Despite hosting a range of dynamic sectors and businesses, the British economy is defined by stagnation and inequality overall. The International Monetary Fund (IMF) forecasts that the UK will be the only G7 economy to fall into recession this year. [1] This reflects longer term economic stagnation; since the 2008 financial crisis, UK productivity has grown at half the rate of the 25 richest Organisation for Economic Cooperation and Development (OECD) economies. [2] Meanwhile, of the 38 OECD member states, the UK has the seventh highest level of income inequality — only Lithuania, the United States, Bulgaria, Turkey, Mexico and Costa Rica are more unequal. [3] Workers are further experiencing the sharpest fall in real wages since 1977 while FTSE 350 profit margins for the first half of 2022 were 89 per cent higher than in the same period in 2019. [4] An economic shock in an already-weak economy has translated into systemic upward redistribution.

Explanations for Britain’s poor economic performance have focused on the effects of austerity, Brexit, the long-term impacts of the global financial crisis and the after-shocks of Covid-19. [5] While these factors are important and self-reinforcing, they cannot wholly explain the extent of the UK’s stagnation and inequality, not least because many other economies have been hit by similar headwinds. As this briefing explains, one critical and consistently under-recognised reason for Britain’s economic struggles is its corporate governance regime — the set of rules that govern the company. Indeed, UK corporate governance is a notable outlier relative to other wealthy economies due to the extent to which it prioritises the interests of shareholders above all other stakeholders while denying workers formal participation rights in company decision-making. This concentration of power pressures companies to distribute earnings to shareholders instead of increasing investment and real wages, and limits the ability of ordinary people to shape — and improve — the strategic direction of their firm.

Corporate governance shapes both production (how corporations operate and innovate) and distribution (how corporate income is used, for example whether to increase wages, or distribute profits to shareholders). [6] Over the past 40 years, the UK has become an outlier among richer economies in its approach to corporate governance. [7] In contrast with less unequal and more productive economies such as Germany, France, the Netherlands, or the Scandinavian countries, UK corporate governance stands out in two ways: first, directors are required to organise the company to promote “the success of the company for the benefit of its members” — in other words, to maximise shareholder wealth and prioritise their interests — and second, workers and other essential company stakeholders are denied formal participation rights in decision-making. [8]

This “shareholder primacy” regime of corporate governance has helped produce key outcomes explored in detail below: corporations have pivoted away from investment in production toward growing shareholder wealth through rising asset prices and ever-larger shareholder payouts (for an illustration of this dynamic see Figure 3). [9] At the same time, real wages have stagnated: the median UK worker suffered a four per cent real earnings loss between 2008 and 2019. [10] As a result of this dynamic, dividends grew six times faster than real wages between 2000 and 2019. [11] The prioritisation of shareholder interests thus generates weak investment and high inequality, underpinning low productivity.

This briefing examines just how far outside of the mainstream the UK’s shareholder-centric corporate governance approach sits and the wider economic consequences of this approach. To do this, we compare performance across European economies on the European Participation Index (EPI) against key economic indicators including investment, business enterprise R&D investment, productivity, income inequality and real wages. [12]

[.box][.box-header]Box One: The European Participation Index (EPI)[.box-header][.box-paragraph]The EPI — produced by the European Trade Union Institute (ETUI) — is a measure of the degree of democracy at work in European countries. It is a composite index which summarises both formal rights and the extent of participation at three levels: in the board, at plant level and through collective bargaining. As the ETUI explain, it is a measure of three equally weighted components:[.box-paragraph][.box-paragraph3]Board-level participation — measures the strength of legal rights in each country for employee representation in the company's highest decision-making body.[.box-paragraph3][.box-paragraph3]Establishment-level participation — measures the strength of worker participation at the plant level.[.box-paragraph3][.box-paragraph3]Collective bargaining participation — measures union influence on company industrial-relations policies, including an average of i) union density (i.e. percentage of workforce belonging to unions) and ii) collective bargaining coverage (i.e. percentage of the workforce covered by collective agreements).[.box-paragraph3][.box]

[.img-caption][.img-caption-header]Figure 1 The UK is one of Europe's worst performers on the EPI[.img-caption-header][.img-caption-text]Source: European Participation Index[.img-caption-text][.img-caption-text]The authors would like to thank Sophie Monk for designing the charts used in this briefing and Chris Hayes for his input with the analysis.[.img-caption-text][.img-caption]

Two findings stand out. First, the UK comes third from the bottom in the EPI, above only Latvia and Estonia, reflecting the extent to which employees are denied participation rights in governance relative to most European countries. Second, explored in the remainder of this briefing, there is a correlation between low EPI performance and poor economic and social outcomes. These correlations indicate that companies perform better and workers thrive when employees have meaningful participation within the firm. Thus, modernising the UK’s corporate governance regime to include employee representation and to transform company purpose offers an opportunity to improve outcomes for all stakeholders: workers, society, and businesses.

[.img-caption][.img-caption-header]Figure 2 Business investment lags behind the OECD average[.img-caption-header][.img-caption-text]Source: World Bank[.img-caption-text][.img-caption]

The UK economy is as much an outlier in terms of low investment as it is for weak participation. Indeed, it is the joint second worst performing OECD member for gross fixed capital formation (a measure of investment) as a share of GDP; only Greece has lower rates of investment. [13] Making cross-country comparisons of investment is difficult owing to the cyclical nature of investment, the connection between investment and sectoral composition and varying levels of public expenditure. However, it is reasonable to infer that pressure to distribute private sector earnings to shareholders — often to the detriment of investment in production — is higher when a company’s priority is rewarding external investors, and when stakeholders with longer-term horizons, such as employees, are denied voice. [14] This inference is supported by firm level analysis of the German model of governance, which mandates worker representation on supervisory boards for companies with over 2000 employees outside the coal, iron and steel industries. Within this cohort, investment is lower at firms without co-determined governance. [15]

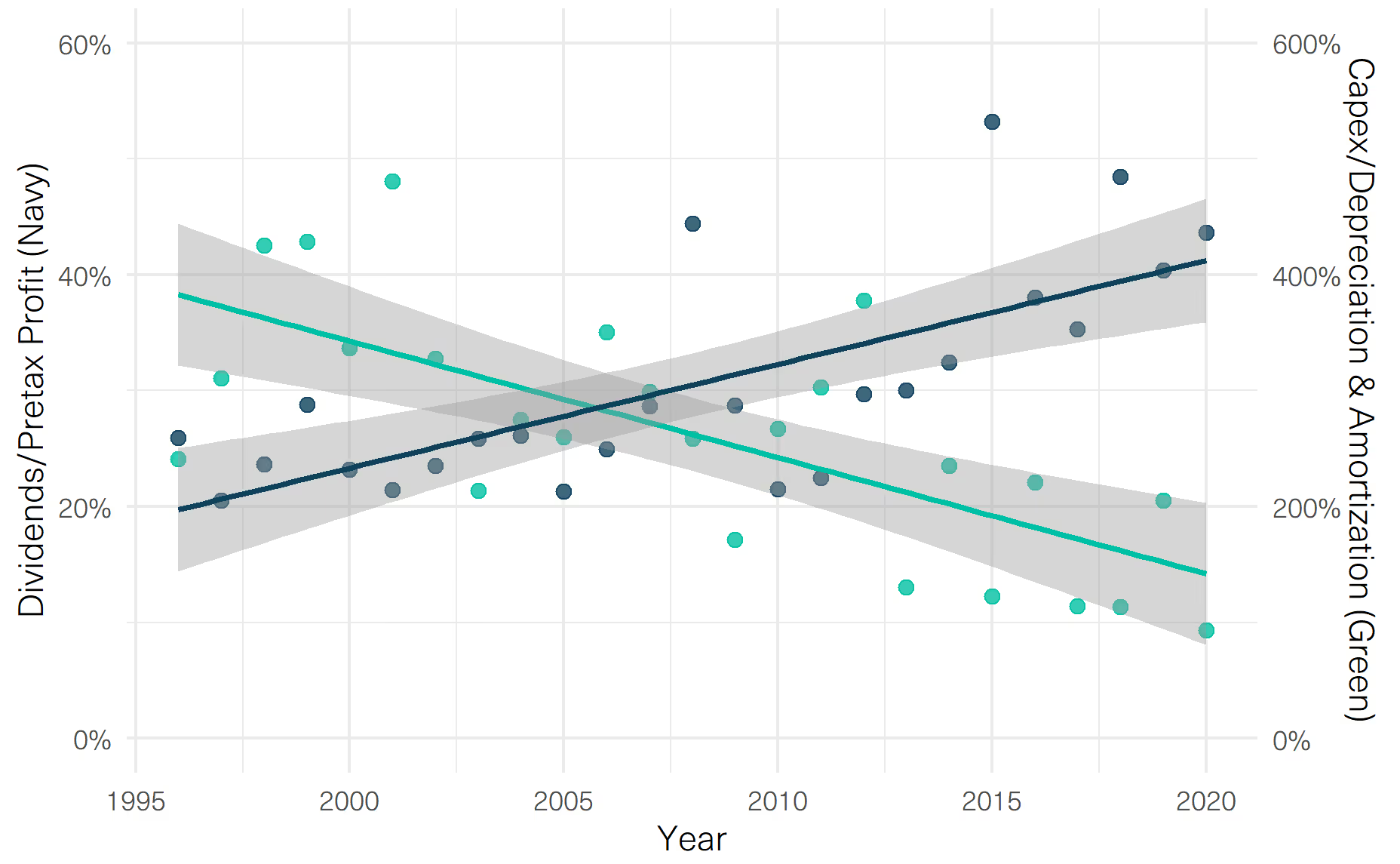

The UK is a model of the consequences of undemocratic company governance. A combination of corporate governance rules and pressure from financial markets to “disgorge the cash” have led companies to prioritise the distribution of their profits in the form of dividends and share buybacks, over increasing investment. [16] For example, in 2020, despite the effects of the pandemic, aggregate dividend payouts by FTSE 350 companies represented around 90 per cent of aggregate pre-tax profit. [17] Buybacks by UK firms reached over £55 billion in 2022, with Common Wealth and IPPR analysis finding that share repurchases by FTSE companies were twice as high last year as their pre-pandemic peak in 2018. [18] The exceptional level of shareholder payouts cements a two-decade trend in the UK economy that has seen the distribution of profits tilt further toward shareholders, with dividends rising six times faster than real wages between 2000 and 2019 while business investment remains chronically low. [19] Figure 3 makes this trend clear, demonstrating more than two decades of decline in business investment in the FTSE350 that has occurred alongside significant increases in dividends as a share of profit.

[.img-caption][.img-caption-header]Figure 3 Investment is falling in the FTSE350 while shareholder payouts rise[.img-caption-header][.img-caption-text]Source: Refinitiv[.img-caption-text][.img-caption-text]Note: Data shows the 121 firms in the index throughout the full period. Capex/Depreciation & Amortization is a measure of investment[.img-caption-text][.img-caption]

[.img-caption][.img-caption-header]Figure 4 Business expenditure on R&D as a percentage of GDP is correlated with economic participation across Europe[.img-caption-header][.img-caption-text]Source: OECD[.img-caption-text][.img-caption-text]Note: Bulgaria, Cyprus, Croatia, Malta and Romania have been excluded due to lack of data[.img-caption-text][.img-caption]

While it is more challenging to draw a direct correlation between business investment and economic participation in European countries, low levels of participation are correlated with lower levels of business investment in R&D, as illustrated by Figure 4. Countries with shareholder dominated corporate governance regimes encourage short-term company behaviour and a failure to invest in the research necessary to improve production. For example, analysis of firms listed on the Stockholm Stock Exchange between 2006 and 2014 showed that companies with employee representation were much less likely to make discretionary cuts to R&D when facing pressure on earnings. [20] R&D underperformance in the UK is significant: in 2020, business enterprise expenditure on R&D was 1.25 per cent of GDP, while the EU and OECD averages were 1.44 per cent and 1.92 per cent respectively. [21] The UK’s corporate governance system, its low levels of investment and its low investment in R&D are closely related, and help explain the country’s poor economic performance.

Business investment is fundamental to productivity growth. [22] Shareholder primacy and the corporate behaviours it induces can thus help explain the UK’s weak productivity outcomes: businesses prioritise distribution over investment, dragging down aggregate performance. At the same time, companies in which workers have participation rights are often more productive overall; the lack of formal representation and a guaranteed stake and say is therefore a further headwind. [23] For instance, analysis of German firms with and without worker representation on supervisory boards demonstrated that companies with shared governance systems produced between two and eight per cent greater value add per worker. [24] Across European countries, the moderate correlation between performance in the EPI and productivity shown by Figure 5 offers support for this connection, although the political economic specificities of the post-Soviet and former Warsaw Pact states are likely a factor in the correlation. This connection between productivity and economic participation indicates that the fundamental structure of the company contributes to the stagnation of the UK and other low participation economies.

[.img-caption][.img-caption-header]Figure 5 European economies with low economic participation have low productivity rates[.img-caption-header][.img-caption-text]Source: OECD[.img-caption-text][.img-caption-text]Note: Malta and Cyprus have been excluded due to lack of data[.img-caption-text][.img-caption]

[.img-caption][.img-caption-header]Figure 6 Income inequality is concentrated in economies with low economic participation[.img-caption-header][.img-caption-text]Source: OECD[.img-caption-text][.img-caption-text]Note: Income Inequality data is taken from 2019, apart from in the cases of Ireland, Poland and Italy, where the latest available data is from 2018. Cyprus, Croatia and Malta have been excluded due to lack of data[.img-caption-text][.img-caption]

As Figure 6 highlights, economies that lack institutions of workplace participation also tend to be more unequal. The European countries with the weakest participation rights in terms of union density, bargaining, and governance have above average levels of income inequality, while the economies with strongest guaranteed rights have levels of income inequality below the European average. This follows logically: when workers have little to no say in company decision-making and lack strong collective bargaining power, it is unsurprising that this power imbalance leads to an upward redistribution of income to those whose interests are prioritised. Rewards at the very top of the income scale exemplify this dynamic: of eleven major EU economies (which represent 85 per cent of companies in the S&P Europe 350), UK CEOs receive the second highest total compensation. [25]

[.img-caption][.img-caption-header]Figure 7 Employee participation rights are associated with higher real wages[.img-caption-header][.img-caption-text]Source: OECD[.img-caption-text][.img-caption-text]Note: Bulgaria, Cyprus, Croatia, Malta and Romania have been excluded due to lack of data[.img-caption-text][.img-caption]

Nor do imbalances in power due to the absence of participation rights just generate inequality, as Figure 7 suggests, they are also associated with weak real wages overall. In the UK, real wages are on a trajectory of decline: labour compensation per hour worked fell by 2.9 per cent in 2021, whereas in the EU, it grew by 0.77 per cent on average. [26] Between 2007 and 2021, the UK was one of only seven countries in the OECD in which real wages fell and the outlook for workers between 2021-22 and 2023-24 is similarly grim: the Office for Budget Responsibility predict the sharpest fall in living standards since records began in the 1950s. [27]

Firm level data on the relation between wages and worker representation in Norwegian and German companies indicates that increased board representation alone has little effect on wages. [28] However, the same analysis shows that in Norway, firms with higher unionisation rates pay higher wages. [29] Evidence from across Europe supports this picture, showing higher wages associated with collective bargaining agreements. [30] This connection between wages and collective bargaining reflects the correlation between the UK’s recent real wage performance and its near-bottom position on the EPI (the latter of which accounts for trade union density and collective bargaining coverage). Put simply, collective bargaining boosts pay and reduces inequality; economies in which it is widespread and legally supported are more equal and enjoy stronger real wages. At the same time, when power is concentrated and company purpose narrowly defined to maximise shareholder wealth, the primary claim on a company’s surplus and strategic direction is to reward its external investors, instead of prioritising better work and higher wages. The result is weak real wage growth for ordinary workers in economies geared toward rewarding wealthy asset-owners.

Corporate governance can sometimes seem a legalistic or abstract issue, distant from the concerns of everyday life. In practice, though often operating invisibly, the way corporations are governed decisively shapes how businesses operate, and therefore whether we live in an inclusive, dynamic and sustainable economy, or one — as at present — marked by stagnation and inequality. Reforming who has decision-making power within the company and its purpose is therefore critical to achieving the urgent changes necessary to ensure everyone has the opportunity to prosper: rising real wages built on strong productivity growth; decent and fulfilling work for all based on democratic production and non-exploitative relations; rising business investment to drive innovation and build the economy of the future, including just and rapid decarbonisation.

Achieving these goals will require a transition away from shareholder primacy to a democratic corporate governance model that gives real power to the varied stakeholders that make up the company. [31] Taken together, this new model of corporate governance should aim to rebalance and democratise distributional decision-making, with the goal of increasing investment and wages and supporting innovation in production. A democratic model can also embed climate safeguards, such as a green veto power, within corporate decision making to ensure that production is compatible with rapid decarbonisation — an approach connected to the inclusion of a broader range of stakeholders, with wider interests than shareholders. Specifically, by reorienting fiduciary duties away from maximising shareholder value and toward serving the interests of multiple stakeholder groups; by including workers in the governance of their workplace through employee representation on boards and in company membership; through the reintroduction of sectoral collective bargaining and union representation; through new institutions to guarantee employees share fairly in the profits they create; and through innovative action to decarbonise business activity, an ambitious reform agenda can transform the British economy away from stagnation and exclusion to a sustainable, dynamic and inclusive future.

Some might object that reform of company law would mark a shift to an “interventionist” agenda; however, this claim misunderstands the nature of the corporate form. Public power is already fundamental to constituting the modern corporation and how it is governed. The state grants companies extraordinary legal privileges as a benefit of their incorporation, including the rights to perpetual existence, limited liability and the ability to take out debt in the corporate name. These legal privileges — which, for instance, protect the future losses of shareholders if the company fails without protecting workers — should underpin a reciprocal relationship: in return for rights granted by the public, the corporate form should act as a vehicle for collective and shared prosperity rather than an engine of wealth extraction. The task is to rewrite the rules of the company to unlock the benefits of genuinely democratic, inclusive and thriving enterprise.

[#fn1][1][#fn1] “World Economic Outlook Update: Inflation Peaking amid Low Growth”, International Monetary Fund, 2023. Available here.

[#fn2][2][#fn2] Krishan Shah and Gregory Thwaites, “Minding the (productivity and income) gaps”, Resolution Foundation, 2023. Available here.

[#fn3][3][#fn3] Measured using the Gini coefficient, see “Income inequality indicator”, OECD, 2023. Available here.

[#fn4][4][#fn4] “For real wage data see “2022 is the worst year for real wage growth in nearly half a century”, Trades Union Congress, 2022. Available here. FTSE 350 profits see “Unite Investigates: Profiteering across the economy — it’s systemic”, Unite the Union, 2023. Available here.

[#fn5][5][#fn5] Adam Tooze, for instance, describes the combined effects of austerity, Brexit and the 2008 crisis on Britain. See Adam Tooze, “Nostalgia for decline in divergent Britain”, Chartbook, 2022. Available here. See also, for example, Resolution Foundation and Centre for Economic Performance, “Stagnation Nation: Navigating a route to a fairer and more prosperous Britain”, Resolution Foundation, 2022. Available here.

[#fn6][6][#fn6] Frederick Alexander, Holly Ensign-Barstow and Lenore Palladino, “From Shareholder Primacy to Stakeholder Capitalism”, Harvard Law School Forum on Corporate Governance, 2020. Available here.

[#fn7][7][#fn7] See Julian Franks, Colin Mayer, and Stefano Rossi, “Spending Less Time with the Family: The Decline of Family Ownership in the United Kingdom” in Randall K. Morck (ed.) A History of Corporate Governance Around the World: Family Business Groups to Professional Managers, University of Chicago Press, 2006, pp.581-611. On Margaret Thatcher’s reform to the taxation system to give tax relief to shareholders see Clare Munro, “The Fiscal Politics of Savings and Share Ownership in Britain, 1970-1980”, The Historical Journal, 2012, 55, pp.757-778.

[#fn8][8][#fn8] “Directors’ duties and responsibilities”, Institute of Directors, 2021. Available here.

[#fn9][9][#fn9] On the current disconnect between corporate income and investment – and the concurrent rise in shareholder payouts, see J.W Mason, “Disgorge the Cash: The Disconnect Between Corporate Borrowing and Investment”, Roosevelt Institute, 2015. Available here.

[#fn10][10][#fn10] Giulia Giupponi and Stephen Machin, “Labour market inequality, Institute for Fiscal Studies, 2022. Available here.

[#fn11][11][#fn11] Chris Hayes, “The Great Divide: Examining Labour Compensation and Dividend Growth”, Common Wealth, 2022. Available here.

[#fn12][12][#fn12] For more detail on the EPI see Stan de Spiegelaere and Sigurt Vitols, “A better world with more democracy at work”, European Trade Union Institute, 2020. Available here. See also Stan de Spiegelaere, Aline Hoffmann, Romuald Jagodziński, Sara Lafuente Hernández, Zane Rasnača and Sigurt Vitol, “Democracy at work” in Maria Jepsen (ed.) Benchmarking Working Europe 2019, European Trade Union Institute, 2019, pp.67-89.

[#fn13][13][#fn13] “Gross fixed capital formation (% of GDP) - OECD members, United Kingdom”, World Bank Data, 2023. Available here.

[#fn14][14][#fn14] Further, employee directors in China have been shown to reduce underinvestment at non state-owned enterprises. See Bingyi Huang and Yuting Huang, “Does employee representation affect corporate investment efficiency? Evidence from China’s capital market”, China Journal of Accounting Studies, 10, 2022, pp.120-144.

[#fn15][15][#fn15] See Simon Jäger, Benjamin Schoefer and Jörg Heining, “Labor in the Boardroom”, National Bureau of Economic Research, 2020. Available here. See also Nils Redeker, “The Politics of Stashing Wealth. The Demise of Labor Power and the Global Rise of Corporate Savings”, Center for Comparative and International Studies University of Zurich, 2019. Available here. As Redeker’s analysis shows, lower investment is also connected to the growth of corporate savings as well as pressure to reward shareholders. See for the shift in global savings away from households and towards companies: Peter Chen, Loukas Karabarbounis and Brent Neiman, “The Global Rise of Corporate Saving”, National Bureau of Economic Research, 2017. Available here.

[#fn16][16][#fn16] J.W Mason originally used the phrase “disgorge the cash” when describing this dynamic within US corporate governance. See Mason, “Disgorge the Cash: The Disconnect Between Corporate Borrowing and Investment”, Roosevelt Institute. Available here.

[#fn17][17][#fn17] “Do dividends pay our pensions?”, Trades Union Congress, Common Wealth and the High Pay Centre, 2022. Available here.

[#fn18][18][#fn18] On the level of FTSE100 buybacks in 2022 see Tom Howard, “Blue-chips buy back record £55bn of shares”, The Times, 28 December 2022. Available here For the Common Wealth and IPPR analysis cited see Joseph Evans, Chris Hayes and George Dibb, “Buy Back Better: The Case for Raising Taxes on Dividends and Buybacks”, Institute of Public Policy Research and Common Wealth, 2022. Available here.

[#fn19][19][#fn19] Hayes, “The Great Divide: Examining Labour Compensation and Dividend Growth”, Common Wealth. Available here.

[#fn20][20][#fn20] Conny Overland and Niuosha Samani, “The Sheep Watching the Shepherd: Employee Representation on the Board and Earnings Quality”, European Accounting Review, 31, 2022, pp.1299-1336.

[#fn21][21][#fn21] “Main Science and Technology Indicators”, OECD, 2021. Available here.

[#fn22][22][#fn22] For instance, see Juliana Oliveira-Cunha, Jesse Kozler, Pablo Shah, Gregory Thwaites and Anna Valero, “Business time: How ready are UK firms for the decisive decade?”, Resolution Foundation and Centre for Economic Performance, 2021. Available here.

[#fn23][23][#fn23] See Thomas Zwick, “Employee participation and productivity”, Labour Economics, 2004, 11, pp.715-740 for evidence that works councils amplify the positive productivity effects of greater shop floor level employee participation. Empirical evidence further indicates a connection between the greater density of cooperative institutions (defined through collective bargaining coverage, wage coordination and the rights of works councils) and the levels of robotisation (and thus innovation and productivity) in 25 OECD countries between 1993 and 2017, see Toon Van Overbeke, “Conflict or cooperation? exploring the relationship between cooperative institutions and robotisation”, British Journal of Industrial Relations, 2022 [Online preprint].

[#fn24][24][#fn24] Jäger, Schoefer and Heining, “Labor in the Boardroom”, National Bureau of Economic Research. Available here.

[#fn25][25][#fn25] Patricia Kotnik & Mustafa Erdem Sakinç, “Executive compensation in Europe: realized gains from stock-based pay”, Review of International Political Economy, 2022 [Online preprint].

[#fn26][26][#fn26] “Labour compensation per hour worked”, OECD, 2023. Available here.

[#fn27][27][#fn27] “UK workers miss out on £4000 in pay growth compared to OECD average since 2007”, Trades Union Congress, 2022. Available here. For living standards see “Economic and Fiscal Outlook”, Office for Budget Responsibility, 2023. Available here.

[#fn28][28][#fn28] Christine Blandhol, Magne Mostad, Peter Nilsson and Ola L. Vestad, “Do Employees Benefit from Worker Representation on Corporate Boards?”, National Bureau of Economic Research, 2021. Available here.

[#fn29][29][#fn29] Ibid.

[#fn30][30][#fn30] See for instance Wouter Zwysen and Jan Drahokoupil, “Are collective agreements losing their bite? Collective bargaining and pay premia in Europe, 2002-2018”, European Trade Union Institute, 2022. Available here.

[#fn31][31] [#fn31] On the essential need for — and social, ecological and economic benefits of — the democratic governance of firms, see Isabelle Ferreras, Julie Battilana and Dominique Méda (eds.) Democratize Work: The Case for Reorganizing the Economy, University of Chicago Press, 2022. See also Isabelle Ferreras, "Democratising Firms — A Cornerstone of Shared and Sustainable Prosperity", Centre for the Understanding of Sustainable Prosperity, 2019. Available here.