Another digital world is possible. A 21st century digital infrastructure anchored in a nationwide full fibre network can provide the conditions for a more democratic, sustainable, and prosperous society. But delivering a full fibre future will require moving beyond the “regulatory state” and market-oriented approaches that have dominated the development of the UK’s digital infrastructure in recent decades - and which have led to the slow roll-out of full fibre, a deep digital divide, but a rich stream of dividends for private investors. Instead, a new set of institutional arrangements based on the democratic ownership and governance of digital, data and knowledge infrastructures is required to lay the foundations for a thriving society.

The building and maintenance of the full fibre network is ill-suited to a wholly market-led, for-profit model of provision. This vital infrastructure is characterised by high fixed costs and economies of scale that make its deployment unprofitable in rural or poorer areas and lead to underprovision; poor connectivity heightens the digital divide and reinforces stark regional inequalities. Deployment of full fibre exhibits classic market failures: cherry-picking, the failure to deliver universal service without subsidy, and damaging short-termism. The sector also suffers from poor coordination of investment, with costly and excessive duplication in some areas and severe under-provision in others; only 2% of households in the North East can access full fibre broadband, for instance, while roughly 50% of households receive their internet from early 20th century infrastructure. [1]

Companies owned by investors seeking to maximise returns are also structurally ill-equipped to deliver universal infrastructure efficiently and equitably, with their focus on maximising shareholder value over investing in the infrastructure needs of the country. The BT Group - including Openreach, the UK’s main network provider - paid out £1.5bn in dividends to shareholders in 2019 alone; indeed, for the past 20 years, the average annual dividend has been over £1bn (adjusted for inflation). At the same time, the level of investment in the telecoms industry over the past 20 years has been relatively flat in nominal terms, with the sector "sweating" existing assets rather than "significantly expanding the capital stock." [2]

As a result of relative under-investment, profit-driven incentive structures and poor strategic deployment, the UK continues to lag far behind other countries in the roll out of a full fibre network. Only an estimated 10% of households have full fibre connection, [3] while the UK was ranked 35th out of 37 countries assessed by the OECD for the proportion of fibre in its total fixed broadband infrastructure. [4] Critically, the government’s own Future Telecoms Infrastructure Review concluded that commercial markets would – at best – reach only 75% of the UK and take 20 years to do so, while reaching 100% coverage under market conditions would require significant government intervention, including billions of pounds of public subsidy. This uneven distribution of digital infrastructure exacerbates existing social and economic inequalities - only 47% of those living on a low income use broadband internet at home and one in five people in the UK are not digitally literate. [5]

Left to profit-driven telecoms firms, digital infrastructure is also likely to be designed to meet the needs of what is variously called "data extractivism", "data colonialism", or "surveillance capitalism", [7] a business model that is unlikely to deliver a digital landscape that is sustainable, privacy-enhancing, rights-preserving, decentralised, innovative and democratic.

To make the most of the power of digital technologies, we must change we organise our digital infrastructure and for what purpose. Digital infrastructure does far more than just connect us to the internet. Full fibre has the potential to deliver an immense productivity boost - estimated to be worth up to £59bn by 2025 - and can help close the UK’s stark regional inequalities. [8] This infrastructure is also the precondition for a growing number of essential services, including public WiFi, telehealth, urban transport and mobility systems, smart energy grids, and electric vehicle charging. It is likely to become even more significant with 5G technology, which enables more detailed, interconnected sensor systems. We cannot deliver a Green New Deal or build an economy that combines justice and prosperity without a modernised digital infrastructure.

A democratic 21st century digital infrastructure can also open up a more innovative and experimental future, from the creation of national data funds and collective data banks to intervening around algorithmic systems; from reshaping platform work to socialising “feedback infrastructures”; to exploring how data infrastructure can be remade as sites of participation around both local and transnational issues. Reshaping the UK’s infrastructure - digital and physical - can drive wider changes in social, economic and ecological relations, changing the purpose of connectivity - challenging exploitative platforms and algorithms and supporting alternative ways to use digital technologies that support the "progressive composition of a common world." [9]

Public policy should therefore seek to reshape how digital infrastructure is deployed and owned, as well as how data are produced and distributed, moving from conditions of private enclosure to a digital commons. We therefore propose treating digital connectivity as a societal right [10] and organising digital infrastructure – the rollout and maintenance of fibre optic connection and 5G in particular – as a vital 21st century public infrastructure. We propose two steps to that end:

[.num-list][.num-list-num]1[.num-list-num][.num-list-text]A new public infrastructure company tasked with rolling out a nationwide full fibre network by 2030[.num-list-text][.num-list]

The government’s own analysis suggests a monopoly provider would deliver a nationwide full fibre network faster and at significantly lower cost than via "enhanced competition" among private companies. To that end, Openreach (and the parts of BT Group relevant to rolling out the core network) should be taken into public ownership, with the new public infrastructure company tasked with rolling out full fibre by 2030. It should provider wholesale open access to the network for a thriving ecology of digital service providers and operators to emerge. Acquisition could be financed through issuing government bonds to shareholders equivalent to the value of shares in BT attributable to OpenReach. The public infrastructure company should be mandated to deliver a nation-wide full fibre network by 2030, with the level and quality of investment required to fulfil that mission set in coordination with the National Infrastructure Commission. A portion of funding for investment could come from charging private ISP providers for access to the network, just as Openreach currently does. Rather than paying dividends, the company should reinvest profits back into rolling out the network. The annual savings from dividends alone could cover over 16% of the Capex required to deliver full fibre over 10 years. To finance the remaining Capex requirements, the public infrastructure company should take advantage of near-record low-interest rates to borrow to invest in a critical public infrastructure.

[.num-list][.num-list-num]2[.num-list-num][.num-list-text]Ensuring accountability and democratic control[.num-list-text][.num-list]

We must go beyond ensuring equity of access and take steps to put our digital future back in public hands. This is particularly urgent in relation to the risk that public fibre provision could hand more control over data to state institutions that already thrive on excessive surveillance. Practical steps to achieving this should include:

We all too rarely think about the ways in which our social, cultural and political values are braided into the wires, coded into the applications and build into the databases which are so much a part of our daily lives.

In 2010, Google Fibre asked cities across America to compete against each other for superfast fibre broadband. [12] Hundreds participated, promising tax breaks or access to publicly-funded infrastructure in return. Sarasota in Florida even offered to rename itself to "Google Island." When Amazon launched a similar process last year to find their new HQ, [13] Tucson, Arizona sent Jeff Bezos a 21-foot cactus and New York City turned all its public lighting orange.

These stunts indicate the weakness of the public realm and its capacity to design infrastructures that work for people and planet. Hollowed out by neoliberal austerity, local and national governments around the world have become dependent on private companies, particularly tech firms, to provide investment and run key services and infrastructure.

The growing "techlash" against Silicon Valley has opened up debates about the questions of ownership and control in the digital economy. But little attention has been paid to the role of the digital infrastructure that enables flows of data, from fibre cables to mobile masts. This infrastructure is essential not just because it allows people to access the internet - find a job, access benefits, for children to do their homework, for elderly people to stay in touch with relatives - but also because it underpins essential services of the future such as "smart" energy grids, "smart" transport systems, e-health and tools for participatory democracy. How this infrastructure develops will shape the future of the digital economy - whether it will generate shared prosperity or deepen social and economic inequality.

The potential of a transformative upgrade in our digital infrastructure is clear: the Centre for Economics & Business Research estimates that nationwide full fibre would provide a potential boost to UK productivity worth £59bn by 2025, and analysis suggests it could create 600,000 new jobs across the UK. [14] Analysis suggests rapid, reliable connectivity could increase the number of businesses operating in an area by between 0.4% and 3.2%; an expected impact of between 0.3% and 3.8% increase in turnover per worker per annum; and significant consumer benefit as the number of services built off the back of full fibre increases. [15]

The benefits of full fibre is why the government’s Future Telecoms Infrastructure Review [16] has pledged a full fibre roll-out to every UK home by 2033, and why all major political parties have made pledges to extend broadband coverage as part of their manifesto commitments in the 2019 general election. The critical question is how to deliver it, who should deliver it, at what cost, paid for how?

Private providers have failed to meet critical targets relating to the development of foundational digital infrastructure. This year Google Fibre pulled out of Louisville (one of the few cities to get Google Fibre since its launch in 2010) leaving its roads badly damaged after a disastrous attempt to cut costs by laying cables in extremely shallow trenches. Leaving the roll-out of full fibre networks to market forces and duplicative private competition in the UK has led to similarly poor outcomes. The UK continues to lag far behind other advanced economies in the roll out of a full fibre network. Only an estimated 10% of premises have full fibre connection, the fourth worst coverage in the EU, [17] while the UK ranks 35th out of 37 countries assessed by the OECD for the proportion of fibre in its total fixed broadband infrastructure. [18] Critically, a Frontier Economics report for the government concluded commercial markets would – at best – reach only 75% of the UK and take more than 20 years to do so, unless there was significant government policy intervention, including billions of pounds of public subsidy. [19] This uneven distribution of digital infrastructure exacerbates existing class and racial inequalities - only 47% of those living on a low income use broadband internet at home [20] and one in five people in the UK are not digitally literate. [21]

The response to the slow deployment of full fibre from Ofcom and the government has been to funnel more funding into public-private partnerships, encourage the rolling out of FTTP (fibre to the premises) networks as an alternative to BT’s fibre to the cabinet (FTTC) approach, create more network-based competition, and to relax planning rules. This has encouraged the growth of alternative networks such as CityFibre and Hyperoptics – companies that often have highly concentrated, private ownership structures, which are now central to the government’s fibre roll-out plan, and which risk turning a vital piece of infrastructure into a source of further rent-seeking and financialisation in the economy.

The building and maintenance of vital infrastructure and universally accessible utility services such as the full fibre network is ill-suited to a wholly market-led, for-profit model of provision. This infrastructure is characterised by high fixed costs and economies of scale that makes deployment unprofitable in rural or poorer areas and leads to underprovision; poor connectivity heightens the digital divide and reinforces stark regional inequalities. Indeed, deployment of full fibre exhibits classic market failures: cherry-picking, the failure to deliver universal service without expensive public subsidy, and damaging short-termism. The sector also suffers from poor coordination of investment, with costly and excessive duplication of infrastructure deployment in profitable areas, and severe under-provision in others. Companies owned by investors seeking to maximise returns are also structurally ill-equipped to deliver universal infrastructure efficiently and equitably, with their focus on maximising shareholder value over - including distributing dividends to investors - over investing in the infrastructure needs of the country.

Openreach is the wholesale network provider that maintains the telephone cables, ducts, cabinets and exchanges that connect nearly all homes and businesses in the UK to the national broadband and telephone network, and is a functional division of BT, albeit divested into a legally distinct company. It has focused on deploying slower hybrid-fibre upgrades which are cheap and relatively quick to rollout in comparison to FTTP, which is much faster, but more expensive and slower to deploy. Openreach’s efforts to roll out full fibre have been generally viewed as a failure - it is estimated that at the current rate of deployment it will take around 30 years to achieve a full fibre roll-out across the UK.

Alongside inadequate delivery of vital utility services and infrastructures, our existing model of provision and ownership generates a number of poor social, environmental and economic outcomes: digital redlining; the proliferation of carbon-intensive technologies; the environmental costs of unnecessary duplication; oppressive systems of surveillance and social control; and undemocratic ownership and governance of essential services. Uneven provision is also a "driver of geographic disparities", with only 2% of households able to access full fibre broadband in the North East and 4% in the East of England, compared to 11% in London and the South East. [22]

Another digital world is possible. A progressive vision is needed for the role that digital, data and knowledge infrastructures can play in creating the conditions for shared and sustainable plenty. Digital infrastructure does far more than just allow us to access the internet on our phones or computers. This infrastructure is the foundation on which a growing number of essential services are built, including public WiFi, telehealth, urban transport and mobility systems, smart energy grids, and electric vehicle charging. It is likely to become more significant with 5G technology which enables more detailed, interconnected sensor systems.

The need for an alternative model of deployment that is faster and fairer is thus of vital importance: without control over the infrastructural foundation, transitioning to less profit-driven, more socially useful models in these other sectors may well be impossible. With the need to remake our economy in the pursuit of a just transition as part of a wider Green New Deal, these technological capabilities are more vital than ever.

The question of who should own and build the new digital infrastructure is therefore not just how quickly we can connect more people to the internet. It is a question of the values shaping what kind of infrastructure is built. Left to profit-driven telecoms firms, digital infrastructure is likely to be designed to meet the needs of what is variously called "data extractivism", "data colonialism", and "surveillance capitalism". Whatever its name, the method remains the same: monopolise control of data-generating infrastructure, gather as much data as you can and then devise ways to monetize that data down the line, with technical systems designed for profit over the needs of people and planet.

While an approach focused on private provision and competition might achieve the highest possible return on investment for a select group of investors, at least in the short run, it does not naturally align with meeting the public interest of digital infrastructure that is sustainable, privacy-enhancing, rights-preserving, decentralised, innovative and democratic. Given that digital infrastructure increasingly underpins so much of our social, economic and civic life, a system with such limited democratic oversight, control and public participation is no longer tenable – and in deep tension with a wider goal of socialist transformation.

Instead, public policy should seek to reshape how foundational digital infrastructure is deployed and owned, as well as how data are produced and distributed, moving from conditions of private enclosure to a digital commons. To that end, we propose treating digital connectivity as a 21st century right [23] and organising digital infrastructure – the rollout and maintenance of fibre optic connection and 5G in particular – as a public good. This requires reimagining how these technologies are developed and used; a new vision for how the digital revolution can deepen justice and prosperity stressing technical infrastructures and the value they generate are a collective accomplishment made possible by complex and connected layers of public and private infrastructure and investments, in people, machines, software, standards, processes, practices and cultures. These complexities require policymakers and the public to think more critically about how digital infrastructure and data-worlds are created and to act to shape them in ways that deepen their potential to generate shared value. [24]

In particular, it requires moving beyond the “regulatory state” and market-oriented approaches to building and maintaining a democratic and sustainable 21st century digital infrastructure and toward a new set of institutional arrangements around the democratic ownership, governance and capacities of digital and data infrastructures.

AB Stokab - owned by the City of Stockholm - was formed in 1994 as a public infrastructure company, tasked with maximising IT development in the region. The deployment of the network was initially funded by public-backed loans. "Today, some 90 % of all Stockholm’s households and nearly 100 % of all companies have FTTH connections with speeds of up to 1 Gigabit-per-second," with the network open to all parties, on equal terms. All financing comes through earnings and loans; the company has never used tax receipts to finance deployment. Over 100 operators and service suppliers use Stokab’s network to deliver their services. The underlying infrastructure has enabled a flourishing tech ecology, with Stockholm-based tech companies, such as Skype and Spotify. [25]

Broadband for the Rural North (B4RN) is a successful community-led initiative to bring full fibre connection to rural Lancashire. The not-for-profit community benefit company launched in 2011 and has connected over 5,000 homes, delivering the world’s fastest rural broadband.

In October 2019, Hull became the first city in the UK to make full full fibre broadband available to all residents. This was delivered by KCOM, a company which has a near-monopoly on the provision of Internet and telephone services in the region, related to a historical fact that the Hull area has no BT landlines.

Australia launched a publicly owned National Broadband Network provider in 2009 with the goal of delivering a full fibre network. However, there are important differences with our proposal. In particular, Australia the policy involved set up a new infrastructure provider, so the implementation period was much greater, delaying roll out; the technical goals shifted mid-way through from delivering fibre-to-the-premises to the majority of homes to fibre-to-the-cabinet; the physical geography of Australia - 32 times the size of the UK was a factor; and there was greater emphasis on private sector involvement with fewer economies of scale. [26]

With the growing intensity of data use, expected increases in demand for data, and the expanding number of "smart" devices and technical systems connected to the internet, superfast broadband isn’t enough. Instead, there is a growing consensus, from the National Infrastructure Commission to Ofcom, that the UK must upgrade its digital infrastructure, away from a reliance on copper wires to a full fibre network. Indeed, it will be impossible to meet vital social missions - such as the rapid and just decarbonisation of the economy - without such an upgrade.

Copper cables, also known as asymmetric digital subscriber lines, transport data in the form of electrons. Fibre cables consist of thousands of individual glass fibres, as thin as a human hair, which carry data in the form of light photons instead of electrons. This means that signals don’t weaken over long distances.

The architecture of a fibre network is similar to that of a mobile network. Fibre connections between premises and local exchanges (or cabinets) in the FTTP access networks are equivalent to the wireless connection between handsets and mobile masts in the radio access network. There are three key components to fibre networks:

That access network can be further broken down:

In 1974, Peter Cochrane, BT’s Chief Technology Officer, was asked to do a report on the UK’s future of digital communication and what was needed to move forward. His conclusion was to forget about copper, which was unsuitable for digital communication in any form, and get into fibre, so BT started a massive effort - that spanned 6 years - involving thousands of people to digitise the network and put fibre everywhere. The country had more fibre per capita than any other nation and two factories manufacturing the components for systems to roll out to the local loop.

But in 1990, the then Prime Minister, Margaret Thatcher, decided that BT’s rapid and extensive rollout of fibre optic broadband was "anti-competitive" and wanted American cable companies providing the same service to increase competition. The factories were sold to Fujitsu and HP and the expertise was shipped out to South East Asia. So in 1991, the roll out was stopped and the UK fell far behind in broadband speeds. To this day, we have ever properly recovered. While Japan and South Korea went on to develop world class infrastructure with over 95% full fibre coverage, as Dr Cochrane puts it, “in the UK there’s no vision, mission or plan, we’re engaged in a random walk into the future.” [30]

Providers of full fibre do not typically sell directly to consumers but instead lease their fibre lines to companies in the broadband market (with the exception of Hyperoptic). The main ISP providers include BT (PlusNet, EE, 9 million subscribers) Sky Broadband (6 million subscribers) Virgin Media (5 million subscribers) and TalkTalk (4 million subscribers). Of the ISP providers, Virgin Media is the only provider with its own fibre network.

In addition, wholesale providers sell bandwidth to mobile phone companies to connect masts; the launch of 5G networks will substantially boost demand for fibre across the country meaning control of this infrastructure will likely grow in economic importance. Critically, while 5G will be an important part of the UK’s digital future, it is less reliable than full fibre, and more to the point, full fibre is crucial and beneficial for fibre-fed 5G; it is not a case of either-or, but both together to deliver 21st century connectivity.

5G uses higher-frequency bands than current 4G LTE connectivity, which enables denser transmission of information, but over a shorter range. Despite relying on a cluster of new technologies, 5G will also build on dense full fibre networks, as they require a large number of small transmitters in close proximity to each other across network coverage. Essentially, 5G technology builds on top of existing fibre infrastructure, and cannot be separated from discussions about fibre systems. 5G will be particularly important for infrastructure networks and the “Internet of Things” related to transport and healthcare systems, automating technologies, as well as consumer products, such as faster streaming and more seamless wearable technologies. [31] By enabling more efficient communication between sensors, databases, and users, 5G will open up new pathways for research and development.

The related cost of 5G is not linear as the costs increase exponentially for the hardest to reach proportion of the population, and is dependent on factors such as the extent of infrastructure sharing; however, estimates suggest £1.5 to £2.5bn annual investment could see 5G reach 90% of the population by 2027 with 50 Mbps. [32]

Together, full fibre and 5G are foundational infrastructures of successful 21st century digital economies and societies.

Reports in October 2019 indicated that Boris Johnson would be allowing Huawei to help to develop 5G network capabilities in the UK. The sections of the network which Huawei would be involved with have been variously described as “non-contentious” [33] or “non-core” [34] however it remains unclear which sections that would involve, and what kind of data access that could provide the company. As it stands, the government has argued that UK firms lack the technical capacity to develop a working 5G network and that it is necessary to contract Huawei to help build those elements of the network. [35]

There are serious concerns about the security and resilience of these networks with a Huawei contract. While arguably there has been a tendency to overstate the significance of Huawei’s threat to national security, a number of concerns are worth considering especially in relation to debates around ownership. The four mobile phone operators who have been developing 5G capabilities – Vodafone, EE, O2 and Three – have already embarked on contracts with Huawei, which is building various equipment components for 5G infrastructure. [36] At this point, blocking Huawei’s involvement in 5G development would see costs to the UK economy ranging from £4.5-£6.8bn, according to some estimates. [37] The UK’s inability to respond quickly to new technologies on a large scale has left the country’s infrastructure largely reliant on external (state and private) corporations to fill critical infrastructure gaps and make decisions that are crucial to long-term economic planning.

The biggest viable threat is a data breach, which could involve espionage or data hacking. Through the installation of a backdoor in the UK’s 5G infrastructure network, Huawei would be able to access data travelling through the 5G network, which could in turn give the Chinese state access to this data. [38] Huawei has denied sharing intelligence data with the Chinese government. [39] And UK government sources have said that the UK is equipped with the necessary technologies to secure itself against possible breaches. [40] A report by the Royal United Services Institute has drawn attention to China’s history of cyber attacks, the ease with which a backdoor could be placed in new digital infrastructure compared to older systems, and the refusal by a number of other UK allies to work with Huawei, which could pose a whole other set of concerns. [41] Data security and privacy remain an unresolved issue: ultimately, the only way to guarantee national security and data protection is by forging more autonomous technological capacities in the UK.

The core case for transforming ownership of the full fibre network is the same as for other fundamental near-monopoly physical infrastructures [42] : the network is crucial for economic and social development, reflected in the UK government’s classifying it as a "critical national infrastructure" in 2017; however, private companies exploit monopolies to make excess profits by overcharging customers and extracting profits from the business rather than re-investing, meaning that critical infrastructure will not be delivered in a timely or equitable manner.

Noticeably, the level of investment in the telecoms industry over the past 20 years has been relatively flat in nominal terms. As stated in the Frontier Economics report:

The only significant variation around the trend reflected the dotcom boom in 2000 and subsequent bust, and a similar if smaller rise and fall either side of the 2008 global financial crisis. This stability in investment, despite rapid growth in output, is consistent with increased demand being met by "sweating" existing assets rather than significantly expanding the capital stock. It also indicates that investment has not been constrained by a lack of industry growth or expectations of growth. [43]

Private ownership of core utilities prioritises rewarding investors via rising dividend distributions and share prices, not reinvesting in better services. Given interest rates are higher for private companies than they are for government, the cost of borrowing for investment by private companies is higher. And there are the extra costs of creating and regulating an artificial market, a regulatory framework which often fails to ensure adequate levels of investment or coordination, to the detriment of consumers and businesses.

Private control of scarce assets and infrastructure by a small number of companies has enabled the growth of rentierism, with rent "derived from the ownership, possession or control of scarce assets and under conditions of limited or no competition." [44] This has not occurred by chance: post-1970s, policy approaches related to asset ownership and property rights have been conducive to the creation of scarce commercial assets from which significant economic rents can be extracted. The telecoms sector - which provides a fundamental infrastructure on which we all depend - is a critical example of the subdivision of the "economy into a series of sinecures upon which large firms stake their claims, protected from competition by watertight rights over scarce resources." [45]

Private ownership of vital utilities is also associated with a series of problematic behaviours, including a drive to reduce labour costs, hostility to unions and reducing pension security; efforts to externalise social and environmental costs as much as possible; the enshrinement of shareholder value and returns above all other considerations; accelerating inequality through both exorbitant salaries for executives and the funnelling of profits to a small group of elite shareholders; the use of off-shore tax havens and other tax avoidance mechanisms; and the establishment of an incentive structure that promotes financial speculation over productive investment. [46]

Regarding the development of the UK’s broadband infrastructure, and the future of fibre in particular, the dominant player OpenReach has invested £13bn into its network over the last decade. However, at the current rate it will take Openreach around 30 years to achieve a full fibre roll-out across the UK. During that period, it has consistently offered 15% return on equity to investors, prioritising paying significant dividends to shareholders over investing in the infrastructural needs of the country. In other words, large chunks of cash generated by a company operating in a near-monopoly position that could be invested in improving digital infrastructure for the general public end up in the pockets of private investors.

Even with a new wave of smaller providers coming on line, there are substantial issues concerning equity, security, and cost. CityFibre, an alternative provider of wholesale fibre network infrastructure which is central to the government’s strategy for delivering fibre network,was acquired this year for £538m by Antin Infrastructure Partners and West Street Infrastructure Partners, a fund managed by Goldman Sachs. [47] Seven financial institutions have backed the first phase of CityFibre’s UK investment plan with a £1.12bn infrastructure debt package, with the company seeking to acquire FibreNation, another full fibre provider owned by TalkTalk.

Vital parts of the UK’s infrastructure are therefore in the hands of substantially unaccountable actors, operating to the rhythm of financial over social needs. While these companies may, with appropriate regulation, have a role to play in developing the UK’s digital infrastructure, their current structures and incentives - opaque, financialised, focused on profit-maximising - are likely to reinforce the behaviours and outcomes that private control of digital infrastructure has already generated.

It has also been demonstrated that the digital divide reproduces racial, gender, and class inequalities. [48] For example, 17% of people earning less than £20,000 never use the internet, as opposed to 2% of people earning more than £40,000. [49] While the "access" divide refers to the uneven distribution of broadband infrastructure, there is also a divide in "use" and "adoption" which reflects the unequal diffusion of information technology skills. [50]

These concerns are particularly pertinent in the context of the government’s "digital by default" plan whereby services such as Universal Credit can only be accessed online. This approach has been deeply problematic for many of the poorest and most vulnerable people in receipt of benefits, and requires both digital and non-digital training and support to address, alongside wider reform of the welfare system.

The unequal distribution of new technologies will only exacerbate the problem further. Due to the shorter wavelength of high-frequency bands and the subsequent need for extensive fibre cable infrastructure expansion, 5G technology poses a particularly difficult challenge. [51] In the race to roll out the latest technology, 5G has already followed patterns of unequal internet connectivity. So far, 5G has only been launched in cities, and even then, some neighbourhoods remain underserviced. [52]

In the race to create a return on investment, the industry will compete to develop infrastructures of hyper-connectivity, enabling as much data as possible to be mined from people and places so that it can then be sold.

The ICT sector already uses 50% more energy than global civil aviation, [53] and the demand for increased bandwidth with the rapid roll-out of ubiquitous connectivity (or the "internet of things") enabled by digital infrastructures will exacerbate this.

Several models have noted the carbon-intensive nature of 5G infrastructure when provided by private broadband companies. [54] Typically, the response by industry is to focus on the potential of 5G to reduce emissions in the sector as a whole through smart sensor technology. [55] However, coordinated planning can allow for a more in-depth response and coordinated effort for a less-carbon intensive rollout of 5G. A national, ”green” public rollout of fibre infrastructure for 5G technology can be integrated as part of a Green New Deal, utilising green transport systems and battery technology, to drive a just decarbonisation of society.

These same high-yield infrastructures of ubiquitous hyperconnectivity also contain the technical capacity for social control, surveillance, predictive modelling and other potentially dystopian ends. Indeed, connectivity is often accompanied by concerns around data capture, commodification and surveillance (including "surveillance capitalism"). Public WiFi, IoT sensor networks [56] and other infrastructures of data extraction are likely to continue to concentrate power in the hands of state and private actors, often in the context of disproportionate monitoring and management of working class communities and communities of colour. [57]

Algorithms already aggregate data from multiple sources rank and rate people to determine what they get access to and the conditions of that access: from sorting job applications and allocating social services to accessing insurance and loans. [58] As the government intensifies the "hostile environment", digital tools such as a new "Status Checking Project" [59] are increasingly employed for immigration enforcement while legal loopholes deny migrants basic data protection rights.

High-tech surveillance also features in almost every "Smart City" plan. CityFibre highlight that while traditional DSL-network based CCTV infrastructure, “limits the ability to support bandwidth hungry camera equipment” [60], their dark fibre infrastructure will provide limitless capacity for new surveillance infrastructures. As private companies discreetly spearhead the roll out of facial recognition technologies in sites across the UK, campaigners have warned that authorities should follow in the footsteps of American cities and ban this “tool of oppression.” [61]

Ensuring new technologies and technical systems dismantle existing inequalities and forms of oppression - rather than amplifying them - will require reimagining not just how digital technologies are developed, but how their deployment and use are governed and by whom. A democratic digital infrastructure should bake into its design and operation protections of privacy and digital rights and ensure that technologies that can be easily abused are not built.

Utilities, transportation, education and health are increasingly mediated by smart technologies run by tech firms, meaning cities and governments hand over the management of public infrastructure and services to unaccountable private players.

Francesca Bria argues that because digital infrastructures function as a "meta-utility" (mediating the provision of services in many other domains from energy to transportation, education and health), it is necessary to consider the “path-determining nature of many smart technologies." [62] In other words, without control over digital infrastructure it may be impossible to push for alternative ownership models such as remunicipalisation campaigns in these other domains, or to drive rapid decarbonisation via smart grids and decentralised, zero carbon energy production.

Ultimately, the undemocratic nature of private broadband providers makes for a deficit in accountability. Because of the tendency towards monopolistic service, providers are able to operate with poor customer responsivity. A recent report by CityFibre surveyed broadband customers across the UK and found that most ISPs were actively deceiving customers, claiming fibre services despite the continued use of copper cabling, blaming the Advertising Standards Agency for failing to enforce regulations around broadband. [63] In the United States, ISP monopolies have driven the erosion of net neutrality, inflated costs to customers, and provided increasingly inadequate service and uneven access throughout the country. [64] In 2017, the United States Congress overturned a crucial privacy protection, passing a resolution overturning an FCC rule that required internet providers to get customers’ permission before they shared their browsing history, opening up ISPs’ ability to sell customer information, including browsing history and location data. [65]

Sidewalks Labs in Toronto demonstrates how all these risks can collide when one company owns the digital infrastructure that underpins the running of an entire city. Sidewalks Labs, a subsidiary brand of Alphabet (Google’s parent company) wants to use digital tools to build cities for “urban innovation”, aiming to solve urban issues such as “longer commutes”, “higher rents” and “fewer opportunities” through technology.

They claim that they will make available to the public much of the data collected in public spaces like parks and streets, as well as data from publicly accessible private spaces like buildings and stores. But you cannot "opt out" of public spaces and the Sidewalks’ plan envisions no "surveillance-free zones." [66]

Just because data is publicly accessible does not mean that everyone can equally access, store or process the data to deliver products and services. Companies with significant stores of proprietary data, algorithmic modelling capacity and commercial distribution infrastructure have a distinct market advantage (Sidewalk Labs, for its part, is in a privileged position as it can draw upon Google’s vast resources in data analytics).

Sidewalk Labs is emblematic of the way in which Big Tech companies are taking over responsibilities traditionally provided by governments, and further encroaching into physical urban space. Eric Schmidt, who was until recently the CEO of Alphabet, has notably described how the idea for Sidewalks Labs came from Google’s founders getting excited about "all the things you could do if someone would just give us a city and put us in charge." [67]

This model of creating our urban future is also an insidious way of handing more control - over people, places, policies - to profit-driven, power-hungry corporations. Municipal governments who have been heavily defunded by austerity have turned to public-private partnerships with the tech sector in order to build more efficient services as a cost-saving measure. [68] Legal scholar Frank Pasquale has described how urban citizens will be increasingly “subject to corporate rather than democratic control” affecting the means of social reproduction, from renting apartments to transport. [69]

Instead of leaving the development of digital infrastructure to the interests and time horizons of powerful corporate actors, we should start from how best to meet the needs and expand the capabilities of ordinary citizens, and then intentionally design digital infrastructure to serve these ends. Decisions on how we design digital infrastructure are political - the pervasiveness of digital infrastructure in modern society means it decisively shapes the distribution of power and organisation of work and materials in society - the fundamentals of politics. As such, how digital infrastructure is organised, and to what ends, should be open to democratic contestation, with a clear emphasis on meeting key social goals. We therefore propose five key priorities that should dictate the design of digital infrastructure to serve citizens.

Getting online enables people to access essential public services, to learn, to find work, to connect with family and friends and ultimately to participate in modern society. Ensuring equity of access involves several factors including the speed and quality of the connection and the extent to which people are able to make use of it. A national mission to connect the public to full fibre by 2030 is thus a vital and powerful goal for a more equal, innovative society.

Access to the internet has become indispensable to full participation in society; the prevailing assumption that connection should be provided by private corporations rather than as a public utility should therefore be questioned. [70] Indeed, legal scholars have recently argued that broadband access should be organised as a human right with guaranteed access for all, rather than provided primarily by market mechanisms. This reflects the fact that rights evolve and are updated; as such, a right to internet access should be reconceived as a key 21st century right. As Ewan McGaughey argues, technological rights must include everything to ensure people can fully participate in society, where "the free and full development of [our] personality is possible," with the right to broadband a cornerstone of the right to freedom of expression in today’s society." [71] An analogous updating of rights for the digital age is the right to personal data protection, a 21st century updating of the right to privacy.

The provision of broadband for free as a social right paid for through taxation, rather than a commodity, is also a central argument of the wider Universal Basic Services (UBS) agenda: “taking basic needs out of commodified relations and overcoming the crisis of "access" to basic needs beyond the realm of waged work, it revives the relevance and scope of state provision not only to ensure equitable access, but to enable economies of scale and scope.” [72] This reflects the fact that changing infrastructures - digital, material, legal - can also drive wider changes in social relations. Rethinking the architecture of ownership can therefore alter more than just the means of connectivity (simply switching providers), becoming part of a broader programme of changing economic, social and ecological relations.

Fibre connection free at the point of use as a core plank of a UBS agenda - while beyond the scope of this report - would significantly reduce the cost of living for those on low incomes, is progressive because it is worth more to poorer households as a proportion of their income, improves connection and reduces insecurity. As UCL’s landmark report into UBS argued, a "service-orientated model meets needs more directly, increases efficiency, reduces costs, facilitates a vibrant private economy, and buttresses the institutional fabric of society." [73]

It is important to recognise that we need not engage with the internet as purely passive service users. Rather, digital technologies can function as important tools to allow ordinary people to engage directly in decision making, and grant them a stake in the world that the internet is helping to build.

For instance, participatory budgeting began more than a decade ago in Southern Brazil as a novel process which allows citizens to present their proposals and priorities through collective debates and voting to determine the allocation of public welfare investments. Participation reaches 40,000 citizens per year including low-income groups, and the process has so far led to the construction of improved sewer and water infrastructures.

This practice has been replicated around the world with varying degrees of success. But new digital technologies employing mass participatory tools and "Big Data" analytics offer an exciting opportunity for cities, towns and rural communities to enact participatory systems cheaply and effectively. It also offers the opportunity for new forms of efficient social coordination and non-market planning.

And it is not just in political democracy: digital technologies, properly organised, can help rebalance power in the workplace and allow for effective organising, putting in place a building block for the deepening of economic democracy.

Decidim.Barcelona was developed with open source software and allows city organisations to run open budgeting and policy co-creation projects. It has 27,000 registered users presenting over 11,700 proposals. One of the best use cases has been the involvement of neighbourhood groups and citizens in the urban planning process through offline citizen assemblies and the online platform. They collectively drafted a mobility plan based on "superblocks" and care free zones to curb excessive air pollution, lower noise levels and reduce traffic by 21%. [74]

In Reykjavik, Icelanders can use the online platform Better Reykjavik, to have their say on local issues ranging from school opening times to local infrastructure. It is built on "Your Priorities", open-source software developed by the Icelandic Citizens Foundation that enables groups of people to develop and prioritise ideas and decide which ones to implement. So far, almost 60% of citizens have used the platform, and the city has spent £1.9 million on developing more than 200 projects based on ideas from citizens. The software has also been used for the Rahvakogu (People’s Assembly) project in Estonia where 50,000 citizens used it to submit more than 20,000 proposals to government. More recently, they launched a new service called "Active Citizen" that uses augmented interfaces to combine online and offline citizens’ assemblies making it easier to participate." [75]

As part of a transformative agenda to decarbonise the economy, digital technologies will play an increasingly critical role in supporting new systems - heating, energy, transport, and economic coordination - that are efficient, resilient and frequently based on a decentralised approach to the generation and distribution of resources. Digital technologies can therefore help develop systems for less carbon intensive cities and towns, for ways of living and working.

The prospect of 5G in particular represents an opportunity to further embed sensors in the city’s infrastructure to more effectively monitor and manage water, energy, air pollution, and bicycle, pedestrian and vehicle traffic flow via improved feedback loops. The collection and analysis of relevant datasets can therefore help better coordinate and manage all of a locality’s services.

To date, there has been a lack of real time information about energy consumption, with forecasting estimates used to anticipate and balance supply and demand. As variable sources of renewable energy continue to enter the energy grid, improved control and predictive ability as to energy supply and demand will be vital. A series of technological innovations – including decentralised, small scale electricity generation and storage; smart meters that measure and communicate consumption; and artificial intelligence to optimize systems – are making it possible for electricity and information to flow both ways. This more dynamic, decentralised system is referred to as the "smart grid", and should be supported by a nation-wide full fibre network to realise its potential and ensure stable energy access throughout the UK in the transition to clean energy.

A transformative decarbonisation agenda will require better coordination of transport and energy systems. This in turn will depend on universal and effective full fibre connection, underpinning ubiquitous 5G coverage.

"Smart" transport: Full fibre infrastructure will provide charging points for electric vehicles but the scale of transformation necessary for carbon reduction will require the dramatic reduction of private car travel through a new publicly-owned and digitally-mediated transport system. Through WeDecide and offline local assemblies, residents of different neighbourhoods and stakeholders from specific groups such as people with disabilities will design a new urban mobility plan to meet their needs. Transport for London, the most publicly owned and heavily planned transport economy in the UK is also by far the most successful. An integrated service covering entire cities would operate through a centralised app which includes dockless bikes or e-scooters and car-sharing schemes with charging bays on each street.

Additionally, 5G will enable the use of urban sensors which can help to facilitate the development of automated freight and logistics systems. [76] Through collaboration with trade unions, these integrated and efficient systems would be vital to a decarbonisation plan. In an international setting UPS, Amazon, and Uber have all began experimenting with these self-driving systems – it’s crucial that government anticipates and plans for the development of these technologies in order to prepare for the potential effects on workers. [77]

"Smart" energy grids will be an infrastructure of national strategic importance, central to ushering in a green industrial revolution. Publicly-owned fibre networks will underpin a clean, intelligent, mobile and distributed energy ecosystem based on democratised and decentralised ownership. The current power plant system was not built to accommodate the diversification in energy sources, especially not the rise in renewable resources, as electricity flowed only in one direction from power stations to end users. Large volumes of data, machine learning and AI will create the ability to successfully operate the smart grid infrastructure in order to optimise the system.

Research and Development: Beyond green infrastructure and sensor-based energy-saving technology, a Green New Deal requires research and development that can work towards advancements in green tech. Full fibre connectivity will significantly increase UK productivity, particularly in rural areas which are more frequently the subjects of outages and unreliable coverage. This has the potential to surge innovation, addressing local issues and building local solutions in response to the climate crisis. The use of "Internet of Things" technology for smart agriculture, as well as the need for reliable broadband speed required by telecommunications, cloud computing and streaming all point to the need for large-scale broadband upgrade. But this depends on adequate planning and universally distributed full fibre to help connect the entire UK and build a mission-oriented economy.

Digital skills remain a pressing concern in the UK. A 2018 survey found that 4.3 million adults had zero basic digital skills at all and 6.4 million adults had only have limited abilities online. [78] Age, gender and low income were the main predictors of poor digital skills. As part of a programme to develop better digital infrastructure, publicly-owned "maker labs" and co-working spaces therefore represent a significant opportunity for government in order to bridge the digital divide.

Freelance, precarious and gig economy work is also increasingly common in the global economy. Nearly 1 in 10 UK workers are employed in some capacity in the "gig economy", [79] and generally lack collective workplaces and opportunities for professional development and support. As autonomous and community-focused spaces, accessible, affordable maker labs and co-working spaces could offer exposure to a foundation in digital skills, such as database management and coding, as well as shared access to new technologies such as 3D printing and cutting edge software.

There is a pressing need to develop an ethical data management strategy, which recognises data sovereignty, privacy, encryption, and collective rights to data as fundamental rights. Such a strategy needs to involve both publicly available data collected by governments, as well as extend to regulatory frameworks for the internet service providers who move data through their networks. We also need to regard public data as a digital public asset - that is, a public good with a discrete value that need not be shared freely to enrich private companies, as is currently the case, for instance in ride-sharing apps’ use of Transport for London data. [80]

Only through clear, forward-looking government regulation can the right to self-determination of personal data use be maintained in the face of a rapidly changing tech landscape. New services - including platforms for integrated transport or participatory democracy - should be required to allow participants to establish the level of anonymity they would like, so that they cannot be identified without express consent. We should similarly not be afraid to introduce outright bans on certain technologies, such as facial recognition systems that generate limited or unproven social good and directly harm already-marginalised communities.

There is political consensus on the benefits of full fibre and the case for delivering it rapidly; indeed, in the UK’s December 2019 General Election, the delivery of nationwide high speed internet connectivity formed a key election pledge for several parties. The questions that remain are how, at what cost and who pays. A report from Frontier Economics for the National Infrastructure Commission analysed a set of different approaches for reaching 100% full fibre in the UK. Their analysis suggests that under current market conditions, FTTP connectivity would reach just 75% of the UK in 20 years time. The analysis does suggest it is possible to reach 100% coverage under conditions of "enhanced competition"; however, this would require significant government intervention, including subsidies and franchisement for areas which are uneconomic for private companies to reach, at a total cost of £32.3bn in deployment Capex.

By contrast, the analysis suggests a monopoly provider would deliver universal coverage faster and at a lower cost than enhanced competition market conditions, with nation-wide full fibre deployment achievable at an undiscounted deployment Capex of £20.3bn. The undiscounted deployment Opex for the two scenarios capable of reaching full coverage (National Monopoly and Enhanced Competition) are roughly equivalent, though slightly less under monopoly provision at £22.8bn compared with £23.7 with government-subsidised 'enhanced competition. The total costs for deployment and maintenance in this case are roughly equivalent to the projected Capex alone for "enhanced competition", with deployment Capex, connection costs and 30 years of discounted opex estimated at a total of £33.4bn. [81]

The obvious candidate for monopoly provision would be Openreach (in addition to the relevant parts of BT Technology), acting as a branch of BT. However, monopoly deployment is likely to be significantly less costly if under public ownership for a number of reasons. First, public ownership eliminates the need to pay costly dividends which undermine investment: BT Group paid £1.5bn in dividends in 2018-19 alone. Secondly, the cost of public borrowing is notably lower than for private companies.

The BT Group has four external-facing divisions: Openreach, which is the network division, Global Services, Consumer, and Enterprise. More than half of Openreach’s revenues come from charging other segments of the company, and so it generates only 9% of external revenues. However, it recorded about 25% of overall operating profits for the BT Group in FY2018-2019, and 30% the previous year, according to BT Group’s financial statements. BT technology is a smaller internal segment which creates and operates BT’s platforms, networks and IT systems across their range of services, and is engaged in designing new services for customers. Certain operations which are currently carried out by this division would be necessary to deploying and maintaining a publicly owned full fibre network, though not the majority. However, financial data pertaining to BT Technology is not available from BT Group’s financial statements and so is excluded from the analysis below. It should be noted that the associated costs would be modest when compared with the value of Openreach.

BT was required to finalise an internal separation of Openreach last year, including the transfer of 31,000 staff as employees specifically of Openreach. This made it easier to separate the network business as a separate private company; it also makes it significantly simpler to take the network segment alone into public ownership.

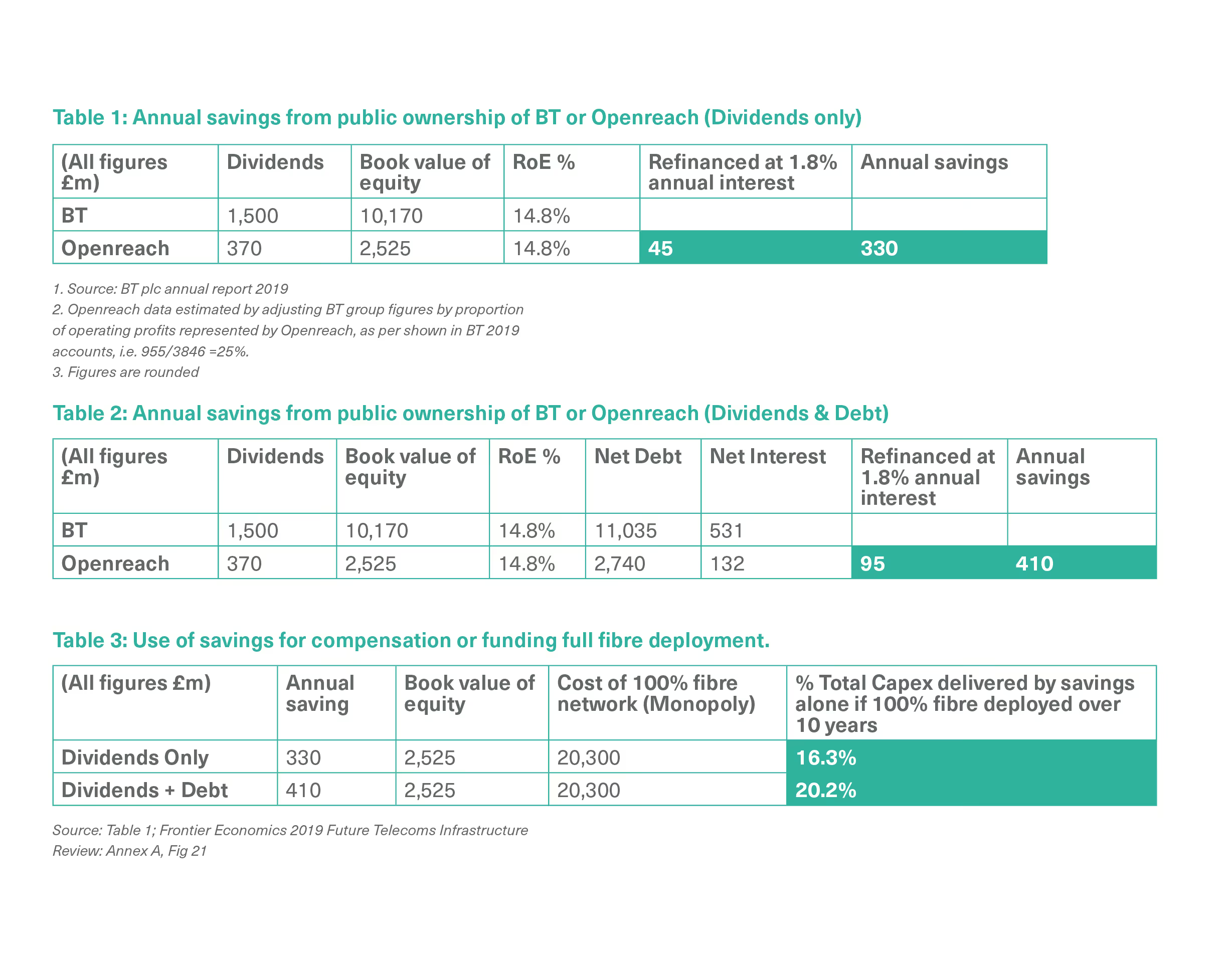

Our analysis suggests that taking Openreach into public ownership - eliminating dividend payments and refinancing at cheaper government bond yield - would provide savings of between £290 and £430 million per year, depending on the measure of profit used to assess Openreach’s contribution to the BT Group. Refinancing existing debt at 1.8% in addition to dividends could yield savings of between £360 and £540 million per year.

The analysis below considers Openreach as a fraction of operating profits. Table 1 shows BT’s financial results, highlighting the proportion attributable to Openreach, pro rata to Openreach’s contribution to the profitability of BT as a whole. This was measured using "operating profits" from BT’s 2019 Annual Report, which shows Openreach generating approximately 25% of group profits for the year. In line with other PSIRU 2019 estimates of public ownership savings, the table assumes government debt would cost 1.8%. This is likely a conservative estimate, as interest rates are currently very low.

The annual savings from eliminating dividend payments equate to approximately £330 million annually for the Openreach segment of the business, if compensation is based on book value of equity. If Openreach’s portion of BT Group’s net interest payments is also considered, the annual savings increase to £410 million per annum. These savings could be used to pay for investment in a 100% fibre network.

The Frontier Report suggests that after an "implementation period" to allow for the process of bringing Openreach into public ownership, the infrastructure deployment would take approximately 9-10 years. Thus, over a 10 year period the savings from nationalising Openreach would cover between 16% and 20% of the Capex cost of full fibre deployment.

There is also a possibility that compensation for shareholders could be based on market rather than book value of equity, which in the case of BT Group is currently higher than the book value. However, the choice of book or market value for compensation does not impact the absolute value of annual savings calculated above, which are determined by the elimination of dividends and potential refinancing of existing net debt; consequently, savings would still generate between 16% and 20% of deployment Capex costs over 10 years. It is worth noting that compensation based on market value can be highly variable due to fluctuations in share price as well as decisions such as the timeframe over which the market value is averaged to determine a price. The 1977 nationalisation of shipbuilding industries, for instance, saw ship builder Vosper Thornycroft receive just £5.3m in compensation based on market value in comparison with the £30m in net assets and cash held by the company. This was the result of basing compensation by market value on the average value over a defined period of several months, which spanned political ruptures like the 1973 oil crisis.

There are certain trade-offs identified between monopoly and enhanced competition approaches to deployment; for instance, the Frontier Economics report suggests a monopoly may have reduced incentive to innovate, while enhanced competition may still fail to deliver full coverage even with government subsidy and regulatory incentives. However, what is clear from the analysis is that a monopoly provider is the most cost-effective route to achieving universal coverage at the fastest pace; indeed, it may be the only way to deliver complete nation-wide full fibre due to the lack of incentive for private companies to service unprofitable areas.

There is a simple historical analogy to demonstrate why a monopoly provider is preferable for rolling out a critical infrastructural network efficiently, equitably and cost-effectively. If our road networks, rather than being planned and delivered by a single provider as a tax-funded public service, had instead been left to for-profit competition, the result would likely have been needless duplication, over-provision in profitable areas, poor rural connection, and the extensive extraction of rent over and above the cost of maintaining the road network. Similarly, without the costs of duplication and the need to distribute dividends to shareholders, a natural monopoly provider able to plan rationally is, as the government’s analysis suggests, likely to deliver nationwide full fibre cheaper and faster than other alternatives.

Another historical analogy can be found in previous waves of communication infrastructure roll out where the failure of private competition and the profit motive to deliver universal access on a reasonable timeline led to shifts in ownership. To build out a national telegraph industry, Gladstone nationalised the telegraph industry in 1870, while the Asquith administration took the telephone sector into public ownership to ensure universal connectivity was achieved.

To deliver a nation-wide, full fibre network under the lowest-cost, fastest pathway, Openreach and the specific elements of the BT Group related to rolling out the core network should be taken into democratic public ownership. The new public infrastructure company – operating at arms length from the government – should be given a mandate to roll out nation-wide full fibre by 2030, working in coordinating with the National Infrastructure Commission to deliver a 21st century digital infrastructure. This infrastructure should be open access.

Frontier Economics suggest the infrastructure deployment period for nationwide full fibre is just under a decade, with an assumed "implementation period" of between 3-5 years for establishing a legal framework for the new monopoly provider during with zero deployment would occur; 100% deployment would therefore achieved by 2033 at the latest. However, there are several reasons to suggest deployment could be completed significantly more quickly, in line with a 2030 target. First, Frontier acknowledge the assumption of zero deployment in this period is unlikely, noting “BT/Openreach could be expected to engage in some FTTP roll out,” during implementation, albeit at a reduced pace. [82] 5 years also represents a significantly longer implementation period than comparable models have exhibited in the past; for instance, the creation of a National Broadband Network (NBN) in Australia saw just a 2 year period in which no deployment occurred, and this was in part attributable to the need to establish NBN from scratch and negotiate with a major incumbent provider, in contrast with taking a fully operational company into public ownership. [83]

Financing the acquisition of Openreach and other minor components of BT Group operations related to rolling out the core network should occur through issuing government bonds to shareholders in exchange for the equivalent value of their shares in BT Group attributable to these elements, a majority of which will derive from Openreach. The compensation method of effectively swapping bonds for shares has various precedents in the United Kingdom, for instance in the nationalisation of the aircraft and shipbuilding industries in 1977. Importantly, from an accounting perspective, transferring ownership does not impact the UK’s public debt, because the bond issuance is matched by holding shares, or in this case a new company, of equivalent value, and the public acquires an income-generating asset. [84] Indeed, the critical issue at hand is not how assets are acquired, but how the new publicly owned entities operate, and whether public rather than private control will generate better outcomes.

To that end, based on the analysis of the National Infrastructure Commission and in coordination with Ofcom and the Treasury, the public infrastructure company should be mandated to deliver a level of annual investment to deliver a nationwide full fibre network by 2030. Funding for investment should come from charging ISP operators and service providers for access to the network, just as Openreach currently does. Rather than paying dividends, it should reinvest profits back into rolling out the network.

The annual savings from dividends alone could cover over 16% of the Capex required to deliver full fibre over 10 years. If debt is refinanced at 1.8%, the total savings could cover as much as 20%. To finance the remaining Capex requirements, the public infrastructure company should take advantage of near-record low-interest rates to borrow to invest in critical infrastructure.

New models of ownership should not replicate the mistakes of older forms of public ownership that were too often excessively centralised, top-down political and managerial; rather, the company should have core democratic principles underpinning its governance and operation. Instead, new models of democratic public ownership are needed that embed worker and wider social participation in decision-making that shape principles, values, and long-term strategic direction of the organisation. This should be based on a multi-stakeholder approach, with clear roles of different stakeholders including workers, users, residents, and other interested parties. This should also involve board representation, including from elected worker and community representatives. Finally, this system should incorporate principles of participatory planning, involving workers and wider communities to inform the goals, methods, and practices of the enterprise. [85]

To support the roll out of the network, a new sector deal for telecommunications should be agreed, including improving the "pipeline" of engineers and technicians required to deliver the network through training and support.

There are a number of successful, regional UK providers that have managed to roll out full fibre at a local scale, including KCOM and B4RN (Broadband for the Rural North). These companies could potentially be integrated into a national network provider, for instance operating as an autonomous local branch of the wider network. B4RN already operates as a community-led non-profit organisation. As assumed in the Frontier Economics analysis, other providers of FTTP infrastructure - notably Virgin Media - could remain free to continue providing and managing their own infrastructure. However, it is unlikely that Virgin Media would invest in extending their current FTTP footprint in the context of a national monopoly provider, and Frontier assume this extension would be undertaken by the monopoly provider. Over time, it may be appropriate to negotiate acquisition of such operations to maximise the benefits of strategic planning and lower the costs of borrowing for a public infrastructure company.

In taking part of BT into public ownership, the state should also take on a fair share of the BT Pension Scheme, which closed in 2018 (as part of the division of assets and liabilities). One approach would be, for example, to take on the fraction of the Pension Scheme representing all employees from Openreach and other relevant segments taken on by the monopoly providers. To place this acquisition in context, it is important to note that there is an existing Crown guarantee for the scheme, so the government is already the ultimate guarantor; and that there is an argument that compensation for acquiring the relevant parts of BT should reflect the fact that the pension deficit has accrued while under private ownership, with several billions of pounds paid out in dividends to shareholders while the Scheme has remained consistently underfunded.

Alongside the public monopoly-driven roll out of full fibre, Ofcom and DCMS should overhaul the regulatory standards of digital infrastructure providers, with stronger requirements around just access, affordability, and a rights-based approach to the development of digital infrastructures. Steps must also be taken to ensure that inequality of access is not replaced by inequality of use, and that communities are able to genuinely participate in shaping our digital future. Preliminary steps to achieve this could include:

With full fibre guaranteeing equal internet access, an online platform called WeDecide.gov.uk could function as an online space for everyone living in the UK (whether citizens, immigrants or asylum seekers; employed or unemployed) to debate and decide priorities for how digital infrastructures are used. These priorities could provide the basis for each local authority to develop a collectively determined plan for its digital future in order to tackle key social and environmental urban challenges. This could include smart energy grids, a digitally-enabled dockless bike system or sensor networks throughout the city for citizens to monitor noise and air pollution.

Once an area has co-created a plan for their digital future with the people who live there, there remains the question of who will run the services to be built on top of the fibre network. Alternatives to corporate platforms face particular challenges to get started so steps must be taken to democratise innovation, supporting the emergence of worker platform cooperatives, community initiatives and SMEs. In order to enable a new ecosystem of public and community-led service provision to grow new sources of financing must be made available, support and capacity-building through umbrella networks provided, and new ethical standards to public procurement procedures introduced to prioritise non-corporate contractors.

Local government should be mandated to provide co-working and maker spaces with 5G broadband infrastructure - either directly or in coordination with other stakeholders - for community business, co-operatives, and employee owned companies to ensure that these spaces can help these forms of enterprise thrive in the digital age.

The improved monitoring of and strategy for fibre roll out to ensure equity of access should be mirrored in considerations of the potential social and political harms of the technologies built on top of fibre networks, including invasive surveillance, social control and environmental damage.

The government should legislate to ensure that the networked data pertaining to individuals that is generated in the context of using public services cannot be owned by private service operators. Decentralised technologies (such as blockchain and cryptography) can be used in this context to give people greater control over the data they produce in their locations, which data they want to share, with whom, and on what basis, as demonstrated by the DECODE project in Barcelona and Amsterdam.

Rather than "tweaks" that seek to improve existing technologies by introducing new features or safeguards focussed primarily on privacy or bias, specific bans or highly stringent regulations could be introduced on technologies such as facial recognition which have particularly potential for use in highly oppressive, undemocratic ends. The same principle should apply to carbon-intensive technologies that cannot demonstrate any material contribution to social good.

Even after delivering fibre to every home, which guarantees equal access, it is likely that without strategic intervention, the digital divide would persist due to inequalities in use and adoption. This divide correlates strongly with class, racial and regional inequalities. A number of steps can be taken to address it. For instance, a network of "Fab Lab" innovation centres - digital fabrication and rapid prototyping workspaces - and "Digital Stewardship" training programmes in every community could be used to eliminate barriers to digital participation and provide the space, tools and resources for people to collaborate on projects to shape the digital future of their local area. Free workshops and "hack days" using people-guided popular education methods will bring tech education to communities that have difficulties accessing or which may have been harmed or disproportionately impacted by new technologies.

To ensure a full fibre future supports a net-zero economy, it is recommended that the installation and development of broadband and 5G infrastructure is planned strategically to enable the support of a just transition away from fossil fuels. The Committee on Climate Change should advise the National Infrastructure Commission on the digital infrastructure roll out the UK needs to reach net-zero rapidly and justly.

The way we organise our digital infrastructure is fundamental in shaping distributions of wealth, power, and capability in contemporary society. The status quo, market-driven methods for deploying full fibre technologies have proven incapable of delivering equality of access and use for all, while new technologies - left unchecked - risk amplifying existing inequalities and forms of social harm and injustice. But a new ecology of democratic ownership and governance of the UK’s digital, data and knowledge infrastructures can lay the foundations for a wealth of shared benefits. With a publicly owned, nation-wide full fibre network - delivered at a lower total cost and more rapidly than the alternatives - anchoring the UK’s digital infrastructure, new horizons emerge: the decommodification of connectivity through a public option ISP; the enshrining of Internet access as a 21st century human right; infrastructure capable of supporting a decarbonised economy; and strategies to ensure we all share the benefits of a digital future.

[#fn1][1][#fn1] Cambridge Wireless, "Full Fibre by 2025: A Bold Vision or a Failure to Grasp Reality?", 2019.

[#fn2][2][#fn2] Duckworth, Martin, “Tomorrow’s Telecoms Networks”, Frontier Economics, January 2018.

[#fn3][3][#fn3] bbc.co.uk, accessed December 2019, “UK reaches 10% full fibre milestone”, BBC News, 11 November 2019.

[#fn4][4][#fn4] Clement, J, “Percentage of fibre connections in total broadband among OECD countries reporting fibre subscribers as of December 2018”, statista, edited September 2019.

[#fn5][5][#fn5] Alston & van Veen, "How Britain's welfare state has been taken over by shadowy tech consultants”, The Guardian, 27 June 2019.

[#fn7][7][#fn7] Zuboff S, The Age of Surveillance Capitalism: The Fight for a Human Future at the New Frontier of Power, London: Profile Books, 2019.

[#fn8][8][#fn8] Centre for Economics and Business Research (CEBR), “Full fibre broadband: A platform for growth. A CEBR report for Openreach”, Openreach, October 2019.

[#fn9][9][#fn9] Latour, B, “Some advantages of the notion of “Critical Zone” for Geopolitics”, Science Direct, 2014.

[#fn10][10][#fn10] gov.uk, accessed December 2019, “Structure of UK telecommunications sector: an introduction”, Cabinet Office, 8 February 2011.

[#fn11][11][#fn11] Bowker, G (2014).; The Infrastructural Imagination’, In A. Mongili & G. Pellegrino (Eds.), Information Infrastructure(s): Boundaries, Ecologies, Multiplicity, Cambridge Scholars Publishing.

[#fn12][12][#fn12] googleblog.blogspot.com, accessed December 2019, “Think big with a gig: Our experimental fiber network”, Googleblog, February 2010.

[#fn13][13][#fn13] Durkin, E, “Amazon HQ2: tech giant splits new home across New York City and Virginia”, The Guardian, 13 November 2018.