Yesterday, the New York State Energy Research and Development Authority (NYSERDA) — a state agency principal to implementing the state’s renewable generation programmes — announced increased state guaranteed strike prices for two offshore wind development contracts, Empire Wind 1 and Sunrise Wind, by 27 per cent and 36 per cent respectively. This move has doubled the cost of each project for New York consumers, felt in their monthly bills.[1] Meanwhile, the re-run reverse auction for contracts did not plug the investment gap left by the withdrawal of developers from their previous contracts.

In global context, private investment in renewable generation, especially in liberalised wholesale markets such as New York’s, depends fundamentally on state subsidy or other derisking such as ex ante fixed “strike price” tools to inoculate against wholesale market volatility and high-upfront capital costs that hinder the profitability of renewables.[2] Offshore wind in particular is capital intensive and reliant on such tools to induce private investment. Yesterday’s announcement should be viewed as a negotiation between state and private capital on the terms of the latter’s green investment, as such derisking tools proved inflexible and vulnerable to other forms of volatility external to the wholesale power market. And a negotiation that should be sidestepped entirely by eschewing private control of investment and embracing public direct investment and public enterprise.

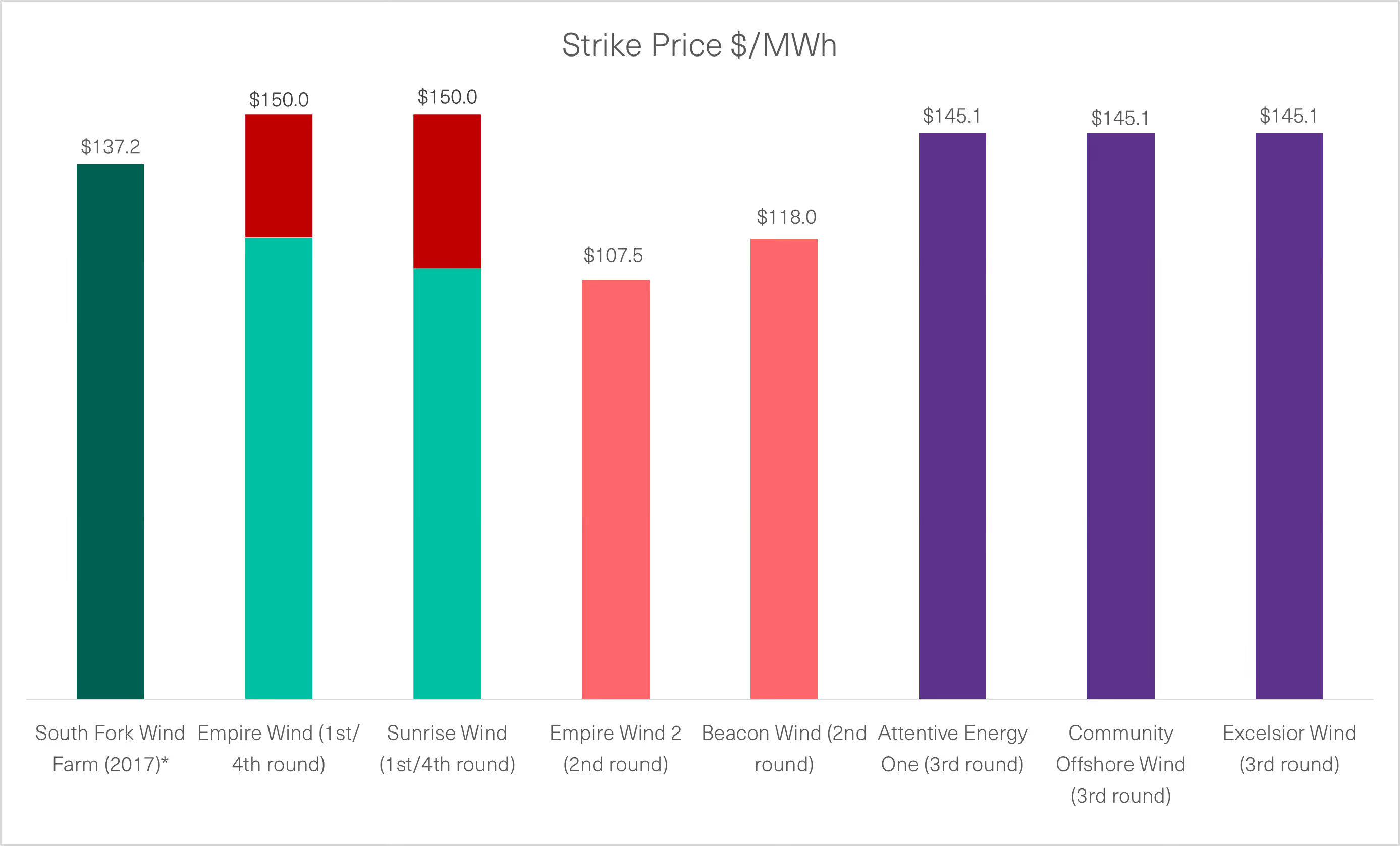

In the face of inflation and rising interest rates — to which renewables are particularly sensitive — developers of four state-guaranteed contracts to build large-scale offshore wind farms had clamoured for a 41 per cent increase in their contracted strike price — the structure of this de-risking programme is discussed further below.[3] The New York’s Public Service Commission, which regulates utilities and sets consumer electricity price controls, rejected this request in October of 2023 due to the increased costs consumers would have incurred.[4] Later in the fall, NYSERDA announced three new offshore wind farm development contracts at a 28 per cent increase in the strike price compared to these four developers seeking adjustments to their contracts and announced that it would re-run procurement auctions for these projects, open to new bidders, but universally taken to be an opportunity to allow existing contract holders to seek an increase in strike price.[5] One project, Beacon Wind saw its developer BPs pull out of their existing contract.[6] And another project, Community Offshore Wind 2 project, has been “waitlisted” and may be awarded in the future.

[.img-caption][.img-caption-header]Figure 1 Strike Price ($/MWh)[.img-caption-header][.img-caption]

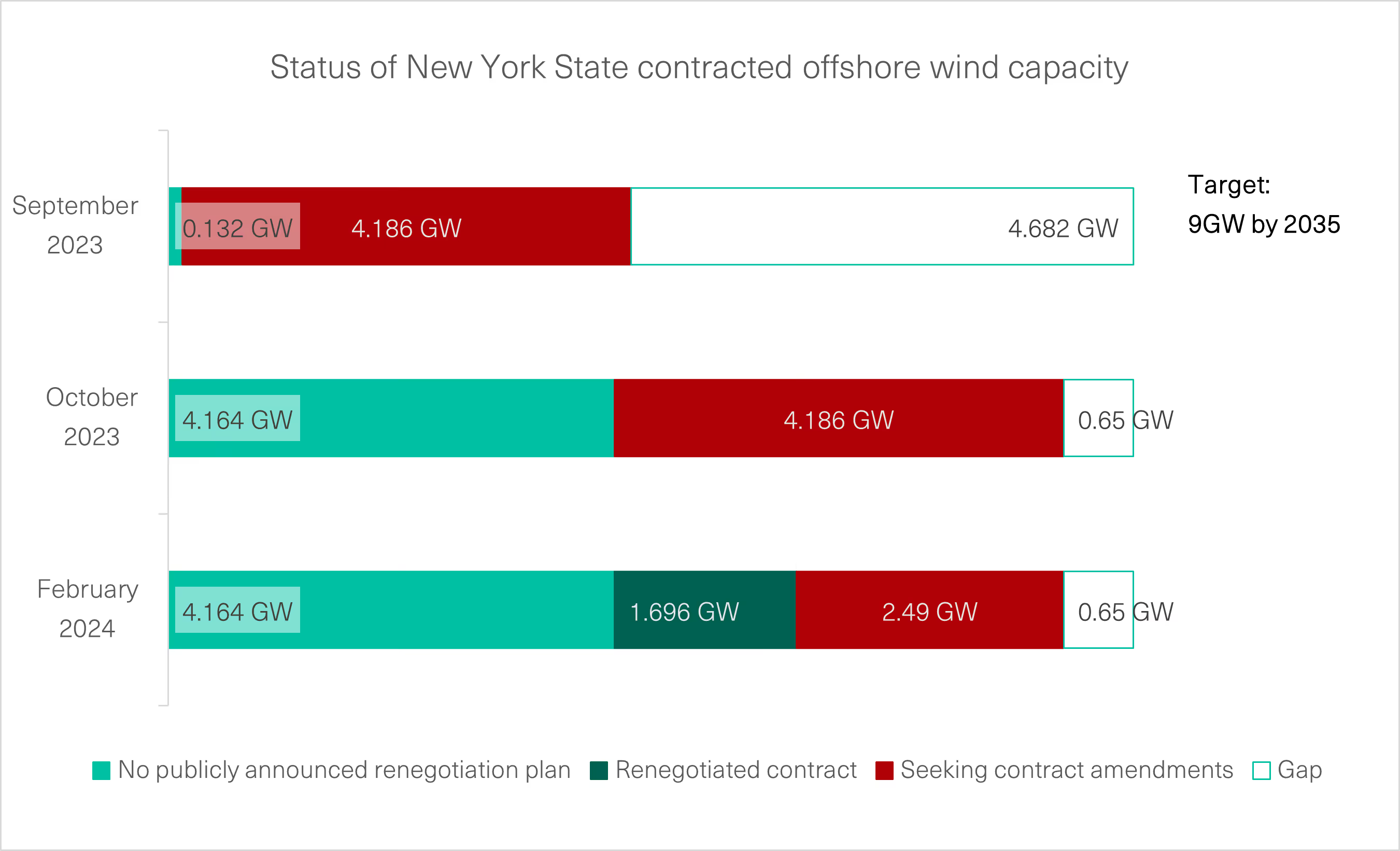

In a global context where new offshore wind procurement auctions using similar de-risking have failed and existing contracts have been abandoned by for-profit developers — discussed further below — there has been a risk of green capital strike ahead of this re-run auction: these four projects account for 47 per cent of the state’s target of reaching nine GW by 2035.

[.img-caption][.img-caption-header]Figure 2 Status of New York State Contracted Offshore Wind Capacity[.img-caption-header][.img-caption]

New analysis by Common Wealth on these for-profit developers has found that of the ten companies with successful bids to develop New York offshore wind, three are private equity backed (Vineyard Offshore, Corio Generation and Rise Light & Power) and the remainder are publicly listed. While Orsted and Equinor are listed on their respective stock markets, the state has a controlling stake in their business — the Danish government has a 50.1 per cent stake in Orsted, and the Norwegian government has a 67 per cent stake in Equinor.

Private equity backed ventures entered the New York offshore wind market in the 3 auction round, securing the highest strike price offered by the state. The private equity business model rose to prominence through leverage buyouts, where firms would acquire existing companies, leverage debt for dividend recapitalisations and strip assets to generate greater returns for their investment partners. In the case of offshore wind, private equity firms use their easy access to capital to provide the initial investment in renewable infrastructure, but this is only made possible by the state guaranteeing a large enough fixed revenue for 10-15 years through a fixed strike price. This much is made clear by Copenhagen Infrastructure Partners, the private equity firm behind the Excelsior Wind farm, who state that they seek to invest in “long-term contracted energy infrastructure with the objective of generating attractive risk-adjusted returns and long-term, stable, and predictable cash flows with low correlation to the business cycle”. The issue with the reliance on private equity is the same as with publicly listed for-profit companies that are investing in offshore wind: if the price is wrong, then they will not bite.

Further, for-profit companies, whether backed by private equity, state owned or publicly listed, seek to extract profit from their business to pay their owners and investors. In the case of New York offshore wind, increased strike prices will ultimately be borne by New York households and businesses. For example, when the developers Orsted, Eversource, BP and Equinor petitioned the state to raise their original strike price, the state calculated in their response that the impact of granting the adjusted strike price would raise monthly household bills by an estimated 2.5-6.7 per cent (approximately an additional $6.28), for heavy industry their bills would increase anywhere from 5.6 per cent to 10.5 per cent. In this case, the developers’ rate of return is locked in and paid for by end consumers and will have an inflationary effect across New York state’s economy.

Since 1996, New York State’s power sector has been organised around a liberalised wholesale market, meaning ownership of generation is divorced from ownership of transmission and distribution infrastructure and a fragmented set of generators compete to sell their power in the market. A set of public institutions shape the sector and this market: the New York Public Service Commission regulates market actors, setting maximum consumer electricity prices and other regulations; the New York Independent System Operator — a nongovernmental, nonprofit company — coordinates the wholesale electricity market; and the New York State Energy Research and Development Authority — a government-controlled public benefit corporation —administers renewable energy and energy efficiency programming in the state, including state level subsidies. Yet, critically, the majority of electricity generation in the state is privately owned and operated for-profit.

This ownership structure and the reliance on private investment pose structural limits to meeting New York State’s power sector decarbonisation targets. In 2019, the New York State legislature passed the Climate Leadership and Community Protection Act (CLCPA), which mandates that electricity used in the state be 70 per cent by renewable generation by 2030 and that nine gigawatts of offshore wind power be built to service the state by 2035. Meanwhile, (clean) electricity demand will rapidly rise across the next two decades as a result of intense electrification of transportation, industry and buildings necessary for whole of economy decarbonisation, meaning these goals are not the final renewable target for the coming decades. Separately, the Biden Administration has set a federal target for deploying 30 GW of offshore wind by 2030. A 2023 report found that the state’s current electricity mix is only 30 per cent renewables, of which the majority is from legacy hydropower owned by the public through the New York Power Authority.[7] This same report anticipates New York will fall far short of these goals through a status quo approach to renewables deployment largely relying on private investment, following a relatively optimistic modeling of investment by private generators based on recent pace of private investment across renewable technologies.[8]

Private investment in renewable generation capacity structurally relies on the state. Renewables owned and operated for profit — across all technology profiles — struggle in wholesale markets like New York’s as they are highly capital intensive (especially compared to existing fossil fuel generation) and structurally vulnerable to the wholesale market’s inherent volatility and the more specific “revenue cannibalisation effect” that renewables face, whereby periods of high output and low demand produce very low marginal prices for variable renewable electricity, causing extremely low or negative market prices that pose debt servicing and solvency issues.[9] To overcome this sensitivity to capital costs, merchant price risk and revenue cannibalisation effects, investment in for-profit utility scale renewable generation in global context structurally relies on state subsidisation tools that provide a guaranteed fixed price or otherwise employ public funds to furnish stable profitability.[10] In the context of offshore wind specifically, New York state follows a similar model to derisking private investment in the sector in global context: NYSERDA runs reverse auctions for bids to build offshore wind farms for pre-agreed fixed electricity price that is state guaranteed but funded by consumer electricity bills — a form of indirect public procurement funded by a captured public through their bills.[11]

Today’s announcement should be understood as a negotiation between state and capital on this terrain: so long as the state abstains from direct investment itself, it is reliant upon inducing private investment by meeting the profitability demands of private investors who in turn are unable to invest in renewables without heavy state intervention. The occasion of this negotiation between state and capital makes clear why such abstention by the state is untenable.

In global context, private investment in renewable generation across all technology profiles did increase across the past two decades, thanks largely to state derisking and subsidization.[12] However, this investment regime has proven insufficient for delivering necessary generation capacity in line with targets.[13] And, as economic conditions structurally shift away from the previous era of low inflation and zero interest rates — which again did not see sufficient investment in renewables to meet power sector decarbonization targets — profitability is under threat.[14] This is despite the generous investment tax credits offered by the federal Inflation Reduction Act in the US context, which subsidize upfront investment costs.[15] As Politico reported at the end of 2023, in New York State alone, “about 60 per cent of the onshore renewables projects awarded contracts to support New York’s climate goals have cancelled their agreements with the New York State Energy Research and Development Authority.[16] This is because ex ante fixed price tools meant to support private investment in turn are inflexible to changing economic conditions.

For-profit investment in offshore wind — which is highly capital intensive — in particular has seen a battering in global context. In 2023, the North American branch of Iberdrola cancelled two offshore wind power purchase agreements (PPAs) signed with Massachusetts and Connecticut in July and October.[17] Similarly, Ørsted abandoned two utility-scale projects off the coast of New Jersey in early November.[18] Subsequently, as mentioned above, energy giants BP and Equinor terminated one of the three PPAs jointly signed with the State of New York in the early part of the new year.

As Common Wealth has analysed at length, the UK is falling far short of its ambitious offshore wind expansion goals and recent failures have further imperilled them. In July, citing supply chain pressures and rising equipment costs, the Swedish state-owned enterprise Vattenfall abandoned the Norfolk Boreas project planned for the UK Continental Shelf.[19] Subsequently, in September 2023, the UK Government's fifth Contracts-for-Difference (CfD) auction round (AR5) for renewable power development failed to receive any bids for contracts to supply new offshore wind power capacity.[20] Developers had communicated to the industry press, UK media, and the government that the maximum electric power contract prices were set too low to ensure adequate profits and justify investments in new capacity. Following this failure, the government raised the subsidised administrative strike price that sets the starting point for next year’s CfD allocation round by 66 per cent which will be paid for by consumer bills.[21]

As Common Wealth has discussed elsewhere, reliance on ex ante fixed price mechanisms to derisk private investment in offshore wind has backfired. Procurement auction failures and contract abandonment or negotiation in global context are occurring not just because of rising costs of capital and supply chain uncertainty, but because of the systemic use of ex-ante fixed prices to derisk investment and the wider structural reliance on private investment. These cannot be easily solved by higher subsidies for clean energy projects. Leaving aside the well-known issue of private developers’ higher cost of capital and focusing on the robustness of delivery, there are three big tensions which public direct investment would alleviate or bypass.

First, it is difficult to respond flexibly to external shocks when relying on private profit-seeking investors whose fixed capital investment decisions are dependent on assurances given long before operation of assets. An approach which sets electricity prices based on average actual costs ex post would allow for greater resilience of investment, especially during periods of turbulence, which climate destabilisation and geopolitical volatility are likely to bring. Although there are subsidy tools that can move away from ex ante fixed price derisking, public direct investment would be best equipped to engage in capital intensive investment then later pricing electricity on average real costs.

Second, there is a continuing tension between maintaining profitability of both private generation and private production in the supply chain while pushing for the lowest possible consumer costs of generation through contract auction models, leaving the sector vulnerable to shocks down the chain. The fragmented allocation process has instead foisted risk onto the wind turbine manufacturers who, from a strategic perspective, are most in need of guarantees from the state.

Third, auction failures and contract abandonment points to the more fundamental issue with relying on private investment — it is subject to subjective hurdle rates, or expected rates of return, to meet generation capacity targets. We do not know if various strike prices would have actually been loss-making — only that it they were not deemed profitable enough for investors, with profitability defined by internally set hurdle rates and relative to other market and investment activities.

New York Stands at the precipice of a paradigm shift, away from reliance on private investment to embracing public power. In May of 2023, New York state passed the Build Public Renewables Act, which legally empowers the New York Power Authority (NYPA) to build and own renewable energy infrastructure across all technology profiles and carries an implicit mandate for the NYPA to literally plug the renewable investment gap vis-à-vis annual sub-targets of the state’s legally enshrined 70 per cent renewables by 2030 mandate. This bill’s passage is both a result of powerful organising campaigns and of the Inflation Reduction Act’s “elective pay” tax credits, which for the first time will enable non-profit developers to claim federal renewables subsidy. Public enterprises, such as NYPA, face no mandate to pay dividends and benefit from structurally lower cost of capital — a cost to which renewables projects in particular are acutely sensitive — and do not stipulate subjective hurdle rates in excess even of these costs as a condition for going ahead with socially needed investments. A publicly-owned energy developer like NYPA would be able to more rapidly and decisively invest in renewable generation while delivering lower costs at both project and system wide levels. Yet, NYPA’s ability to lead in delivering on this mandate will depend upon further political efforts to build capacity and capitalisation for the institution to directly invest and own in renewable generation at scale.

Moreover, offshore wind may require further intervention and policy development, especially to move beyond the state’s initial 2035 target to support deep economy-wide decarbonisation. The Build Public Renewables Act allows for NYPA to invest in and operate renewable generation across technology profiles, including offshore wind. More recently, during public comment, NYPA’s CEO Justin Driscoll said NYPA would consider stepping in to redevelop failed project in the state, without ruling out any particular technology profile. Yet, as a 2021 study which modelled the feasibility and benefits of NYPA undertaking the majority of onshore utility scale solar and wind noted, due to its capital intensity and other risks, without an increase in capitalisation, NYPA should consider moving into offshore wind farther along the state’s renewable energy investment sprint.

Yet, as public intervention in the offshore wind sector increases, such a capitalisation increase for NYPA should be on the table. And even absent NYPA direct investment, options for public development should be on the table at the state, regional, and federal levels. In the coming months, we will consider such potential public pathways for offshore wind, from public equity stakes in the near term, to the development of a federal offshore wind developer to support the US’s offshore wind goals.

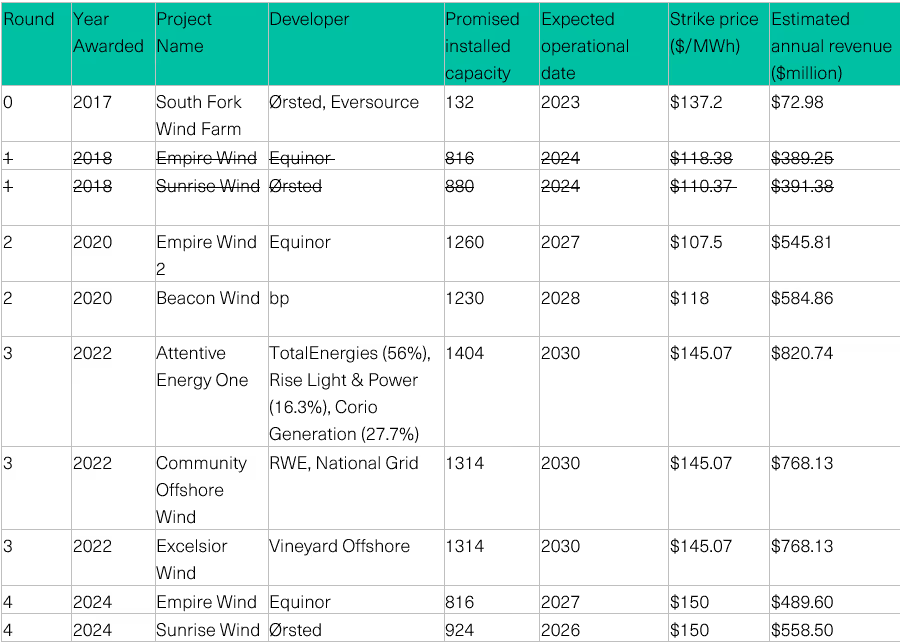

Eight licences have been awarded across three licencing rounds (excluding the South Fork Wind Farm) in 2018, 2020 and 2022. NYSERDA announced the results of its fourth round in early February 2024, which included renegotiations of previously awarded contracts.

[.img-caption][.img-caption-header]Table 1[.img-caption-header][.img-caption-text]*NB: stakes are split 50-50 unless explicitly mentioned. Estimated revenue calculated by MW capacity*capacity factor of 46%*hours in a year. The source for the capacity factor is found here.[.img-caption-text][.img-caption]

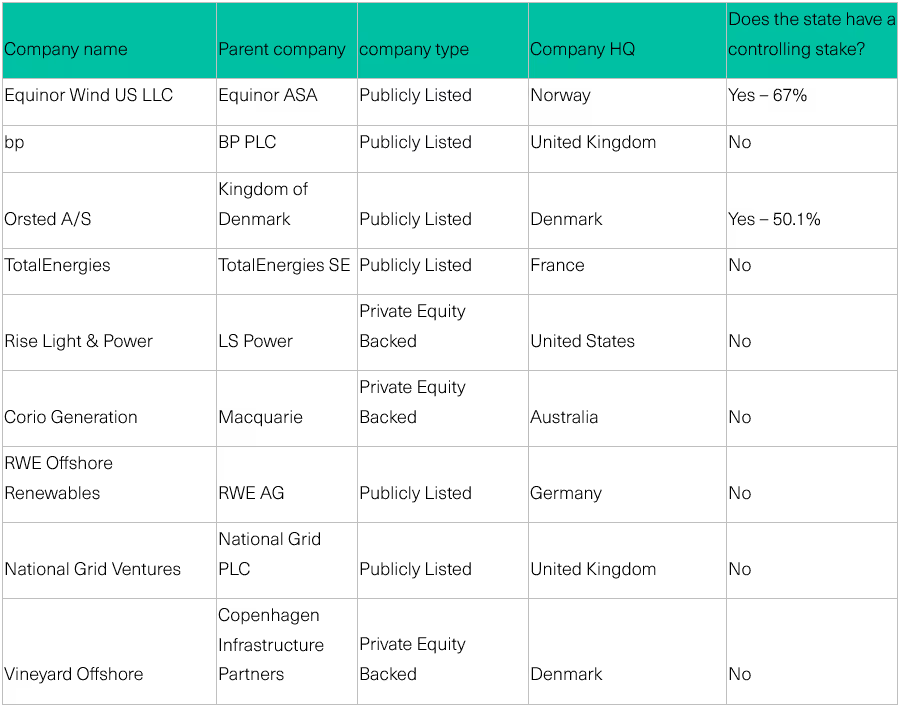

Of the ten companies with successful bids to develop New York offshore wind, three are private equity backed (Vineyard Offshore, Corio Generation and Rise Light & Power) and the remainder are publicly listed. Private equity companies are new entrants to New York’s offshore wind auctions, only winning bids in the 2022 auction round, which has noticeably higher strike prices than previous rounds. While Orsted and Equinor are listed on their respective stock markets, the state has a controlling stake in their business — the Danish government has a 50.1 per cent stake in Orsted, and the Norwegian government has a 67 per cent stake in Equinor.

This mix of publicly listed oil majors and private equity backed firms in offshore wind is not unique to New York. There has been an upswing in interest in offshore wind globally due to higher capacity factors than onshore wind farms and decreasing installation costs (prior to the current surge in initial capital investment).

Here is a summary table for the companies with offshore wind development licences:

[.img-caption]Table 2[.img-caption]

[1] Marie French, “Offshore wind costs double for consumers as New York keeps early projects on track”, Politico, 29/2/2024. Available here.

[2] Brett Christophers “Taking Renewables to Market: Prospects for the After-Subsidy Energy Transition”, Antipode, 2022, 1519-1544.

[3] Matthew Zeitlin, “New York’s Offshore Wind Future Is Being Dragged Down By Its Past,” Heatmap, 27/10/2023. Available here.

[4] Matthew Zeitlin, “New York Rejects Plan to Rescue Sinking Offshore Wind Projects,” Heatmap, 12/10/2023. Available here.

[5] Zeitlin, “New York’s Offshore Wind Future Is Being Dragged Down By Its Past,” Heatmap, 27/10/2023.

[6] "Equinor, BP Cancel Contract to Sell Offshore Wind Power to New York”, Reuters, 3/1/2024. Available here.

[7] "Mind the Gap: An Estimation of the Renewable Energy Needed to Meet New York’s Clean Energy Mandates”, Strategen, 2023. Available here.

[8] Ibid.

[9] Christophers “Taking Renewables to Market: Prospects for the After-Subsidy Energy Transition”, Antipode, 2022.

[10] Ibid.

[11] Beiter, Philipp, Jenny Heeter, Paul Spitsen, David Riley, ”Comparing Offshore Wind Energy Procurement and Project Revenue Sources Across U.S. States”, National Renewable Energy Laboratory, 2020. Available here.

[12] Christophers “Taking Renewables to Market: Prospects for the After-Subsidy Energy Transition”, Antipode, 2022.

[13] Ibid.

[14] Lars Paulsson, Will Wade, and Jennifer A Dlouhy, ”Why Offshore Wind Is Stumbling and What Can be Done”, Bloomberg, 16/9/2023.

[15] Tracy Alloway, Joe Weisenthal, and Aashna Shah, ” Challenges Are Piling Up in the US Offshore Wind Industry”, Bloomberg, 22/9/2023. Available here.

[16] Marie French, ” More developers cancel contracts for New York renewable projects”, Politico Pro, 22/12/2023. Available here.

[17] Maz Plechinger, ”Iberdrola cancels another offshore wind farm project”, Energy Watch, 3/10/2023. Available here.

[18] Diana DiGangi, ”Ørsted cancels two offshore wind projects along New Jersey coast,“ Utility Dive, 1/9/2023. Available here.

[19 "Vattenfall says it is stopping British Norfolk Boreas offshore wind farm”, Reuters, 20/7/2023. Available here.

[20] Offshore Staff, ”Investors shun UK offshore wind auction,” Offshore,8/9/2023. Available here.

[21] Chris Hayes and Melanie Brusseler, ”For-profit schemes can’t drive the transition to net zero”, New Statesman, 21/9/2023. Available here.