National Grid plc is a publicly listed company with a diverse portfolio of business interests split across the US and UK. In the UK (specifically England, Scotland and Wales, here after referred to as Britain), National Grid is the parent company of several subsidiaries that serve central functions in our energy system. These include companies that own and operate the long-range transmission infrastructure that carries gas and electricity throughout the country, as well as a system operator that ensures the balancing of supply and demand in real time. The cost of these services is paid for through “network charges” in household or business energy bills.

Driven in large part by Russia’s invasion of Ukraine and the conflict’s impact on global gas supply and by increased demand for energy following the end of the Covid-19 lockdowns in 2021, the ongoing crisis in Britain’s energy system has reopened a crucial debate on the system’s ownership and design, and whether these are fit for purpose. Common Wealth is undertaking a programme of work on every aspect of Britain’s energy system, from generation to supply, looking at how to establish an energy future that is secure, green, and affordable for all.

In this briefing, we present analysis of National Grid plc and its key UK subsidiaries, including the firm’s ownership, distributions to shareholders and measures of profitability.

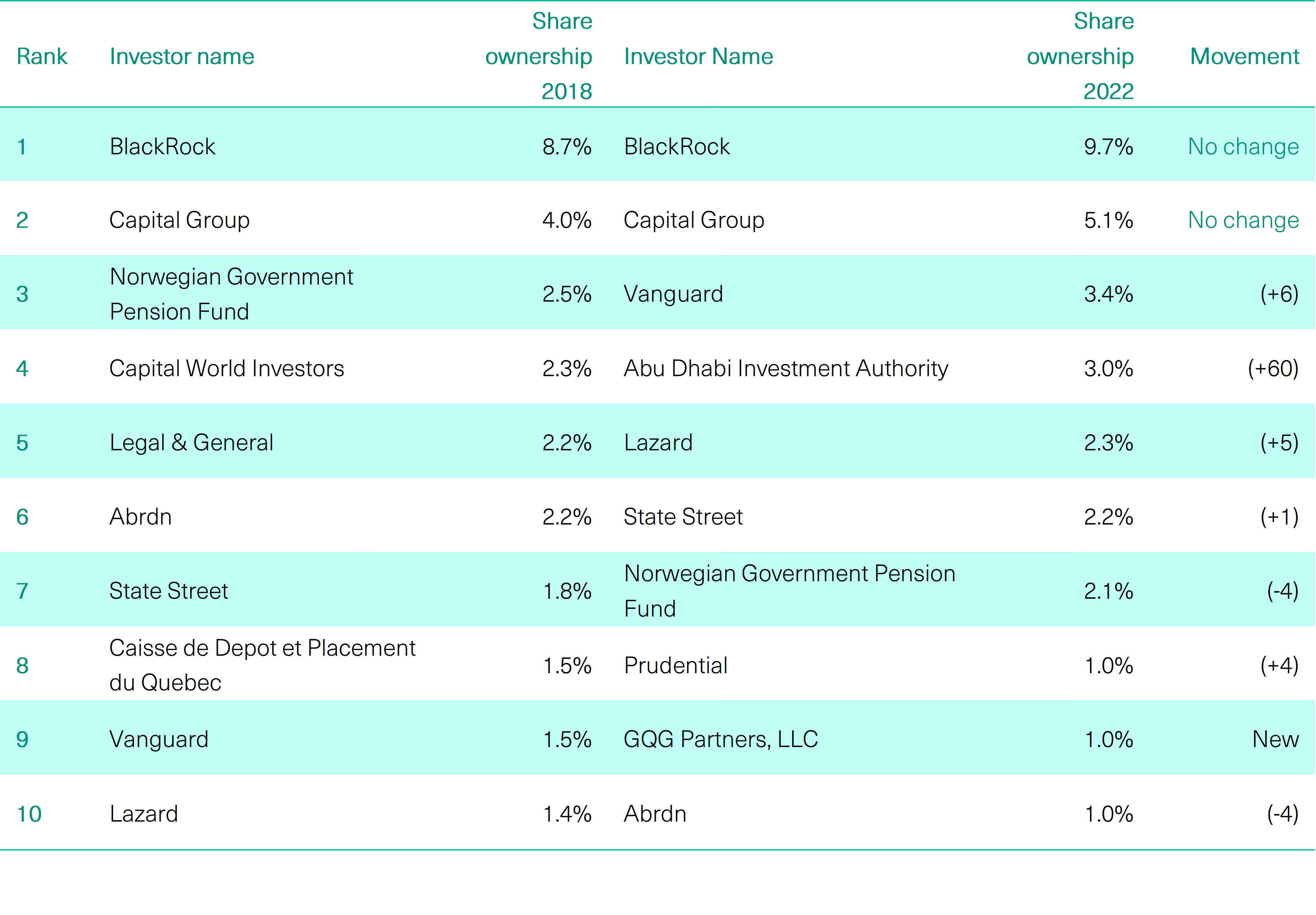

National Grid plc’s top ten shareholders range from global asset management firms BlackRock and Vanguard to public pension funds, notably those of Norway and the Abu Dhabi Investment Authority. As of 2022, BlackRock held close to 9% of total shares.

[#interactive][.img-caption][.img-caption-header]Table 1[.img-caption-header][.img-caption-text]Note: 2018 is the financial year 2017/18 etc.[.img-caption-text][.img-caption][#interactive]

Although National Grid plc is a multinational company with diverse business segments, our analysis focuses on the following key subsidiaries relevant to Britain’s energy system:

All three of these subsidiaries were, until very recently, wholly owned by National Grid plc. In March 2022, a deal was agreed for National Grid plc to sell 60% of its shares in National Grid Gas plc to a consortium including Australian investment giant Macquarie and the British Columbia Investment Management Corporation, whose AUM are approximately 80% derived from the Canadian province’s public pension funds.

Until the sale of National Grid Gas plc shares this year, these three key subsidiaries were all wholly owned by National Grid plc, thus dividend figures cited reflect internal redistributions of funds within the company. Payouts to external are made via National Grid plc.

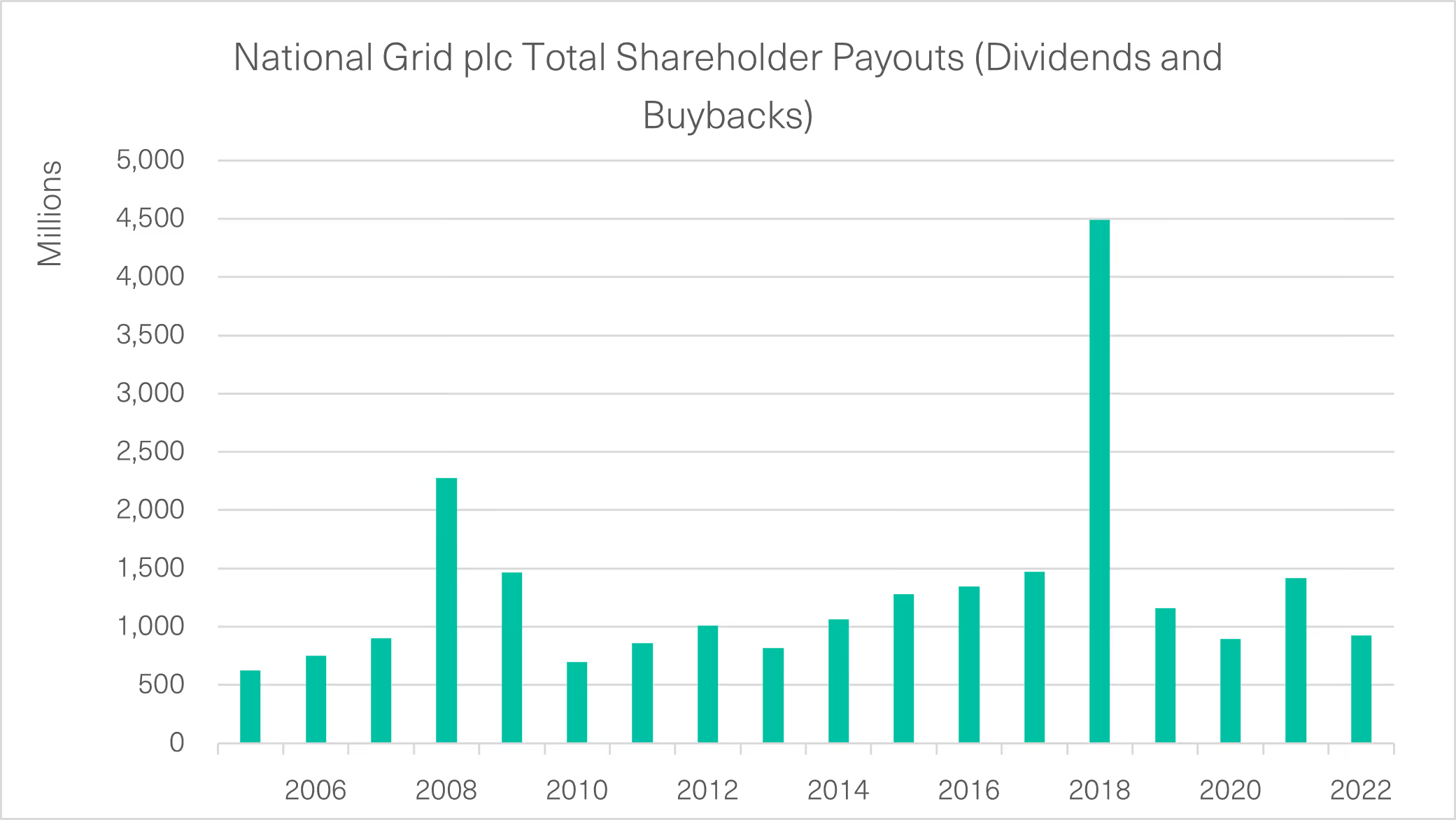

[.img-caption]Figure 1 National Grid plc Total Shareholder Payouts (NB 2018 is the financial year 2017/18 etc.)[.img-caption]

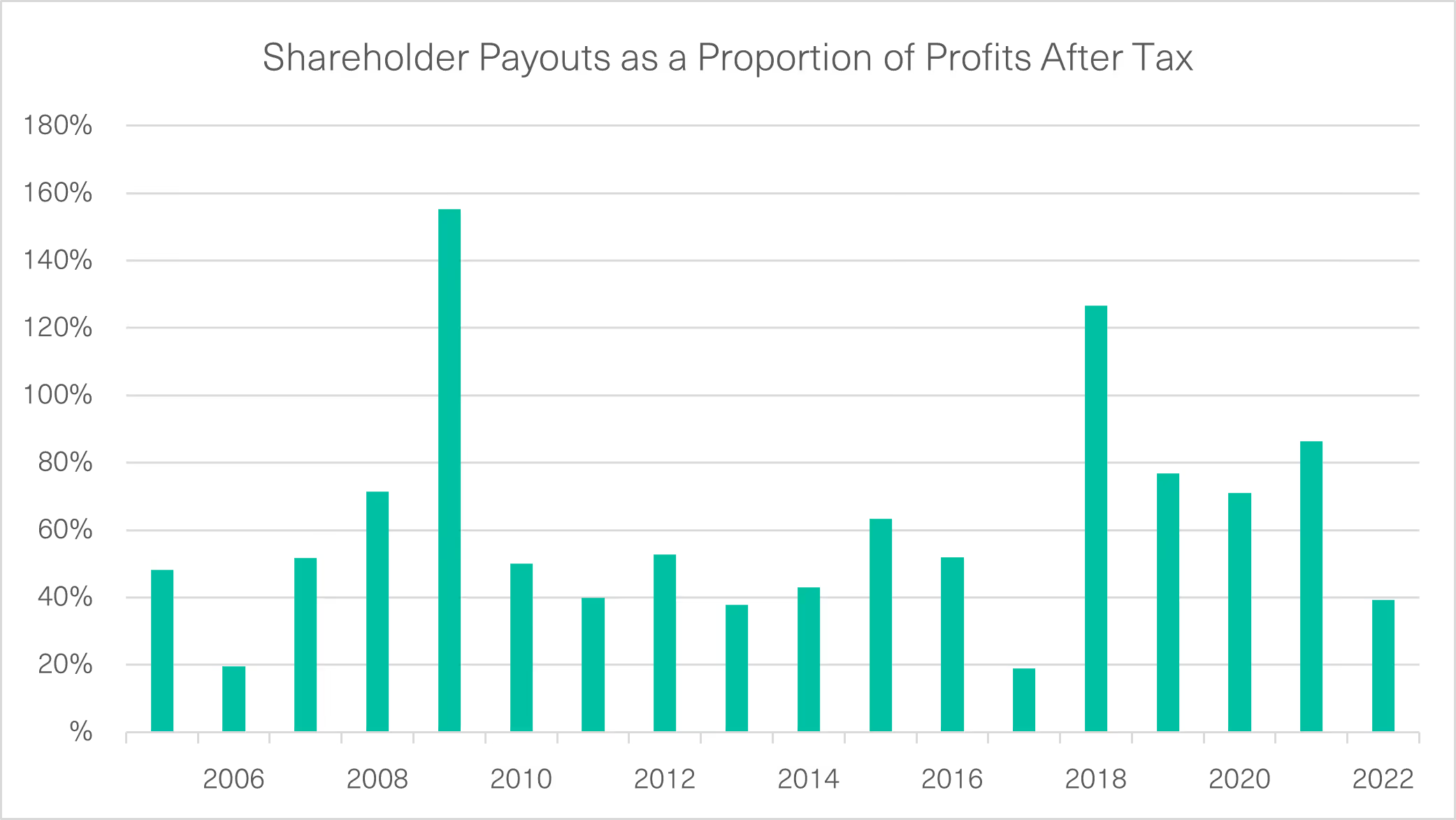

[.img-caption]Figure 2 Shareholder Payouts as a Proportion of Profits After Tax[.img-caption]

Over the five years 2018-22, the electricity segment of the business made interest payments on its debts totalling £676 million. These payments relate to multiple borrowing sources including intra-company borrowing, bank loans and overdrafts, and corporate bonds. A breakdown of the total value of debts in each of these categories was not available.

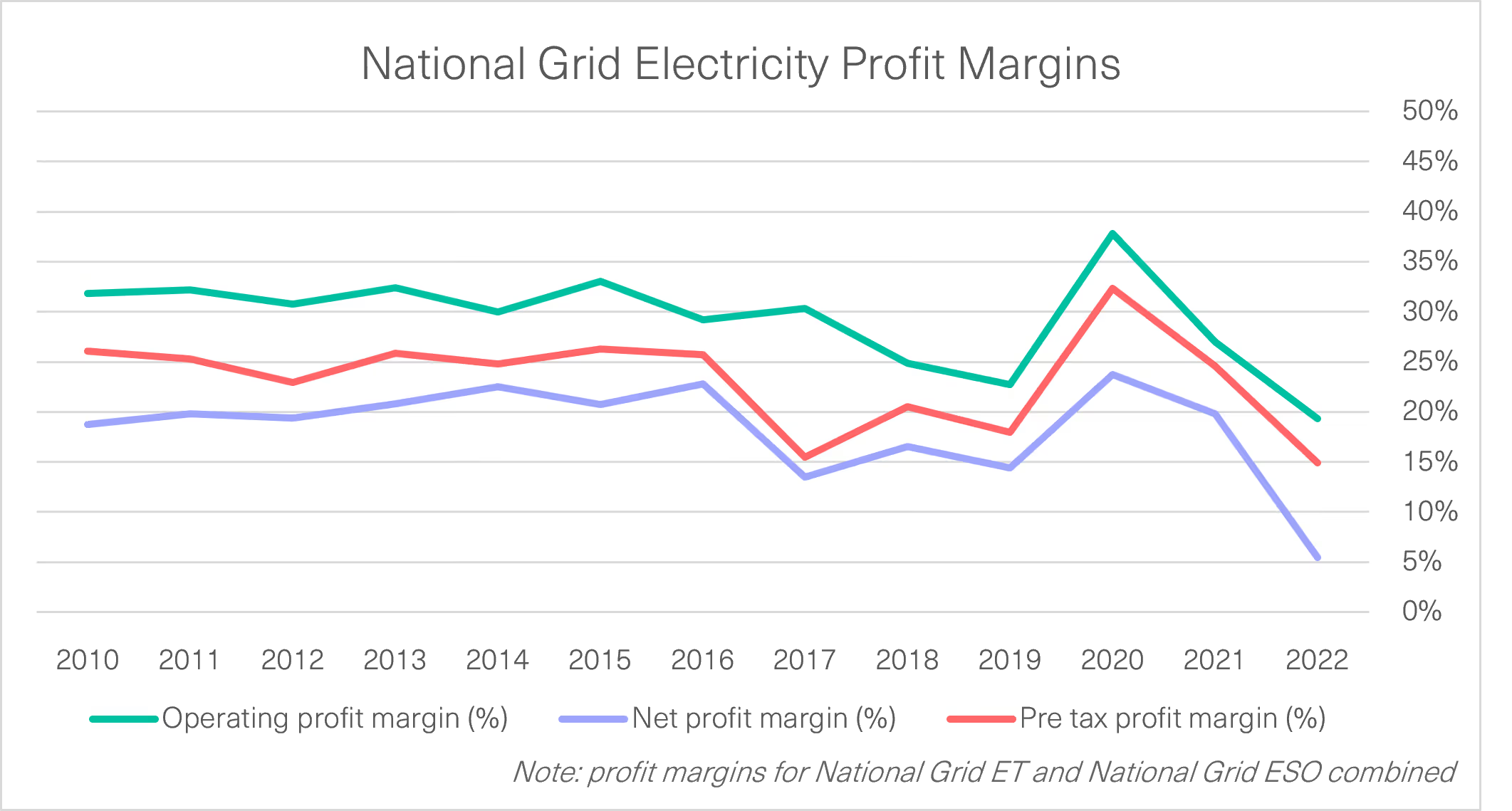

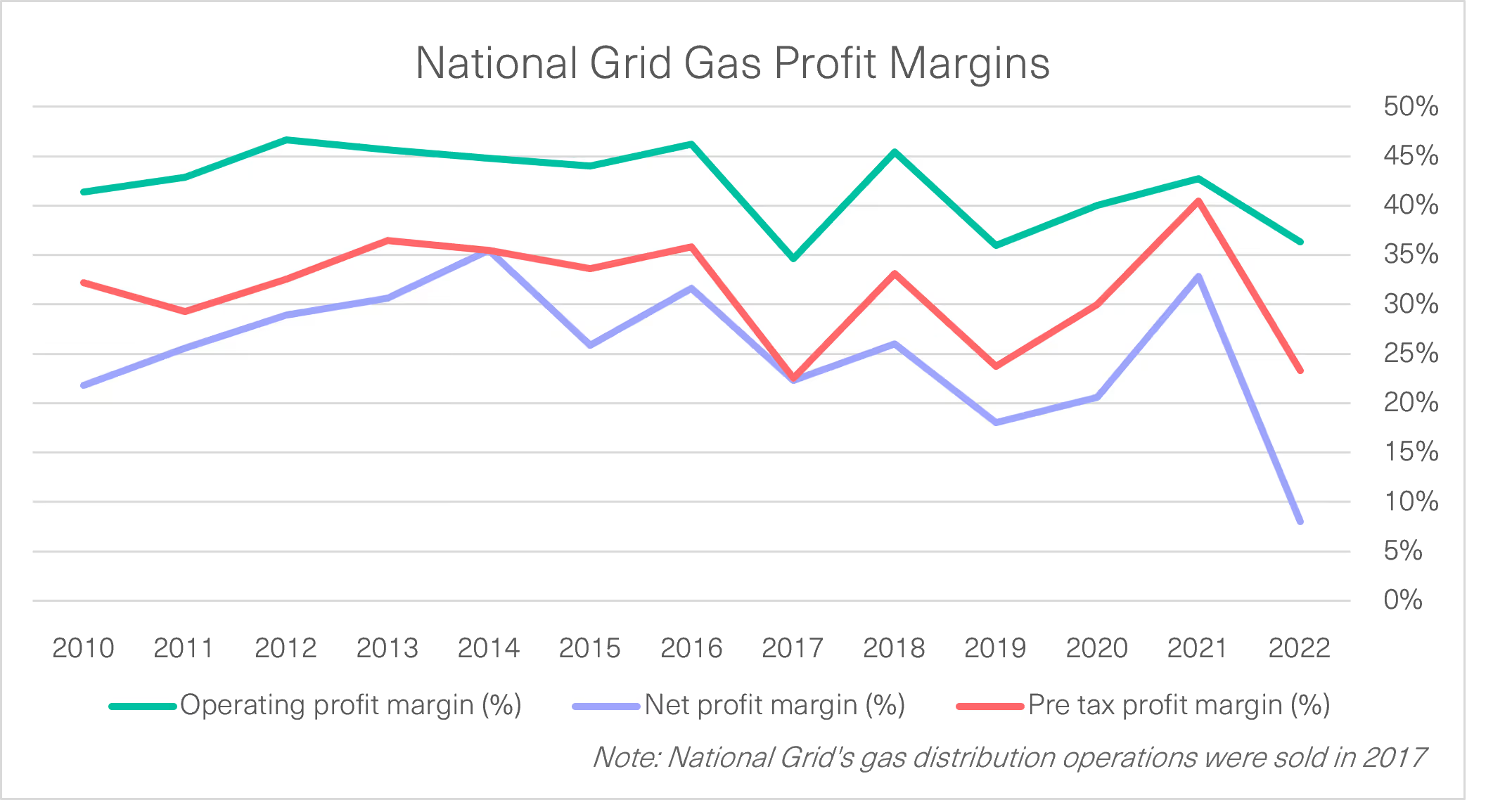

National Grid’s operating profit margins over the past year differed between business segments, with electricity (transmission and system operator) at 19% and gas at 36% in 2021/22. Figures 3 and 4 show how these margins differ across the company’s gas and electricity segments in Britain.

[.img-caption]Figure 3 National Grid Electricity Profit Margins[.img-caption]

[.img-caption]Figure 4 National Grid Gas Profit Margins[.img-caption]

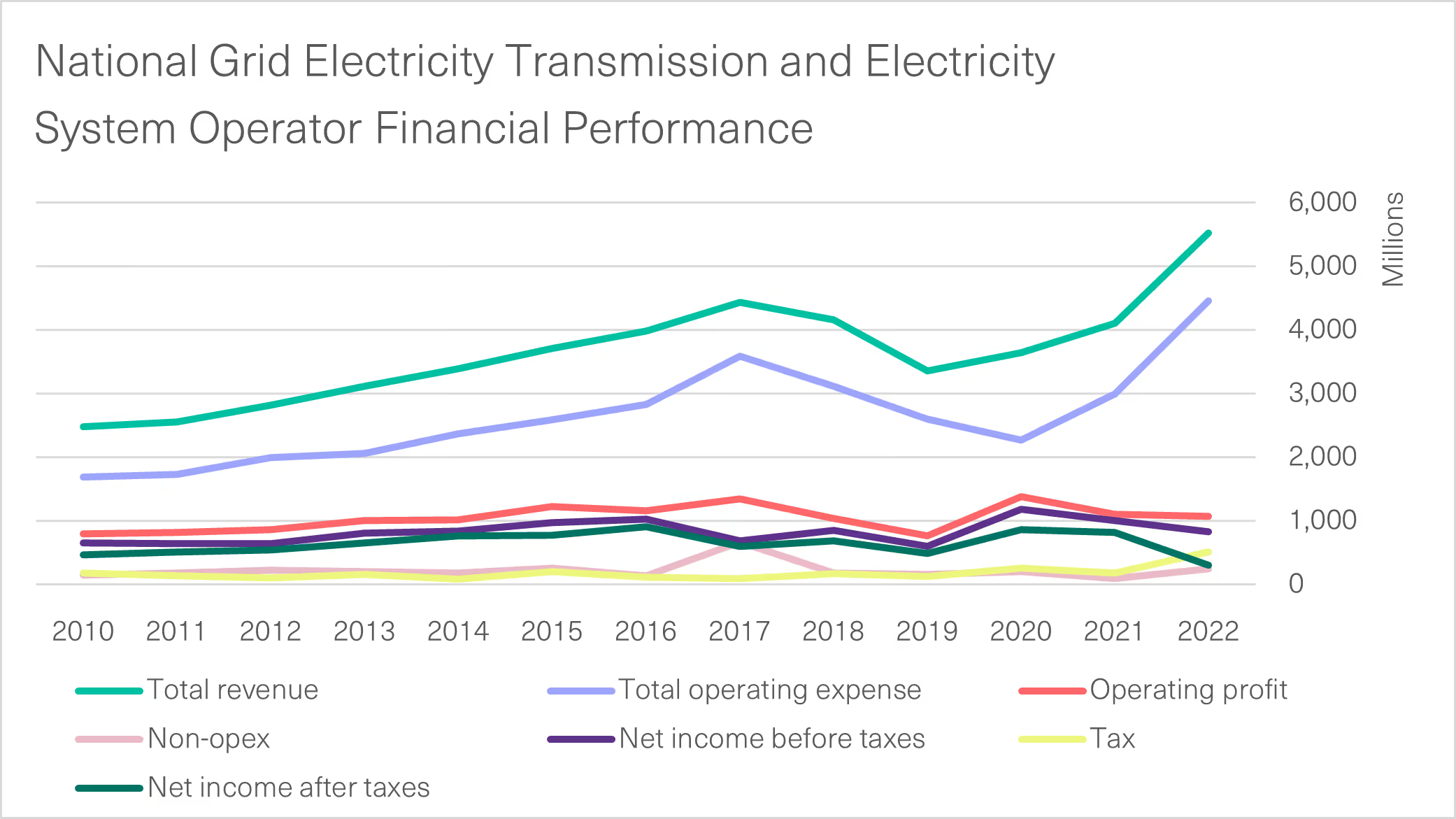

Figure 5, below, breaks down the constituent elements of these electricity segment's profit margins. As the figure shows, National Grid’s British electricity business has maintained a fairly steady operating profit since 2010. Of interest in this respect is the recent paired spike in both operating expenses and revenues.

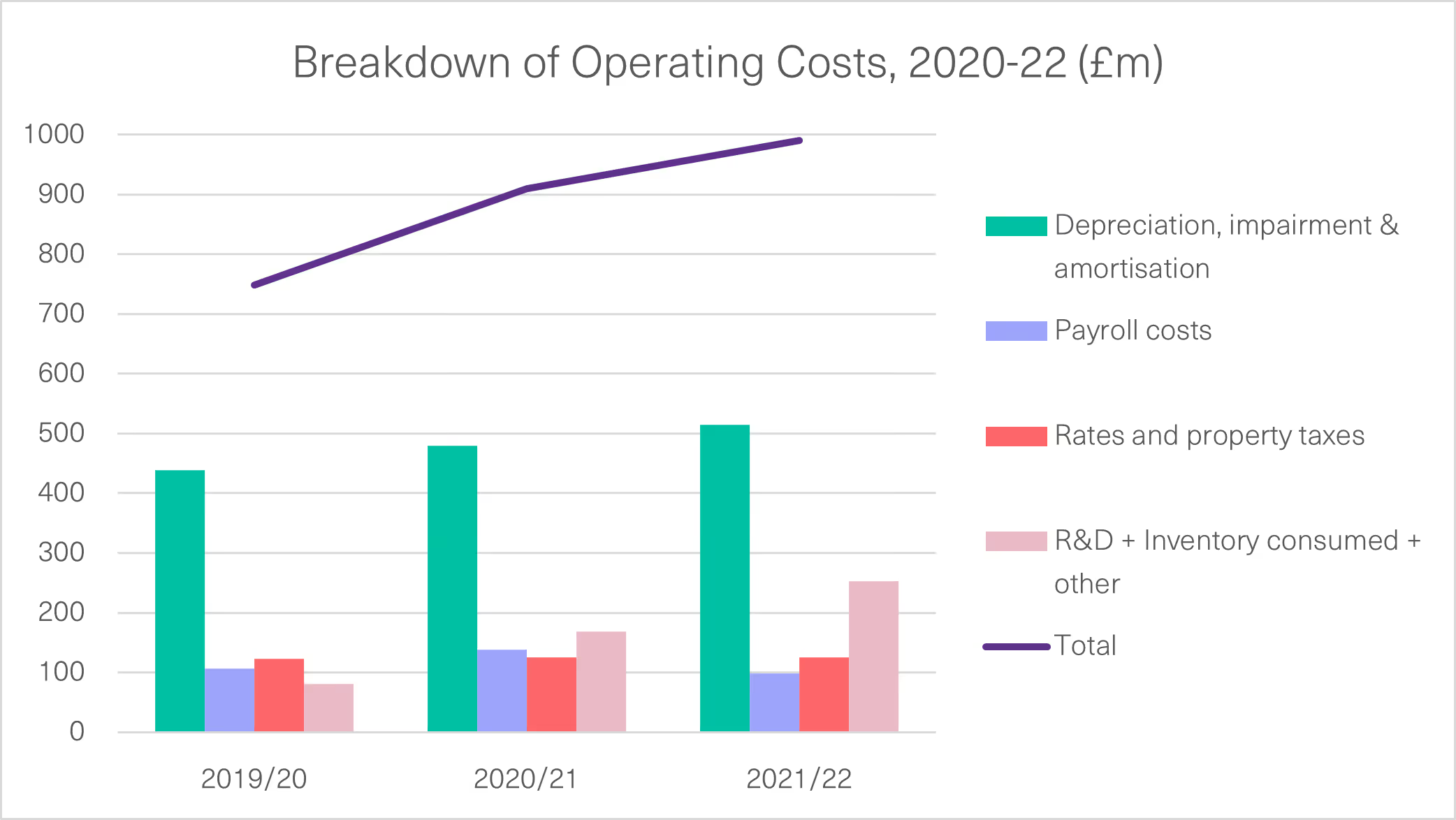

National Grid Electricity System Operator Ltd.’s most recent annual report notes a substantial rise in “balancing costs” (associated with the service of balancing supply and demand in real time) as the source of this spike, citing the crisis in Ukraine, effects of the Covid-19 pandemic, and a growing renewable share of generation as causal factors. The report notes balancing costs for FY 2021/22 were 139% of their £1.3 billion target. At the same time, National Grid Electricity Transmission reported an increase in operating expenditure between 2020 and 2022 related to “R&D + Inventory Consumed + Other” costs (Figure 6). Further details as to the nature of these costs, which accounted for roughly a quarter of their total op-ex in the most recent financial year, are not disclosed.

[.img-caption]Figure 5 National Grid Electricity Transmission and Electricity System Operator Financial Performance[.img-caption]

[.img-caption][.img-caption-header]Figure 6 Breakdown of Operating Costs, 2020-22 (£m)[.img-caption-header][.img-caption-text]Source: National Grid Electricity Transmission plc Annual Report[.img-caption-text][.img-caption]

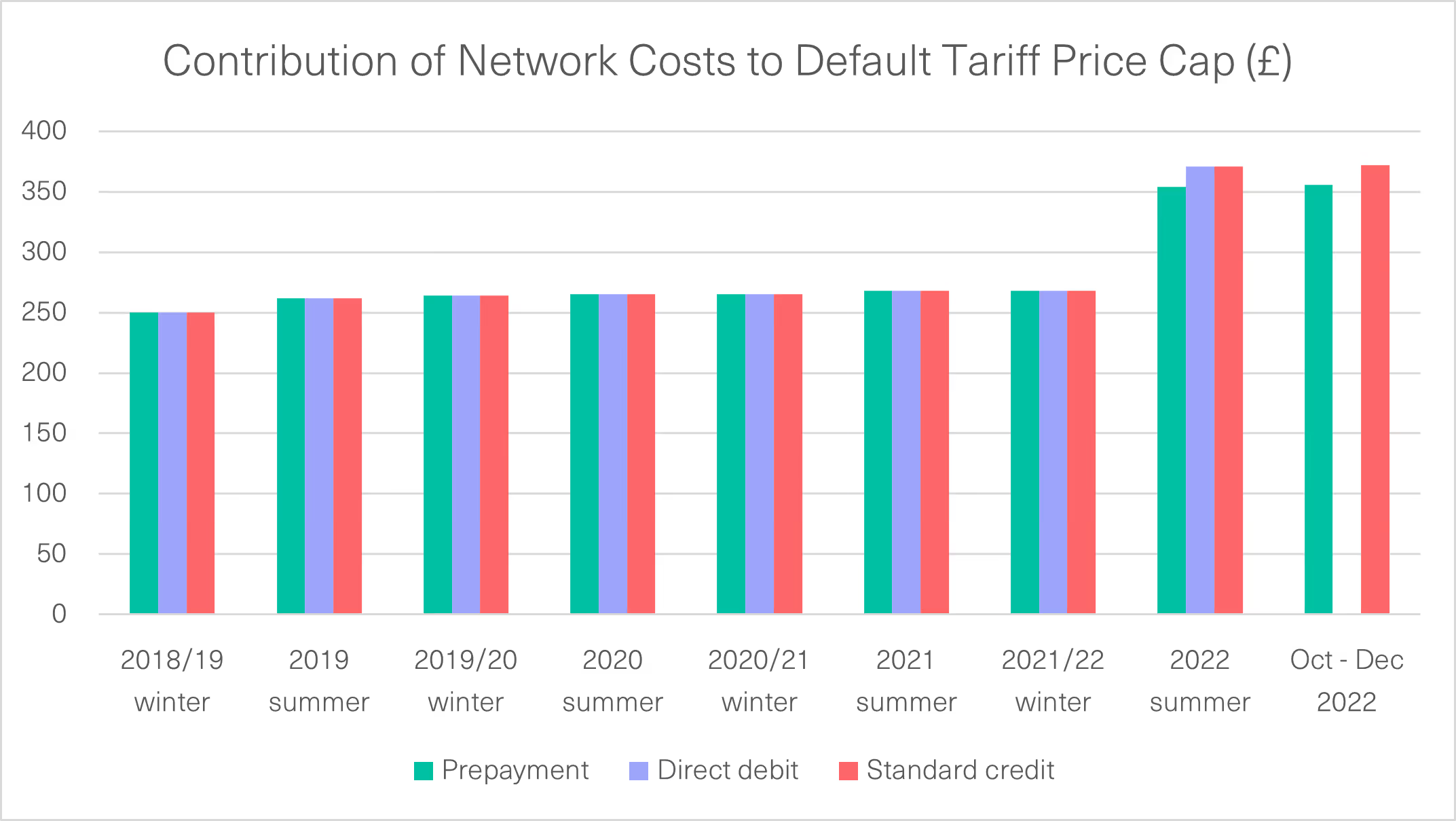

While the majority of the rise in the Ofgem price cap is attributable to rising wholesale costs, it is notable that there has been a substantial uptick in the scale of “network costs” within the breakdown of the price cap (see Figure 7). Specifically, between 2021/22 winter and 2022 summer, the total direct debit price cap rose by £694 or 54% (figure not shown). As shown in Figure 7, £103 (or 15%) of this jump pertains to a 38% rise in network costs. Meanwhile £549 (or 79%) pertains to the 104% rise in wholesale costs (not shown).

NB. Network costs include charges related to transmission, distribution, balancing, and, where applicable, exceptional levies.

[.img-caption][.img-caption-header]Figure 7 Contribution of Network Costs to Default Tariff Price Cap (£)[.img-caption-header][.img-caption-text]Source Ofgem[.img-caption-text][.img-caption]

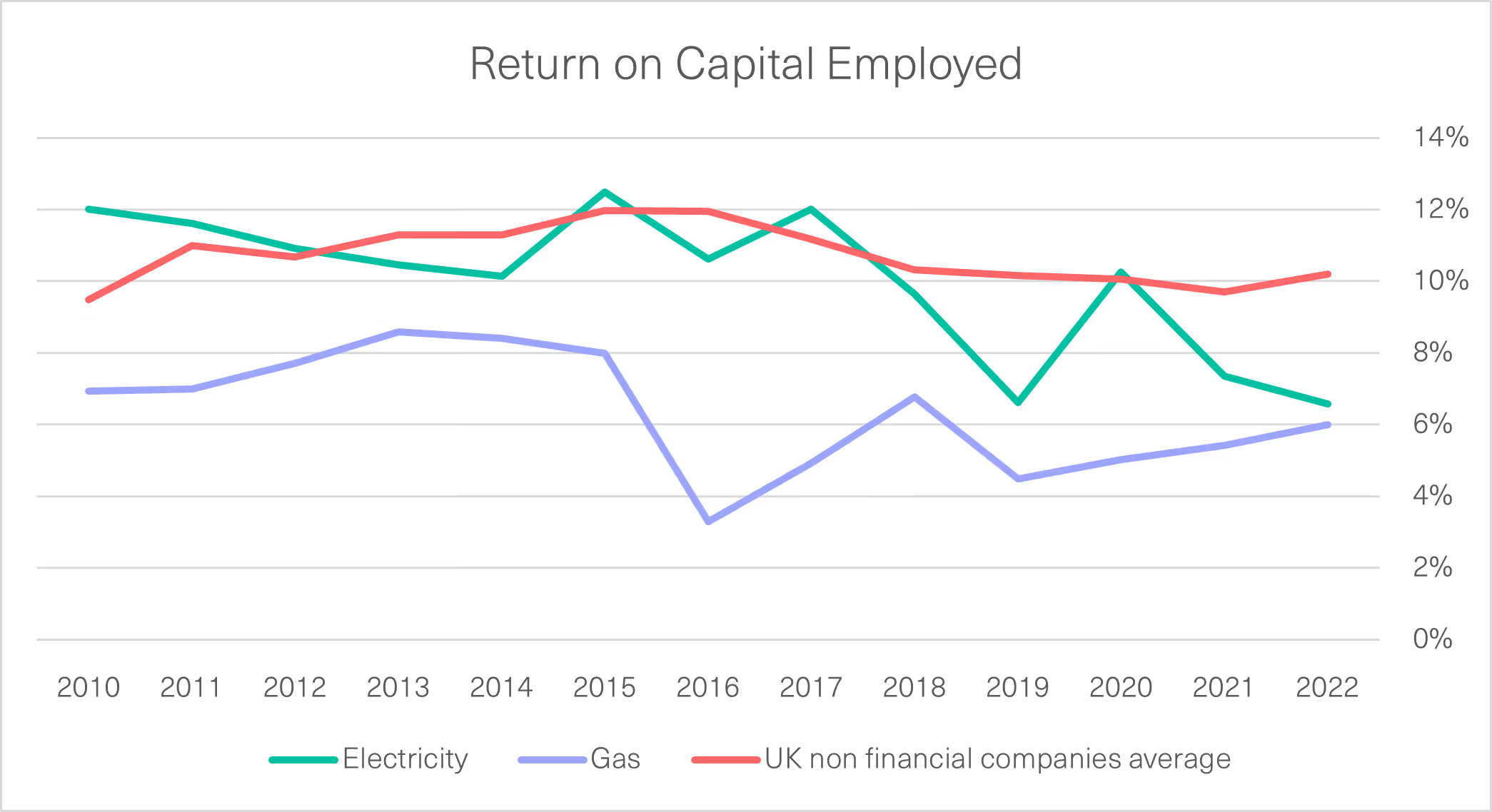

The indicator of profitability preferred by the Office for National Statistics (ONS) is the return on capital employed or “rate of return”. The figure below shows the rate of return for National Grid’s business segments, used by the ONS to measure profitability across the economy and calculated here using the ONS methodology outlined in the appendix.

As Figure 8 below shows, National Grid’s electricity segment has delivered a rate of return marginally lower than the national average over the past few years, having been broadly similar for the preceding decade. Their gas segment, by contrast, has delivered a consistently lower rate of return. In our clarifying note below, we discuss the different insights to be gleaned from differing measures of profit.

[.img-caption]Figure 8 Return on Capital Employed[.img-caption]

Return on capital employed (ROCE), which divides EBIT (earnings before interest and tax expenses) by total assets less current liabilities. Financial analysts often use this profitability metric to compare firms in capital-intensive industries, as it indicates how efficiently capital is being employed to generate profits, and therefore how lucrative it is likely to be for investors to park their capital (debt or equity) in a given company compared to alternatives.

We believe that a key concern should be the balance of affordability for users and the security and sustainability of energy provision. Thus, in contrast with ROCE, we are interested in how much of the revenue generated by British consumers is actually required in order to carry out the functions of National Grid’s electricity business.

The cost of physical capital is reflected in the income statement on an accruals basis (its overall cost spread out over its useful economic life) as depreciation, depressing EBIT via operating expenditure. The National Grid’s capital intensity therefore affects its ROCE both through its denominator and – in a more fictitious, paper form – through the numerator. Comparability with other industries’ operating margins and ROCE is therefore heavily affected by the depreciation policy used in its accounts.

To take the case of National Grid Electricity Transmission: a 6.6% ROCE (as in 2022) implies the company’s capital employed is equivalent to 15 years of EBIT, on an undiscounted basis. The 10-12% ROCE over the course of 2010-17 would imply only 8-10 years (undiscounted). By contrast, the stated depreciation policy for Electricity Transmission plant assumes a useful economic life of 15-100 years, and — if we assume a straight-line policy with a scrap value of zero — the relative size of their depreciation and amortisation expense implies an average life of 31 years. We note that their EBITDA for the year 2021/22 was equivalent to 9.8% of capital employed, having hovered in the 14-16% region throughout 2010-18.

At any rate, in the case of National Grid Electricity Transmission’s, an operating margin of 50% before interest and a pre-tax margin of 40% (after interest) suggests that a considerable proportion of the flows of income and expenditure are being cashed out in the form of profits.

ONS Methodology for Rate of Return

Net surplus = Operating profits (after Depreciation and Amortization

Rate of Return = Net surplus / (Total Assets – Current Liabilities)

Unless otherwise indicated, data for all figures in this briefing are sourced from Common Wealth analysis of Companies House filings or available data in the Refinitiv database.