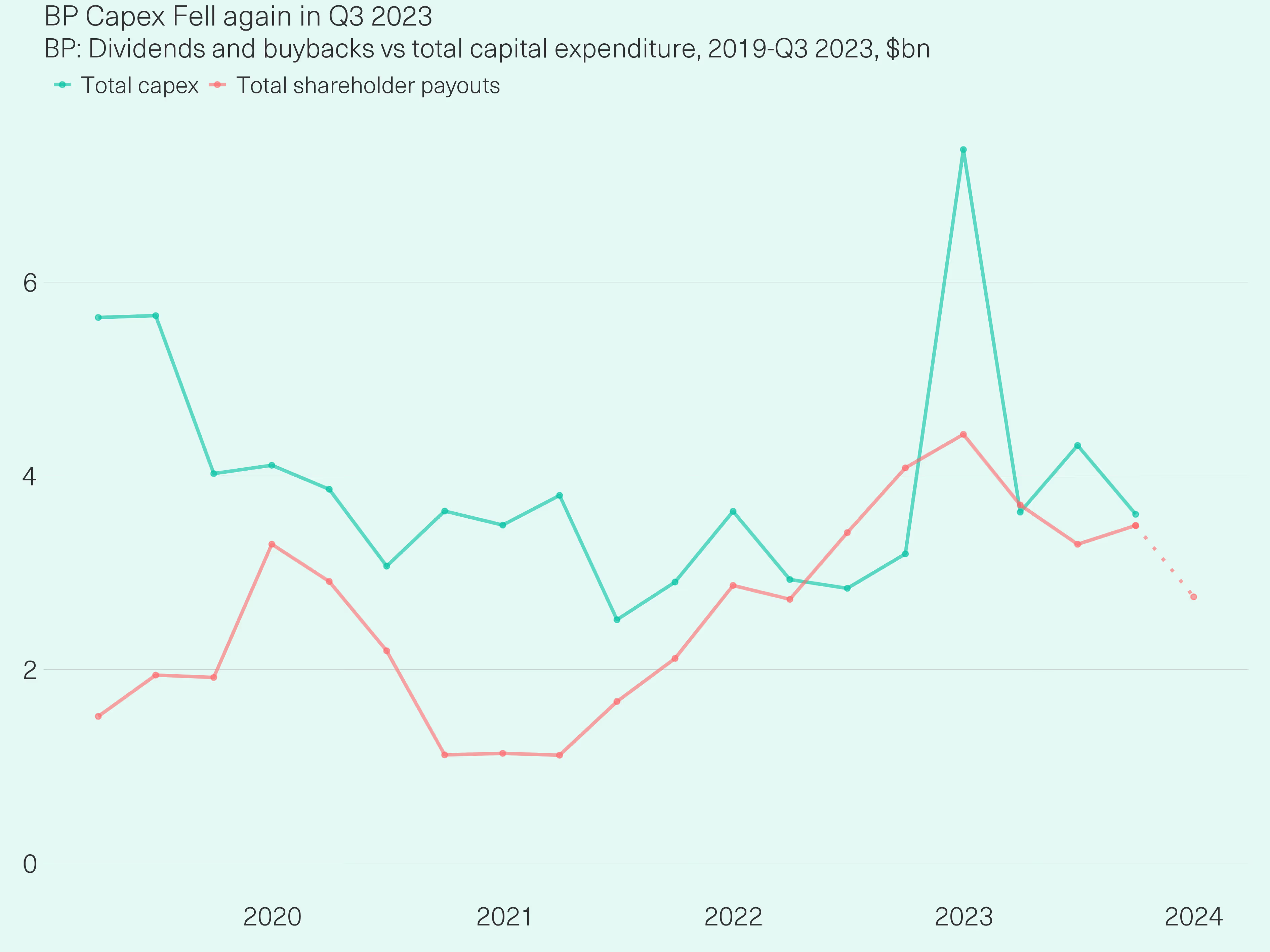

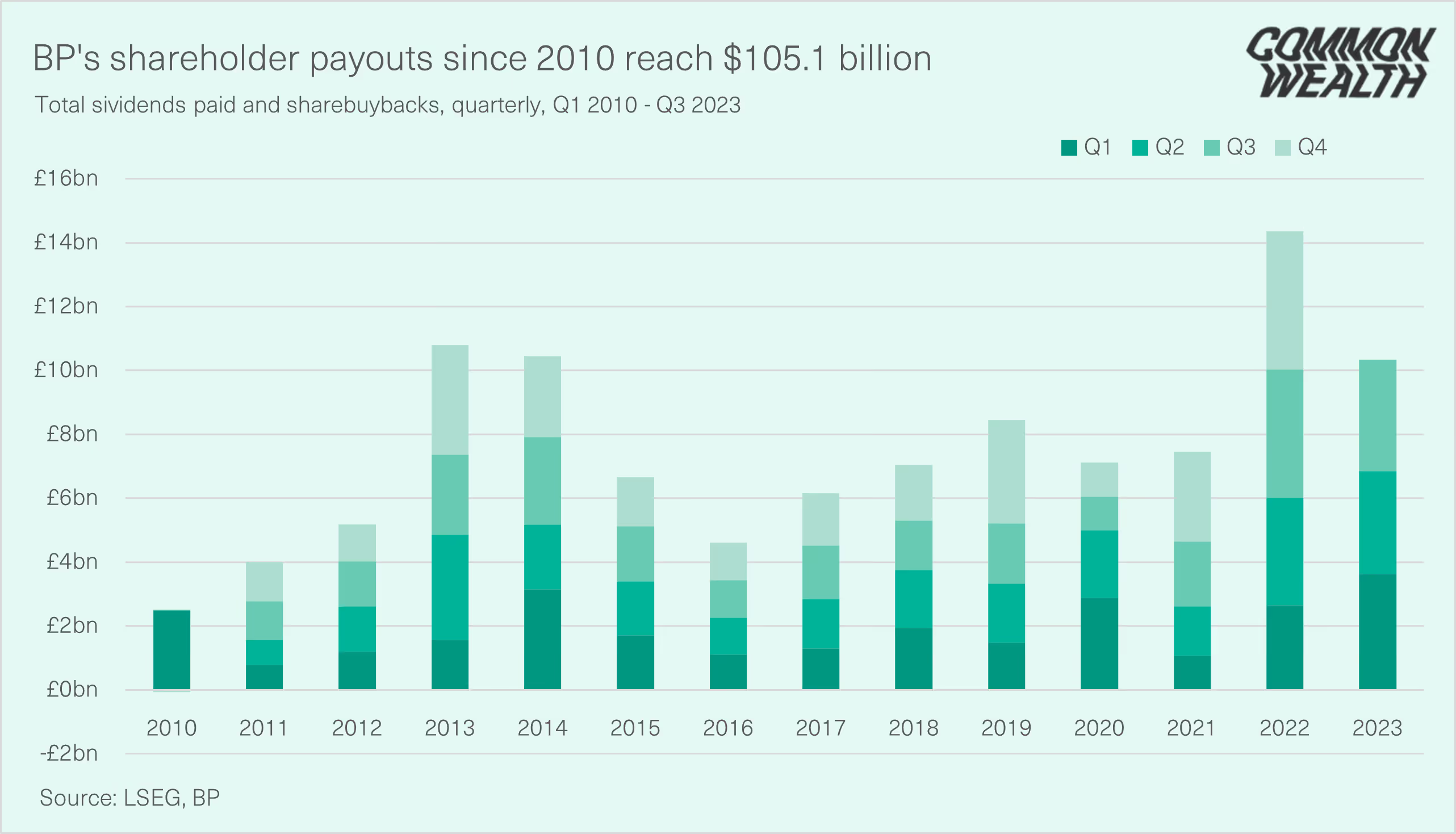

Analysis from the think tank Common Wealth finds BP reported profits of $3.3 bn (£2.7 bn) in its Q3 2023 results. Shareholder payouts totalled $3.3 bn (£2.7 bn), comprised of $2 bn (£1.6 bn) in share buybacks and $1.2 bn (£0.99 bn) in dividends.

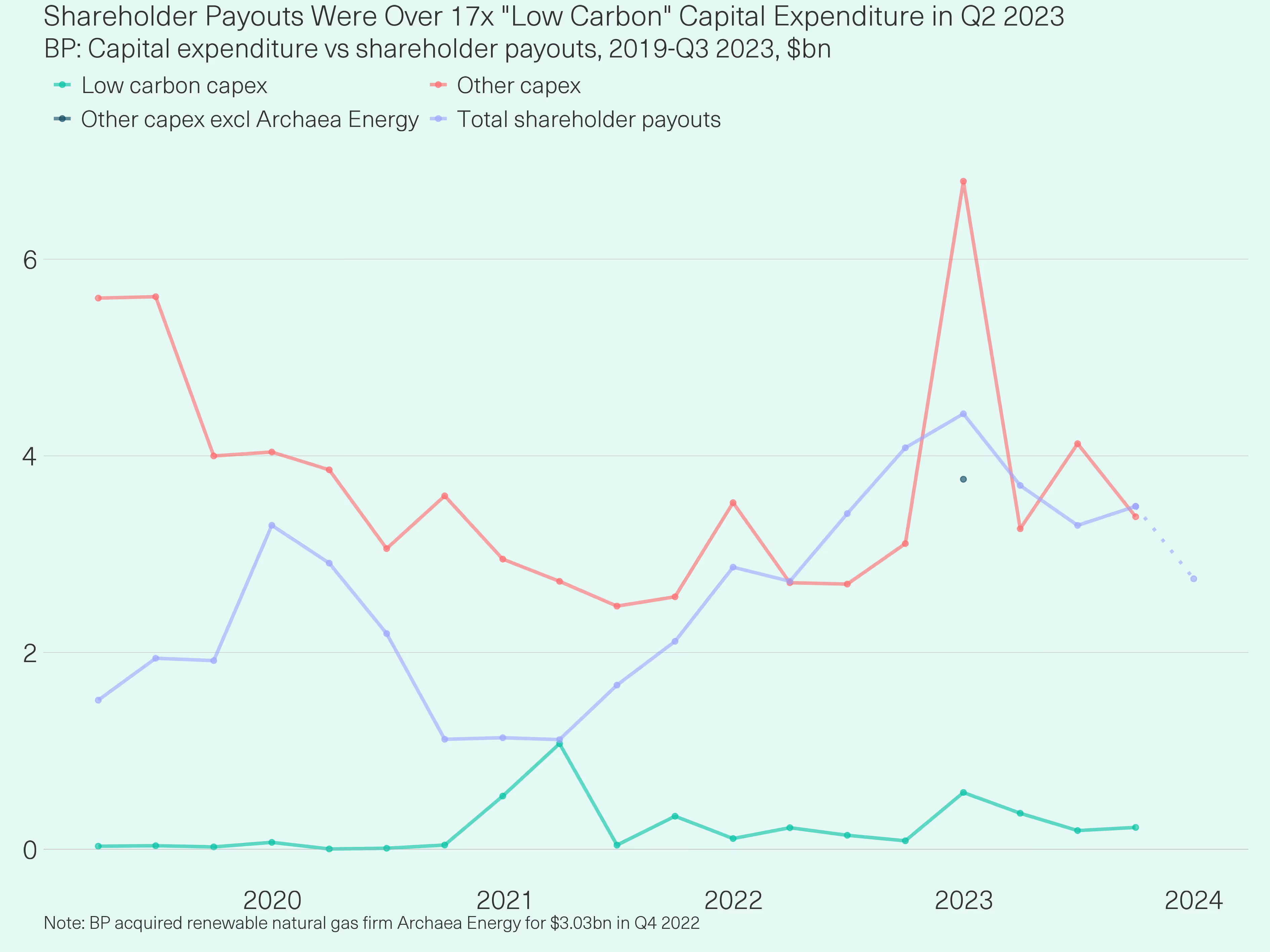

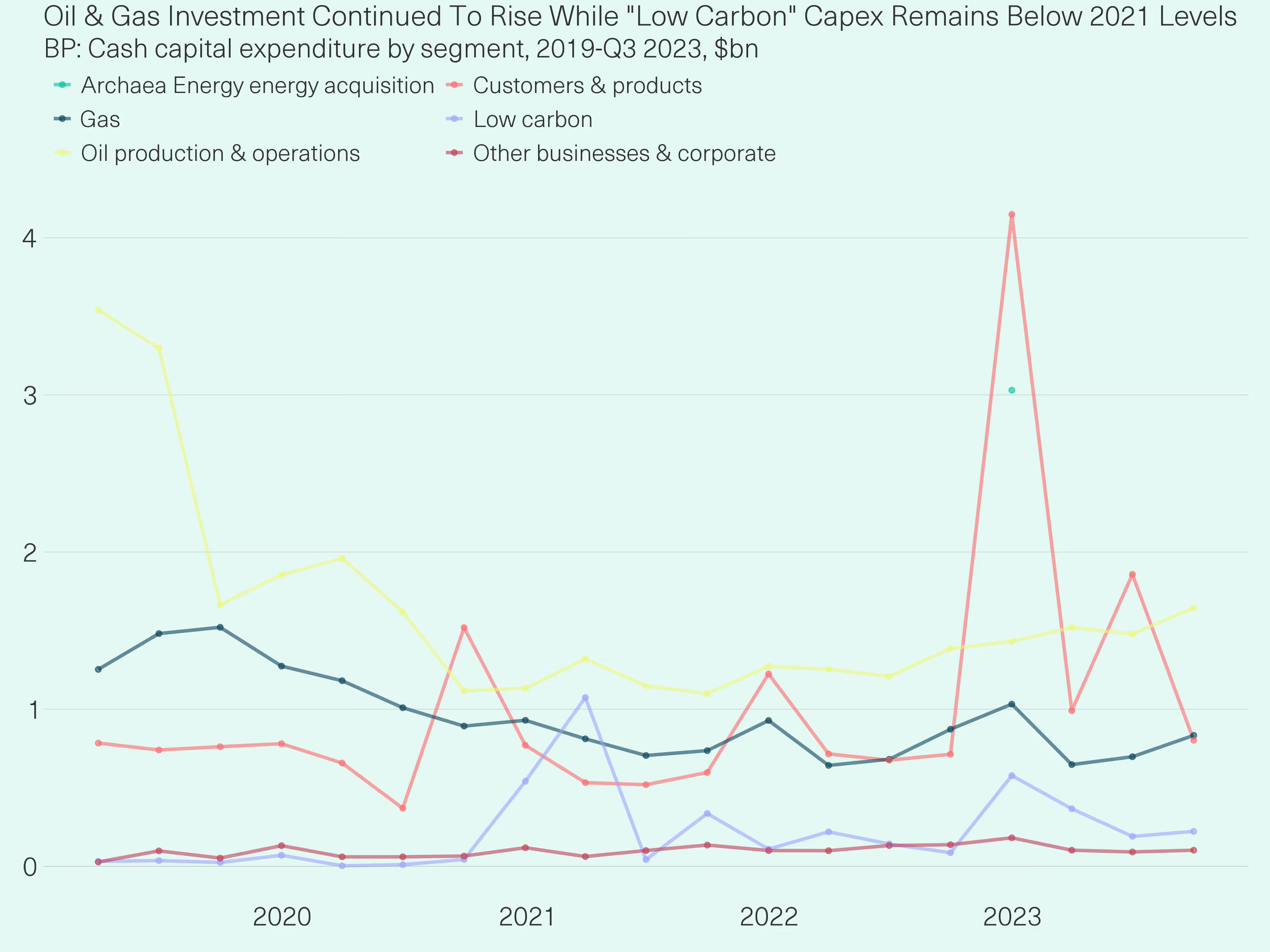

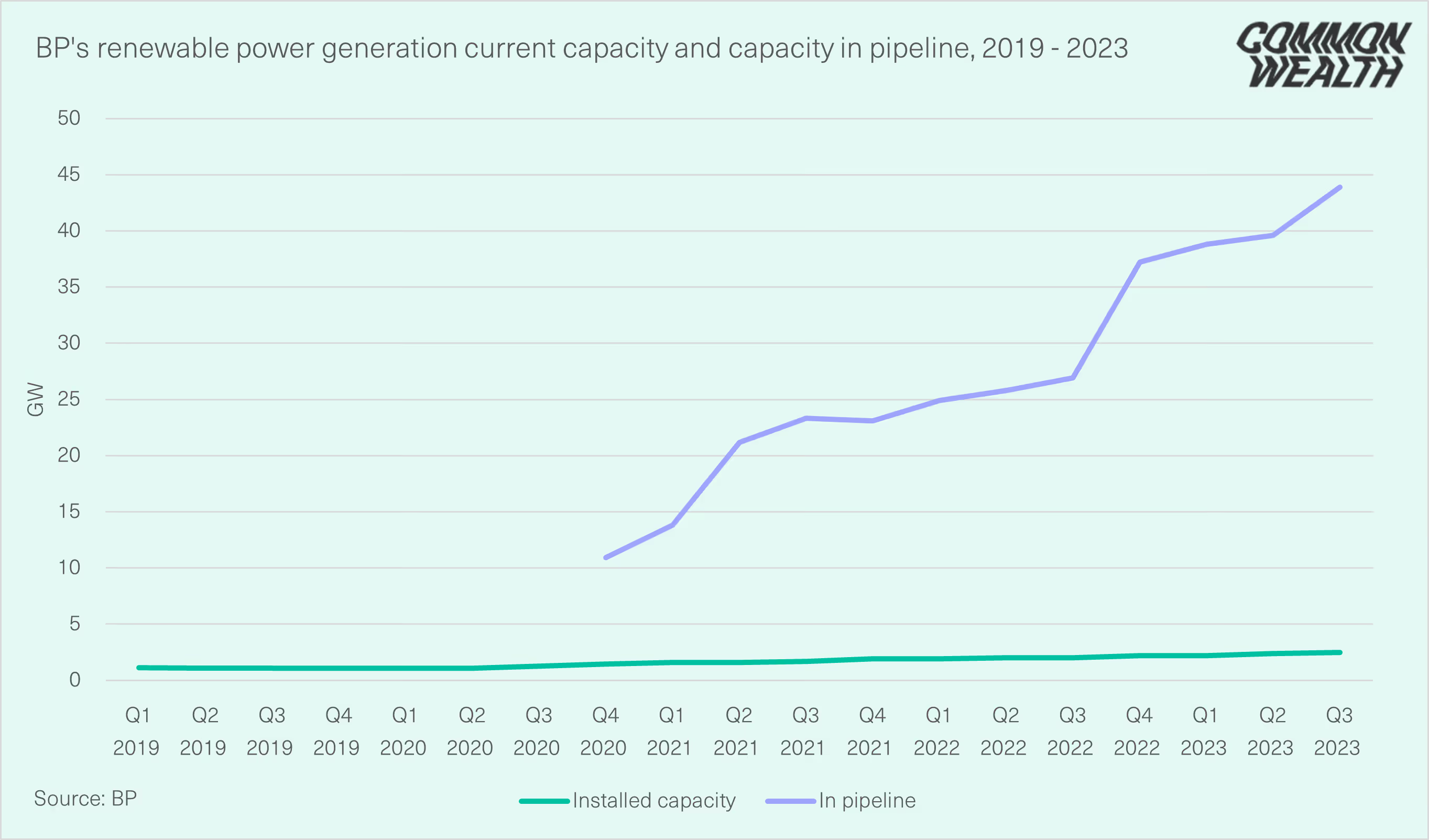

The analysis adds to the mounting evidence that despite its climate-friendly rhetoric, BP is doubling down on fossil fuels as the climate crisis intensifies. The new figures show BP's investment in “low carbon” segments pales relative to its investment in fossil fuels and what it pays out to its shareholders. In Q3, Common Wealth found BP invested 11 times as much in fossil fuels ($2.2 bn) as in its “low-carbon” segment ($190 m). BP’s “low carbon” segment includes a range of investments including renewables, hydrogen and carbon capture. In total, BP has paid shareholders $105.1bn since 2010.

Over the summer, the government re-announced plans to issue 100 new fossil fuel exploration licenses in the North Sea and approval was granted for the Rosebank oil field, the largest in the UK. However, according to the campaign group Uplift, an estimated 80% of North Sea oil is exported overseas, highlighting the limited domestic benefits of the government's policy.

Previous Common Wealth analysis has also highlighted the growth of private equity-backed firms and overseas state-owned entities in North Sea oil and gas, with countries like the UAE and China present in the North Sea, among others. Forthcoming research from Common Wealth will track the changing pattern of ownership of North Sea oil.

The surge in profits and shareholder payouts from fossil fuel giants amidst an energy-driven cost of living crisis raises critical questions about the structure and role of the for-profit corporation in driving a secure and fair transition to a clean energy future.

Chris Hayes, Senior Analyst at Common Wealth, said:

The last two years have locked us into two mutually reinforcing distributive and ecological crises, with oil majors hoovering up cash from the rest of the economy and using to consolidate their position and hasten climate breakdown.

All net zero pathways demand fossil fuel majors wind down their existing dirty assets and scale up renewables. Yet as we see, as long as the stewards of these assets remain answerable to shareholders, the pace of both will remain glacial. As Bernard Looney reiterated at the last earnings call, "our returns thresholds are sacrosanct". Little else is.

Using cash windfalls to buy up existing low- carbon companies should not be mistaken for additive investment in decarbonisation and should be recognised for what it is — consolidation of market power whose consequences are purely distributive.

Melanie Brusseler, Senior Researcher at Common Wealth, said:

Malcoordination of the energy transition can be told as a tale of two energy firms: in the largest deal in its history, last month Chevron acquired oil and gas producer Hess—a $53 billion bet that demand for fossil fuels will remain steady for decades. This comes mirrored across the industry as companies invest energy crisis super-profits in an acquisition frenzy. Chevron’s Chief Executive says that he sees no imminent peak in oil demand, painting himself as a realist among what he suggests are a growing band of environmental ideologues. The International Energy Agency, the west’s oil watchdog, is not “remotely right” that all fossil fuels, including oil and gas, will see a peak in demand before the end of this decade, according to Wirth.

Meanwhile, the German government is preparing a bailout of Siemens Energy, who has seen its shares fall by nearly 70% since June when it announced losses by its wind turbine arm Siemens Gamesa due to technical problems, input inflation, and boom bust order cycles downstream of disorganized private investment in clean generation.

For-profit energy firms are structurally unable to orchestrate the phaseout of fossil fuels and the rapid, large- scale rollout of a clean energy system. Instead, we need public energy companies freed from the profit imperative that can invest and divest to meet social goals.

Sophie Flinders, Data Analyst at Common Wealth, said:

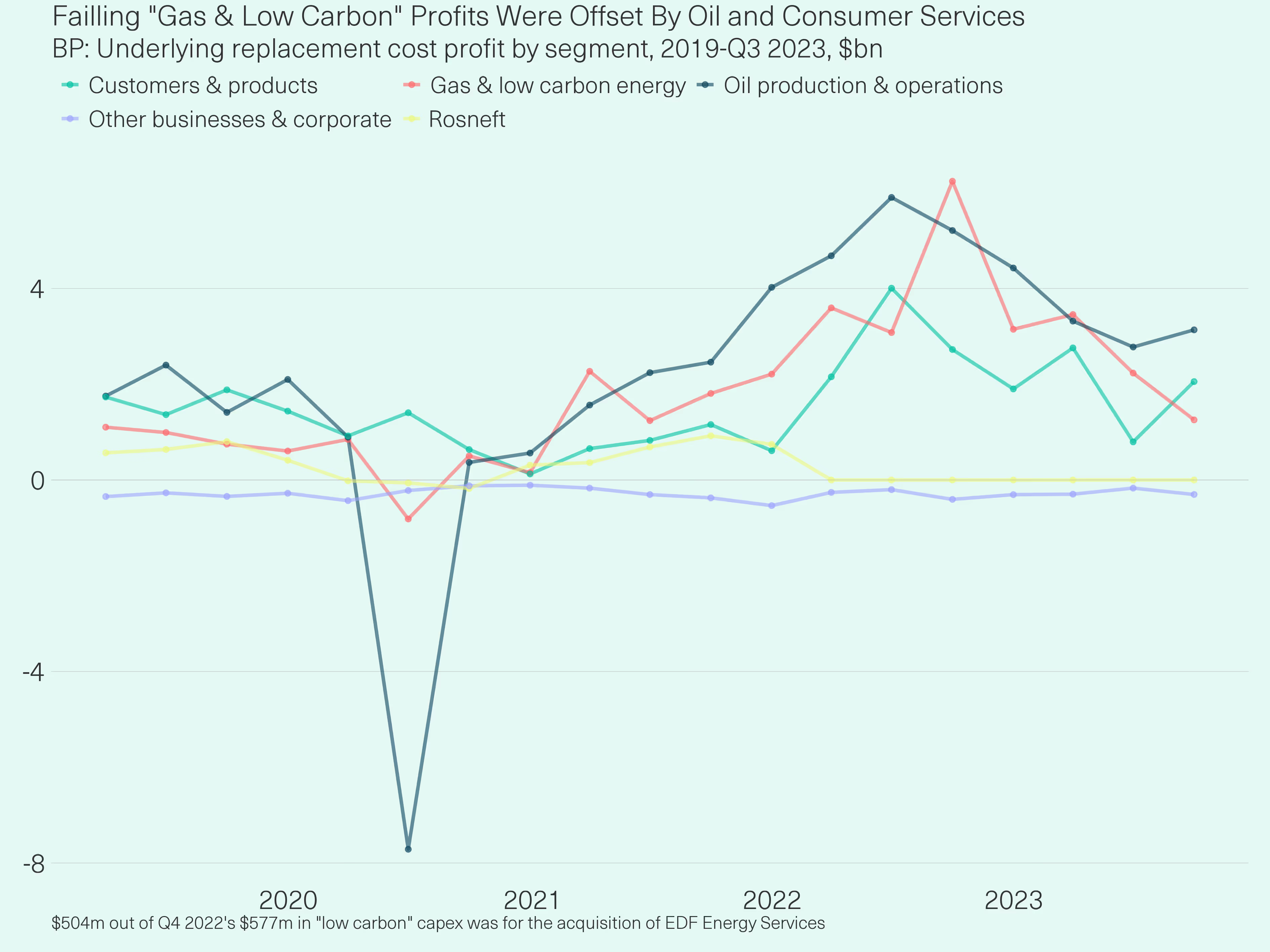

Today’s results tell us one thing: Big Oil is one of the biggest barriers to the clean energy transition. BP has failed to substantially increase their renewable capacity and instead diverted investment into new fossil fuel extraction and the expansion of their existing oil and gas operations. This makes sense to them. Their oil and gas segments are profitable and provide significant and reliable returns. But this does not make sense for protecting the planet from the worst of climate breakdown.