, “The Section 45Q Tax Credit for Carbon Sequestration,” US Congress, 01/25/2023. Available here.

[54] “U.S. National Hydrogen Strategy and Roadmap,” US Department of Energy, 2023. Available here.

[55] J.O. Bockris, The Solar-Hydrogen Alternative, The Architectural Press, 1976.

[56] Jeff St. John, “Clean energy experts break down hydrogen hype and hope,” Canary Media, 02/01/2024. Available here.

[57] Tom DiChristopher, “NiSource advances early-stage hydrogen investments at gas, electric utilities,” S&P Global, 09/10/2023. Available here.

[58] “Hydrogen blending – Not a serious decarbonization pathway,” Clean Air Task Force, 2024. Available here.

[59] “US weighs funding cuts to four of seven hydrogen hubs,” Reuters, 03/26/2025. Available here.

[60] Alexander C. Kaufman, “Trump’s cuts to billion-dollar hydrogen hubs rattle industry,” Canary Media, 10/10/2025. Available here.

[61] “US Department of Energy to cancel all hydrogen hub grants, leaked documents reveal,” Fuel Cell Works, 10/08/2025. Available here.

[62] Alan Mitchell, Sam Bowers, Eliza Sheff, Sam Bailey, and Jess Wymer, “Continued uncertainty: Department of Energy circulates latest ‘retain/modify’ awards lie,” Clean Air Task Force, 05/11/2026. Available here.

[63] “U.S. Preserves and Increases 45Q Credit in ‘One Big Beautiful Bill Act’,” Global CCS Institute, 07/08/2025. Available here.

[64] Vandana Gombar, “US data center builder goes off-grid to speed deployments,” BloombergNEF, 02/27/2026. Available here.

[65] Naveena Sadasivam and Jake Bittle, “Data centers are scrambling to power the AI boom with natural gas,” Grist, 02/10/2026. Available here.

[66] Molly Taft, “Data centers are driving a US gas boom,” Wired, 01/28/2026. Available here.

[67] Brian Martucci, “A fraction of proposed data centers will get built: Utilities are wising up,” Utility Dive, 05/15/2025. Available here.

[68] Aaron Larson, “Gas turbine supply chain bottlenecks could reshape the generation mix in 2030 and beyond,” Power Mag, 15/01/2026. Available here.

[69] Aaron Larson, “Engine power plants surge as data centers drive unprecedented demand,” Power Mag, 03/02/2026. Available here.

[70] Advaith Arun, Bubble or Nothing, Center for Public Enterprise, 11/12/2025. Available here.

[71] Nick Lichtenberg, “Communities are blocking billions in data centers. Big Tech has wagered $1 trillion otherwise,” Fortune, 05/18/2026. Available here.

[72] Nina Lakhani, “Biden administration warns natural gas expansion would drive up domestic costs,” The Guardian, 12/17/2024. Available here.

[73] Rachel Gass, “Unpacking the 2025 Annual Energy Outlook,” The Energy Co-Op, 04/30/2025. Available here.

[74] Kevin A. Hassett and Aparna Mathur, “Benefits of hydraulic fracturing,” American Enterprise Institute, 04/04/2013. Available here.

[75] Amanda Eversole, “Abundant U.S. natural gas, oil deliver America nearly $2 trillion in economic, trade and job Benefits,” American Petroleum Institute, 05/16/2023. Available here.

[76] “All employees, oil and gas extraction,” Federal Reserve Bank of St. Louis, 01/08/2025 (last updated). Available here.

[77] Ted Boettner, “The fracking boom in Appalachia: Big GDP growth, small amount of jobs and local income,” Ohio River Valley Institute, 2020. Available here.

[78] David Wethe, “Global oil job cuts top 250,000,” Bloomberg, 11/20/2015. Available here.

[79] “Petroleum & other liquids,” US Energy Information Administration, 08/29/2025 (last updated). Available here.

[80] “Natural gas,” US Energy Information Administration, 08/29/2025 (last updated). Available here.

[81] Mike Soraghan, “Oil and gas jobs decline amid record-breaking production,” E&E News, 08/08/2024. Available here.

[82] “More oil and gas production = fewer jobs,” Food & Water Watch, 2022. Available here.

[83] Jens Manual Krogstad, “How North Dakota’s ‘man rush’ compares with past population booms,” Pew Research Center, 0716//2014. Available here.

[84] “West Virginia oil and gas study,” WorkForce West Virginia, 2015. Available here.

[85] “2021 annual Ohio shale report,” Ohio Department of Job and Family Services, 2021. Available here.

[86] Rachel Adams-Heard, “Welcome to the ‘man camps’ of West Texas,” Bloomberg, 08/07/2018. Available here.