Securing safe, affordable, reliable bus services, as well as restoring vibrant local economies and thriving high streets, will require reshaping the ownership and operation of bus networks.

Covid-19 triggered dramatic changes to the UK’s transport sector. The suspension of the UK rail franchise system last September exposed an illogical and unspoken arrangement, whereby private companies are substantially subsidised to profit during normal times, while their losses are guaranteed in times of crisis. In February, the Welsh Government took the Wales and Borders rail franchise into public ownership, and rail services in Scotland are set to be nationalised as of March 2022. Yet alongside seismic transformations in the rail sector, there has been a recent surge in appetite to transform regional and local bus services, as demonstrated in places like Greater Manchester.

Decades of bus privatisation and deregulation combined with years of austerity has resulted in increasing fares, unreliable services, and poor pay and conditions for many bus workers. The pandemic exacerbated this: London bus drivers, for example, had a two-fold excess in mortality in the first wave of the epidemic.

The model of a heavily deregulated and privatised bus network disproportionately impacts people that are marginalised by the current economic system. Lower paid people that live in deprived areas tend to be more dependent on bus networks, as well as being more likely to turn down jobs due to transport-related concerns. And, as the Women’s Budget Group notes, “poor quality, unreliable and expensive public transport has a far bigger impact” on the lives of women than it does on the lives of men.

Yet while communities struggle with inadequate bus service provision, private bus firms and their shareholders have reaped substantial profits. Private bus service operators Arriva, FirstGroup, Go-Ahead, National Express and Stagecoach paid out an average of almost £150 million a year to shareholders between 2008 and 2018. What’s more, our analysis reveals that share ownership of bus companies is dominated by a combination of high net worth individuals, large banks, major asset management companies, and firms owned by foreign governments. As a result, rising bus fares drive a significant transfer of income from ordinary bus service users - often those with no choice but to travel by bus - to wealthy individuals, investors, and governments.

The Transport Act of 1985 dramatically changed the landscape of bus ownership throughout Britain, paving the way of large-scale deregulation and privatisation of buses, making provisions to transfer the operations of the National Bus Company to the private sector. Today, the vast majority of bus services are now privatised. At the same time, they face little competition: only 1% of bus services face head-to-head competition, which a 2011 Competition Commission report has shown has led to lower quality services and higher fares.

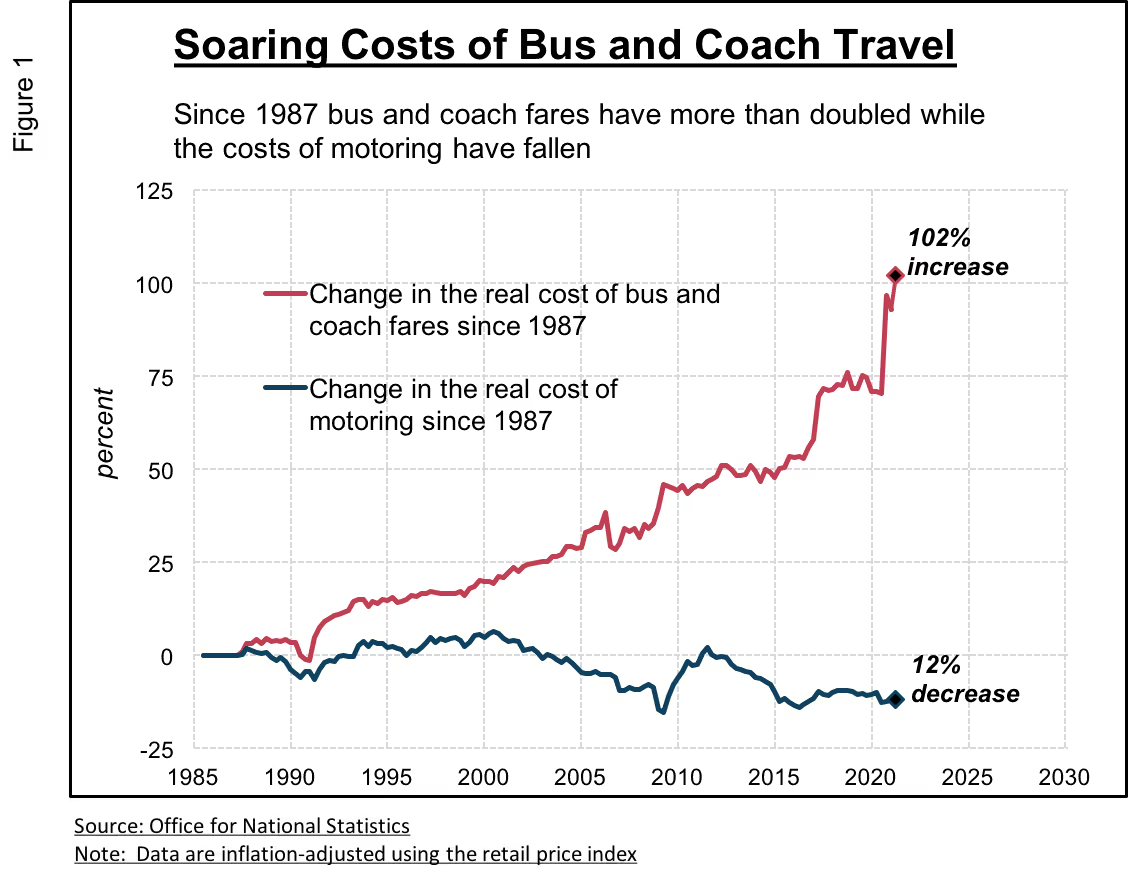

The privatised bus network has created multiple, compounding problems. Figure 1 shows data on the costs of motoring versus the cost of taking the bus or coach in the UK from 1987. By comparing these data, we can see how a policy regime of promoting automobiles and privatising public transport since the 1980s has led to a massive divergence in the costs of different modes of travel. While the real cost of taking the bus and coach have doubled since 1987, the real cost of driving one’s own private automobile has fallen by 12 percent.

These dramatic changes in the cost of car versus bus and coach transport hinder efforts to tackle the climate emergency. According to a Department for Transport (DfT) report, cars and taxis are responsible for 55 percent of greenhouse gas emissions (GHG) related to domestic transport, while buses and coaches account for only 3 percent. Estimates suggest that a local bus journey is responsible for just over half of the GHG emissions of a single occupancy car journey. Increases in the relative cost of bus and coach transport also have highly regressive distributional effects. Data from the Office for National Statistics (ONS) reveal that 93 percent of the richest 10 percent of UK households (ranked by gross income) own a car or van, while only 35 percent of the poorest 10 percent of UK households own a car or van.

Figure 2 shows changes in the inflation-adjusted cost of local bus fares since 1995 on a regional basis. Local bus fares have increased across the UK, but the rate of change is uneven. At 63 percent, English metropolitan areas outside of London - Tyne & Wear, Merseyside, Greater Manchester, West Midlands, South Yorkshire and West Yorkshire - have suffered from the sharpest increase in local bus fares. Throughout England, Scotland and Wales, London has witnessed the lowest increase in local bus fares at 23 percent; and in fact, local bus fares in the capital have fallen steadily since 2016 under Mayor Sadiq Khan. Falling bus travel costs in London – due largely to fare freezes and passenger-friendly ‘hopper’ fares – illustrate how public policy can play a crucial role in improving the accessibility of public transport. All that is needed is the political will to enact such policies.

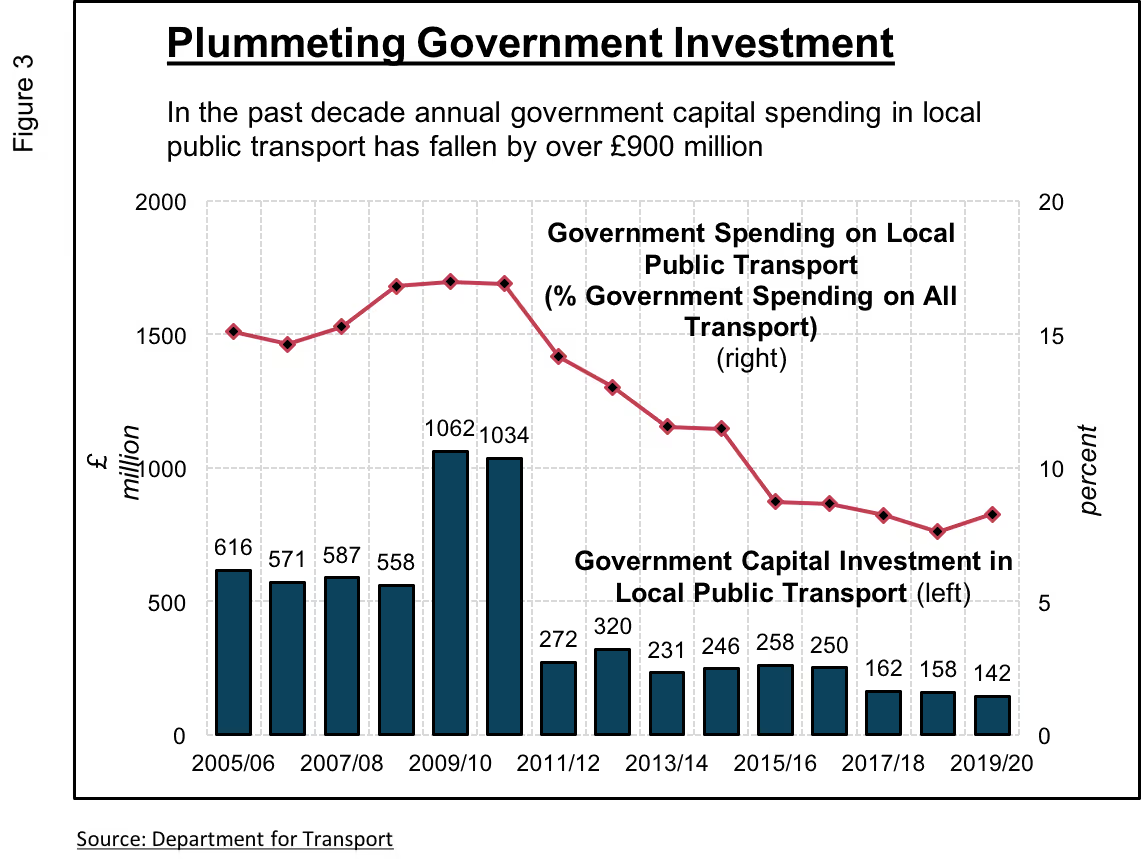

Figure 3 focuses on government investment in local public transport from 2005 to 2020. It is worth noting that 99% of the funding displayed in this figure comes from local governments. The bars at the bottom of the chart show the overall amounts of government capital investment in local public transport (in millions of GBP), while the line above the bars shows the share of government spending on local transport as a percentage of government spending on all transport (e.g. motorway maintenance and expansion, railway services, etc.).

What we see is that dramatic reductions in capital investment and spending on local public transport coincide with the austerity regime that was introduced by the Conservative and Liberal Democrat coalition Government starting in 2010. In short, the increased cost of bus travel and the severe cuts to government spending on public transport go hand in hand.

To this point we have focused on bus service users and governments, but what about bus companies? Which companies are the major players? How are they structured and who are their major shareholders?

Figure 4 shows the largest bus operating groups and their key owners. It includes the ‘Big Five’ UK-headquartered companies that dominate local bus provision - FirstGroup, Go-Ahead Group, Stagecoach Group, Arriva and National Express - along with three large foreign companies that operate in the UK - RATP Group, Transdev and Abellio. For the big five we see that they are principally owned by a combination of high net worth individuals, large banks and asset management companies. For the foreign companies, we see that foreign governments dominate the ownership network. RATP Group is 100% owned by the French Government, Abellio is 100% owned by the Dutch Government, and Transdev is 66% owned by Caisse des Dépôts, a public financial institution wholly owned by the French Government.

[.fig]Figure 4: Major Owners of the Largest Bus Operators in the UK[.fig]

Bus companies might seem like fairly straightforward entities: traditional ‘brick and mortar’ businesses offering simple, if vital, transportation services. Yet once we peer into the organisation of these companies, we see that they are incredibly complex. Some of the big five UK bus operators have hundreds of subsidiaries, spanning many different countries and operating in various sectors, both financial and non-financial. Figure 5 shows the major bus subsidiaries of the largest bus operating groups. Given the enormous complexity of these companies, we have imposed a threshold for inclusion in this figure: any bus subsidiary with revenues in excess of £50 million is included, all others are excluded. This leaves 27 major bus subsidiaries overall. We can see that the largest operators have a commanding presence throughout the UK.

[.fig]Figure 5: Revenues of the Subsidiaries of the Largest Bus Operators in the UK[.fig]

What kinds of business strategies do the bus companies employ? One of the central features of ‘financialised’ capitalism over the past few decades has been a corporate governance model anchored in principles of shareholder value maximisation. This model often involves downsizing operations and reducing productive capacity, and distributing profits to shareholders in the form of dividends and stock buybacks.

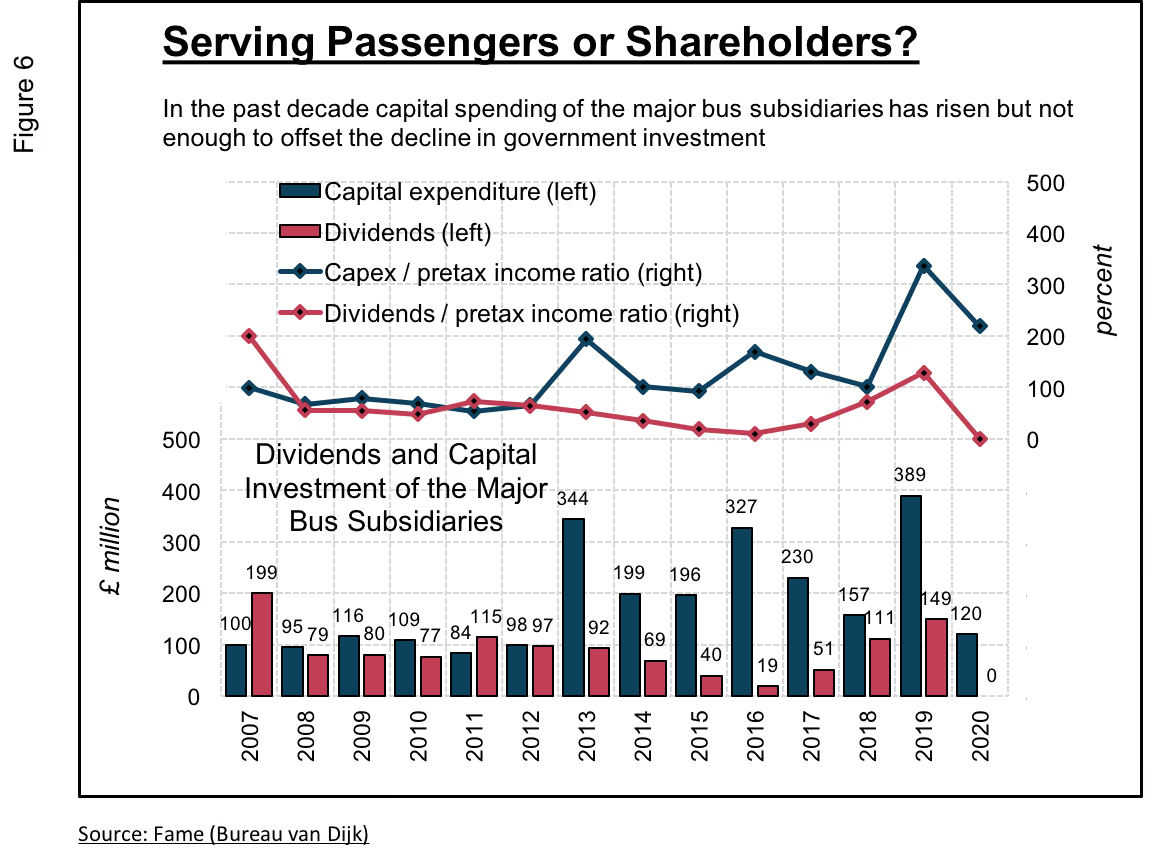

Figure 6 gauges the major bus companies’ commitment to shareholder value, showing their capital expenditures and their dividend payments to shareholders. Capital expenditures can be regarded as an inverse proxy for downsizing: the higher they are, the less a company can be said to be engaged in downsizing, and vice versa. Dividend payments are a proxy for the extent to which companies are distributing value to shareholders. The bars in the bottom part of the figure show the total amounts the bus companies dedicate to capital expenditures and dividends (in millions of GBP). The two lines above the bars show capital expenditures and dividends of the bus companies as a percentage of their pre-tax income.

[.fig]Figure 6: Servings Passengers or Shareholders?[.fig]

A noteworthy aspect in the figure is the increase in capital expenditures from 2013 onwards. This increase in investment suggests that the bus companies are bucking the trend of downsizing associated with shareholder value maximisation. This increase in the capital expenditures of bus companies roughly coincides with the drastic decrease in government capital investment in local public transport shown in Figure 3.

As such, it appears that the private investment is compensating for the reduction in public investment. However, the increase in capital expenditures of the 27 major bus company subsidiaries falls well short of the decreases in government capital investment in local public transport. The average capital expenditures of the major bus company subsidiaries amounted to £105 million per year from 2007 to 2010 and then doubled to an average of £214 million per year in the period from 2011 to 2020, an increase of £110 million per year between the two periods. Meanwhile the average government capital investment in local public transport was £810 million per year from 2007 to 2010, and then dropped to an average of £227 million per year from 2011 to 2020, a decrease of £584 million per year between the two periods.

When it comes to dividends, we see that they were relatively stable from 2007 to 2019. Overall, £820 million has been paid out by these 27 subsidiaries since 2010, which indicates that the major bus companies have been committed to distributing significant amounts of their profits to shareholders. Since the Covid-19 outbreak, there has been a ‘dividends drought,’ which has put a halt to the payouts to which bus company shareholders have become accustomed.

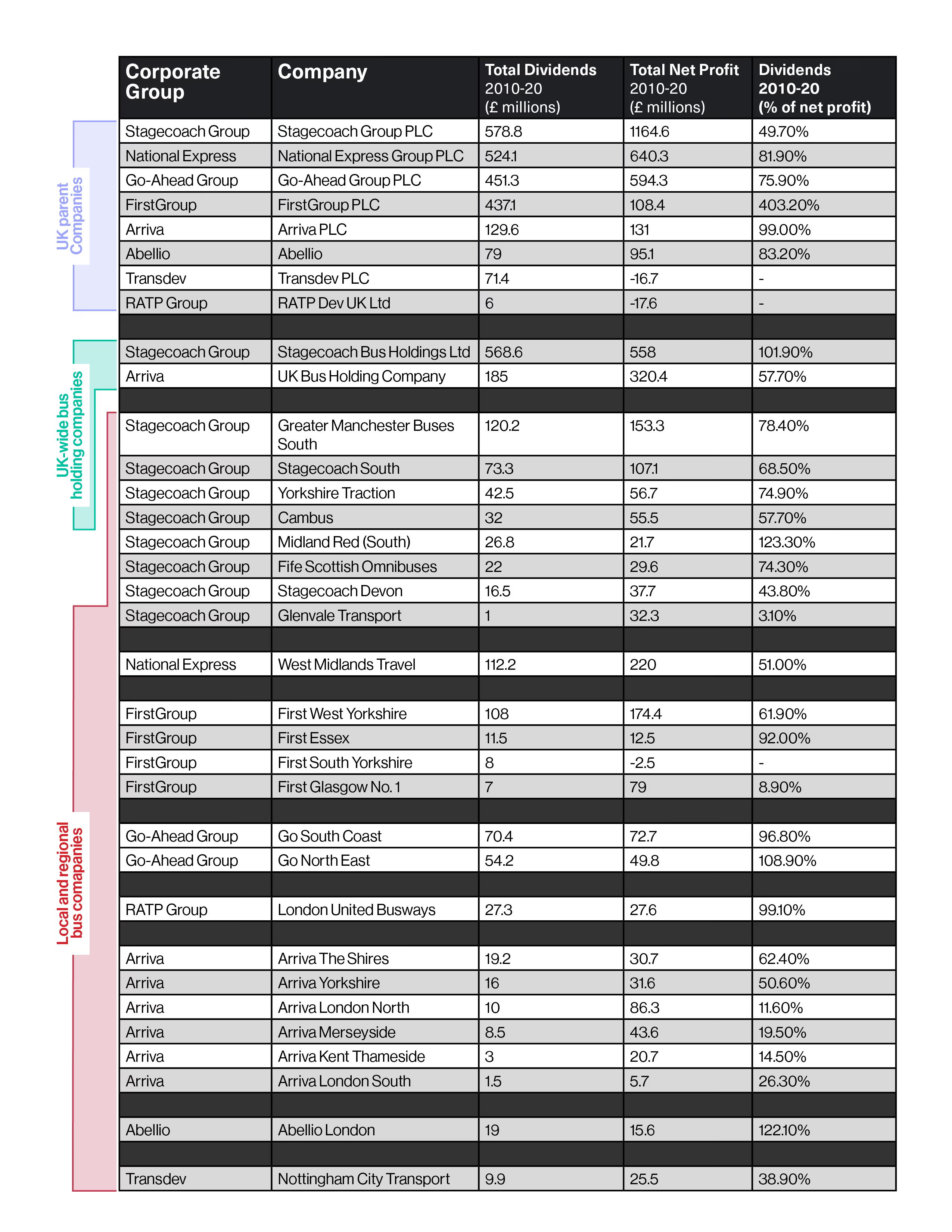

In order to get a more fine-grained perspective, Table 1 breaks down dividend payments by the UK parents and the subsidiaries of the major bus companies. The table shows that the situation is quite varied across levels of corporate organisation, and across the different regions of the UK. But one point to emphasise is that some of the bus subsidiaries operating in regions with the steepest hikes in bus fares (i.e. metropolitan areas outside of London) are paying out the most in terms of dividends. This includes FirstGroup’s First West Yorkshire (£108 million), National Express’s West Midlands Travel (£112 million), and Stagecoach Group’s Greater Manchester Buses South (£120 million).

[.fig]Table 1[.fig]

When we piece it all together, the significant bus fare increases that the UK has experienced serve a dual purpose. First, they finance the private investment of bus companies, partly offsetting the sharp cuts in government investment in local public transport. Second, they redistribute income from those reliant on bus services, many of whom find themselves in the bottom part of the income distribution, to the bus companies’ shareholders.

In March, it was announced that Greater Manchester's bus network would be brought back under public control, where operators bid to run services on a franchise basis. The plan was approved by the Greater Manchester Mayor, Andy Burnham, and backed by the overwhelming majority of the region’s councils. Burnham stated that bus privatisation since the 1980s has paved the way for "35 years of routes being cut and ticket prices rising".

Many campaigning for reform argue that deregulation has failed passengers by bringing about fragmented, unaffordable services and, in some cases, no services at all; an outcome that disproportionately harms poor people on low incomes and those that disproportionately rely on public transport systems, such as people with caring responsibilities that require multiple daily bus trips.

Service users are not the only group negatively impacted by the current ownership and operation of bus services. April witnessed a strike in Manchester after Go North West was accused of subjecting its bus drivers to ‘fire and rehire’, with Unite the Union stating: "Bus drivers who have kept working throughout the pandemic, risking their health and that of their families, deserve better than this.”

What does the situation look like in Greater Manchester where Mayor Andy Burnham has pledged to bring the bus system under public control? Figure 7 shows the major owners of the largest bus operators in Greater Manchester. It is interesting to note how the ownership network resembles the wider UK ownership network presented in Figure 4. As a sort of microcosm of the whole country, ownership of Manchester’s bus operators is dominated by a familiar combination of high net worth individuals and company founders, giant banks and asset management companies, as well as foreign governments.

[.fig]Figure 7: Major owners of the largest bus operators in Manchester[.fig]

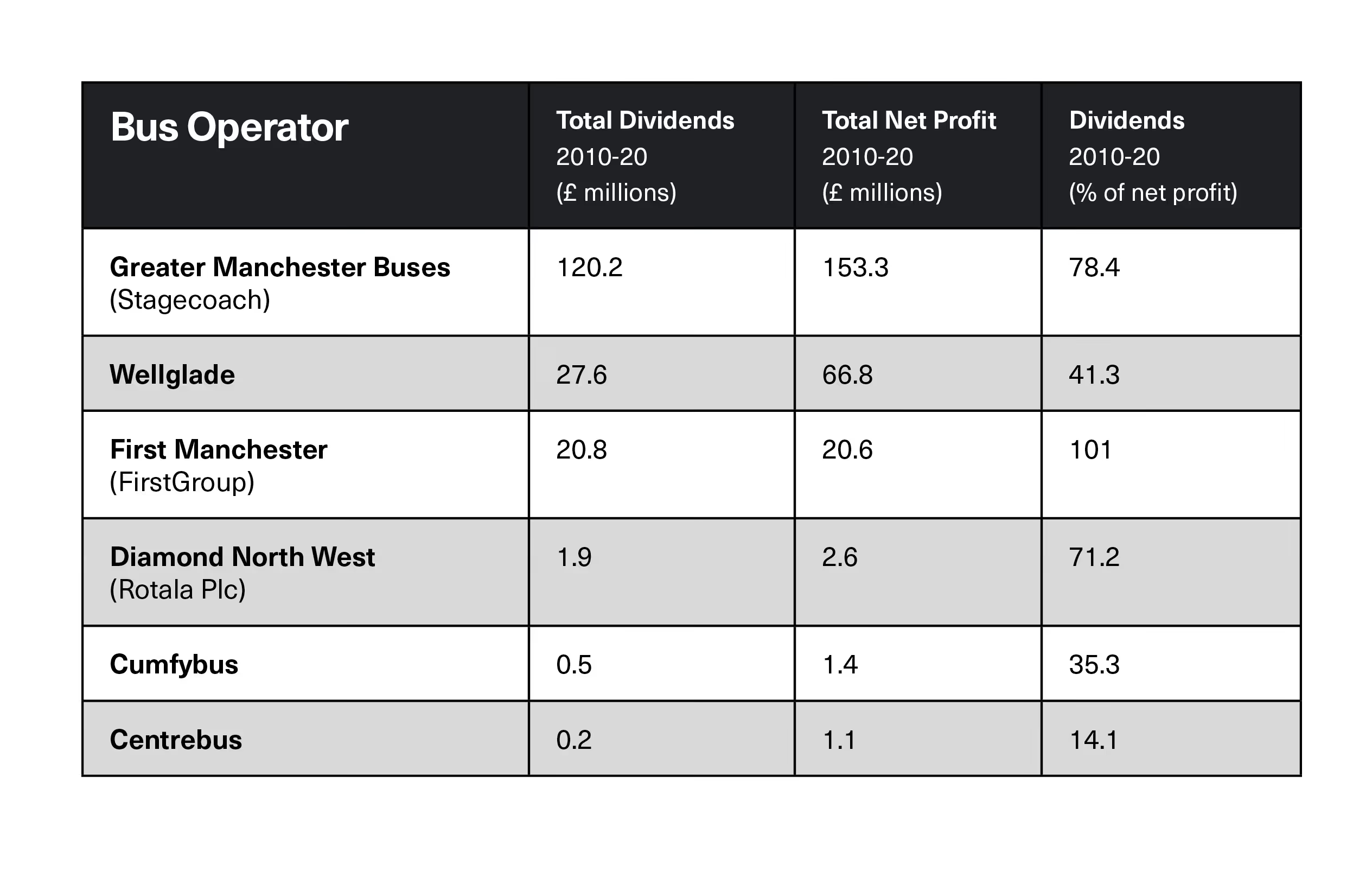

Table 2 tracks the dividend payouts of the Manchester-based operators. From 2010 to 2020, we see that the six bus operators distributed over £171 million in dividends to their shareholders.

[.fig]Table 2[.fig]

The largest three of these operators – Greater Manchester Buses, Wellglade and First Manchester – paid out 99% of these dividends. And Greater Manchester Buses South, whose parent Stagecoach is spearheading a legal challenge to block Burnham’s bus franchise system, has paid out 70 percent of those dividends, for a total of £120.2 million.

In place of the current model of privatised, deregulated provision, we should organise our bus networks based on forms of municipal and public ownership and democratic re-regulation of services. It is estimated new municipally run and publicly owned bus operations in Britain, outside London, could save over £500 million a year. As the National Union of Rail, Maritime and Transport Workers (RMT) says, “we need radical, meaningful action from Government to ensure that local authorities are able to provide affordable and reliable bus services to their community via a publicly owned municipal bus company.”

Rather than funnelling money into shareholder payouts, earnings can be reinvested in services. Under public ownership, this reinvestment could serve to reverse fare increases, decarbonise bus fleets, and rapidly expand accessible services, especially in rural areas. Replacing deregulated competition with public ownership can also enable better planning of the network.

We know this works as there are already successful publicly owned bus networks across the UK and beyond. As the campaign for 21st century public ownership, We Own It, have demonstrated:

Public ownership is already the norm elsewhere in Europe, such as in Germany where publicly owned operators provide 88% of all local public transport journeys. Publicly owned buses have also achieved lots in the UK. The 2016 UK Bus Awards were a resounding success for public ownership – with publicly owned Reading buses winning three awards and publicly owned Nottingham City Transport being named UK Bus Operator of the Year for the third year in a row. As a municipally owned bus service, Reading Buses can invest an additional £3 million a year in the bus network (around 12-15% of its annual turnover) because it doesn't pay out dividends to private shareholders. The extra money means better quality buses, one of the greenest fleets in the UK, and contributes to more people taking the bus in Reading. The UK’s largest public bus company, Lothian Buses, operates 70 routes in Edinburgh and the surrounding area. Levels of customer satisfaction for Lothian Buses are the highest in the industry and the publicly owned company recently returned £5.5 million to the public purse.

As demonstrated in places such as Preston and, more recently, North Ayrshire, Community Wealth Building strategies can help build resilient, democratised, thriving local economies and communities, rooted in the five pillars of Community Wealth Building set out by the Centre for Local Economic Strategies. Municipal bus services can play an important role in a wider transfer of physical and financial assets to local economies and communities.

Further, a rapid expansion of bus services can become a key lever to addressing the climate and environmental crises. By significantly reducing the number of petrol and diesel cars on the road, properly resourced, affordable, and accessible bus services can have an immediate impact on carbon emissions. But overall emissions from transport remain high. As such, a key priority for any government should be to decarbonise existing transport networks and invest in the roll out of low carbon alternatives, like procuring new fleets of electric buses.

As demonstrated by the recent strike action in Manchester, there is an urgent need to tackle poor pay and conditions for transport workers throughout a devastating and deadly pandemic. The shift towards municipal bus companies should thus come hand in hand with a concerted effort to dramatically improve workers’ rights in the transport sector, alongside a broader New Deal for workers, including but not limited to the creation of a new legal definition of a ‘worker’ to cover all existing employees and workers, guaranteeing a strong set of rights from day one, ending zero hours contracts, stronger and more equitable family friendly rights, an end to ‘fire and rehire’, and the significant expansion of sectoral collective bargaining.

It is clear that the deregulated, privatised model of bus service operation is incompatible with the integrated, fair, reliable and affordable services required to serve the needs of communities throughout the UK. In its place, we need a new era of municipal and public bus ownership to usher in a green, affordable, and vibrant future for passengers and communities across the UK.