Already battling with the turmoil of Covid-19 and the complex challenges posed by Brexit, the UK economy is facing a fresh crisis: extraordinary spikes in wholesale electricity and gas prices.

Gas price hikes have led to gas in Europe trading at nearly three times the price of crude, as the consumer energy market faces the prospect of surging prices. Domestic energy bills are predicted to rise by at least 30 percent by early next year. Households whose deals on fixed-price energy have recently ended have already faced added costs. The UK is on track to witness the highest increase of domestic energy bills since records began in 2009.

The implications for energy retail companies are severe. A total of ten energy companies have folded due to rocketing natural gas prices since the start of August, meaning that 1.7 million customers have lost their supplier. There are nearly 50 energy suppliers in the UK, but predictions for their longevity are in doubt. With the energy market already dominated by a handful of larger companies, some executives predict that the sector could go back to as few as four companies.

Under the current approach to energy supply, the gas market remains important for industry, power generation, and domestic supply, with more than 22 million households connected to the gas grid.

Prime Minister Boris Johnson claims that the gas supply shortage is a knock-on effect as the economy begins to recover from the pandemic. The Department for Business, Energy and Industrial Strategy points to a series of additional factors, notably the winter surge in household demand, rescheduled maintenance projects from the previous year, and disrupted shipping of natural gas following an uptick in demand in Asia for Liquified Natural Gas.

The problems with the energy market, however, did not start with this crisis. From the lack of gas storage capacity leaving the UK’s gas supply more vulnerable to volatile global markets, to gas bills rising by 50% since 1996, and the average profit margins of big energy suppliers growing from 1 percent to 4 percent between 2009 and 2017, it is clear that systemic problems are designed into the current energy strategy. The current approach to the ownership and operations of energy companies points to deeper, systemic failures of the privatised energy market and its implications on energy security and supply.

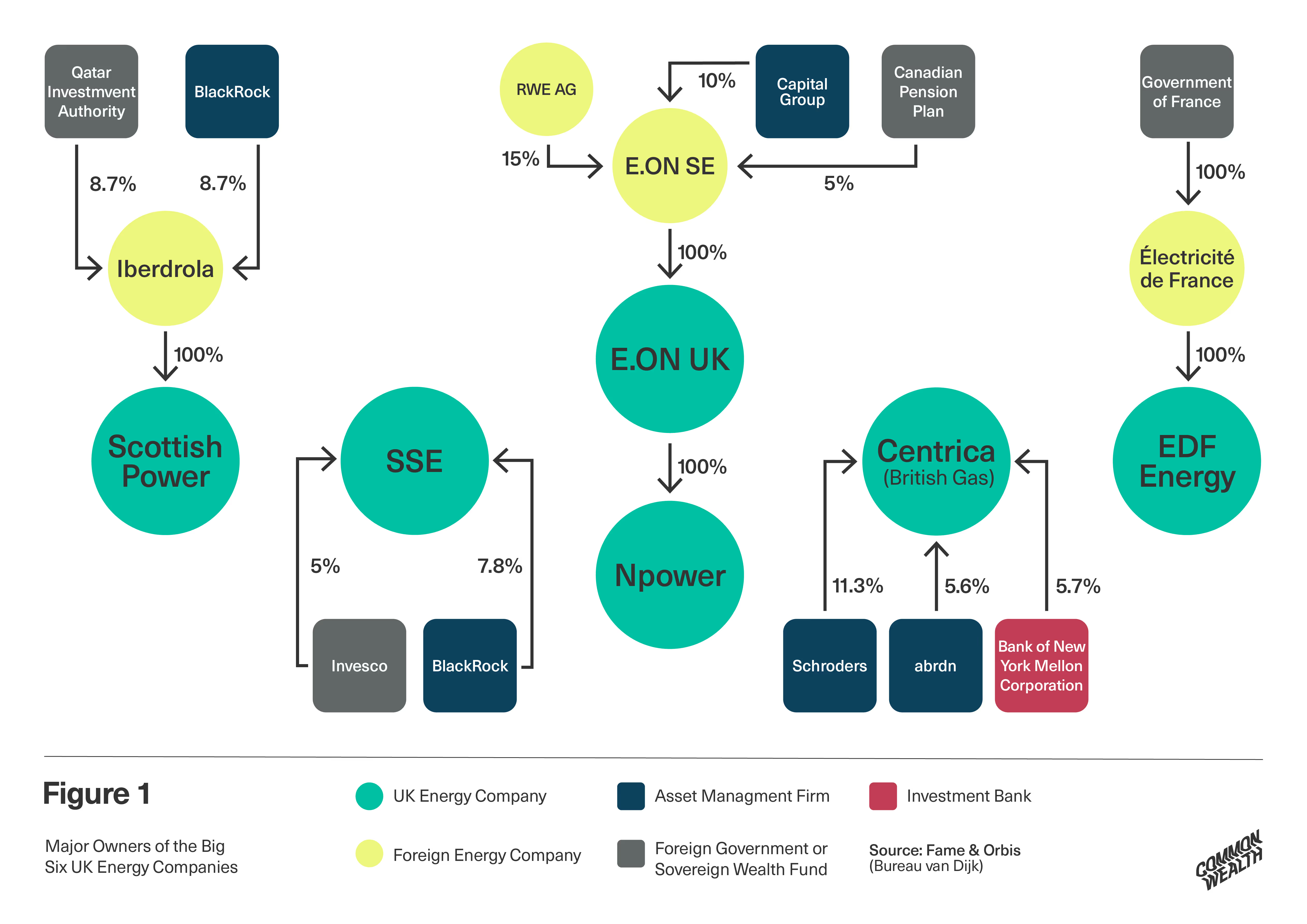

The privatisation of the UK's energy system that began in the late-1980s and early-1990s has given rise to a highly concentrated market dominated by the "Big Six” energy companies: British Gas (Centrica), EDF Energy UK, E.ON UK, npower, Scottish Power and SSE.

Figure 1 provides an overview of the ownership structures of the Big Six, listing the major shareholders with 5% or greater stakes in each company. The two major shareholders of SSE are giant US asset managers: BlackRock and Invesco. Scottish Power is 100% owned by Iberdrola, a Spanish energy electric utility which counts BlackRock and the Qatari Investment Authority as its major shareholders. In early 2019 Npower was bought by E.ON UK, making both subsidiaries of the German parent company E.ON SE. Among the major shareholders of E.ON SE we find RWE AG, another German energy company, Capital Group, a US asset manager, and the Canadian Pension Plan Investment Board, a Canadian Crown Corporation. EDF Energy UK is 100% owned by Électricité de France, a French public utility owned by the Government of France. And finally the major shareholders of Centrica, the lesser-known parent company of British Gas, include the UK asset management firms Schroders and abrdn, as well as Bank of New York Mellon Corporation, a US investment bank.

Figure 1 indicates that the energy company wealth that was once held by the UK Government has been transferred to a handful of private companies, investors, and foreign governments. Who benefits from this privatised ownership model? One way to explore this question is to examine how the earnings of the energy companies are divided amongst their stakeholders: shareholders, management, workers and government (for a general overview of firm governance in the UK, see Common Wealth’s Commoning the Company report).

Table 1 provides some metrics that allow us to gauge how the profits of the energy companies are distributed. These data are presented over a ten year period from 2011 to 2020 as well as a five year period from 2016 to 2020 in order to give a sense of the longer-term dynamics at play.The first two columns in Table 1 show the total amount of taxes and dividends the energy companies have paid for the two periods. According to the available data for the last ten years, the Big Six have paid out almost £23 billion in dividends: six times their tax bill for the period. The same pattern of potential income being effectively diverted from the public domain to the private is also in evidence for the past five years, with dividends paid to shareholders (£9.69 bn) once again six times larger than their tax payments (£1.52 bn). This starkly illustrates how the privatization of utilities has served to redistribute income - previously destined for the public purse - to shareholders. As established by Figure 1, some of the major shareholders reaping these dividends are foreign governments, while others are asset management firms and investment banks that principally service those households belonging to the top-end of the wealth and income distribution. Overall, the Big Six have paid out the equivalent of 82% of their pretax profit in dividends over the past five years, while their effective tax rate has been just 13% in the same period, well below the current statutory corporate tax rate of 19%.

[.img-caption]Table 1. Source: Data in table 1 were compiled in September 2021 using the Fame database from Bureau van Dijk. Note: Tax paid, dividend, net interest and capital expenditure data are for Centrica, Scottish Power, SSE, EDF Holdings Limited and E.ON UK (which also owns Npower).[.img-caption]

Interest payments on debt is another vector through which value has been captured by financial actors, rather than channeled to consumers and citizens. The data here are equally eye-opening with the Big Six incurring £10.22 bn in interest expenses over the past decade, and £3.95 bn over the past five years. These numbers represent over 2.5 times the amount paid in tax over the same two periods. Interestingly, the effective interest rate paid by the Big Six on their total debt has been relatively high: standing at 4.1% over the past ten year, and 3.2% over the past five: well above the average rates on long-term UK government debt in the same periods: 2.5% and 1.6%, respectively. This too shows how an energy system taken back into public ownership would potentially secure better value for money for citizens and consumers. Not only would it mean that no money would be diverted to shareholders via dividends, it would also mean that utility providers would not be paying elevated rates of interest in private debt markets. Under common ownership, such savings could be recycled into lower household energy costs as well as expanded investment in renewables.

The final column in Table 1 expresses as a ratio the salary of the energy company’s highest paid director relative to the average wage and salary of non-directors. This ratio can be seen as a measure of firm-level inequality, allowing us to assess how energy company earnings are being distributed to top managers relative to the average worker. Overall, we can see that the average firm within the Big Six has, over the past ten years, awarded their highest paid director almost fifty times the pay of the average worker in the company, and forty-five times the average income in the past five years. Moreover, according to available data, employee numbers of the Big Six have been cut by a third in the past decade, from 89,664 employees in 2011 to just 60,218 employees in 2020. The decline has been consistent each year, with no discernible impact from the Covid-19 pandemic itself. Therefore, taken together, the data show that the Big Six have been reproducing inequality within their own ranks through outsized director pay and worker layoffs, as well as in society at large via huge dividends that disproportionately benefit wealthy households in the UK and globally and elevated interest payments to private creditors.

Far from creating a competitive market and a shareholder democracy, the privatisation of the UK energy system has produced a highly concentrated market dominated by the Big Six. Without intervention, there is a danger that energy prices will continue to be intensely vulnerable to global market fluctuations and that companies will continue to fold at an alarming rate, further concentrating the market.

The analysis indicates that a privatised ownership model in the energy sector has highly uneven distributive consequences for stakeholders. The major shareholders and private creditors of the UK energy companies have reaped the benefit of huge dividends and elevated interest payments, respectively, both of which massively outstrip what the energy companies pay in taxes.

It is increasingly clear the current approach to energy ownership is failing, for consumers, workers, energy companies and energy security. Taking the energy sector back into public ownership could be key to securing a just energy transition: accomplishing better value money for consumers, more and better-paid jobs for workers, and an accelerated roll-out of the renewable energy infrastructure that the UK so desperately needs.

Public ownership of energy is already a reality in many other European countries, and is proving successful in many states. In Germany, for instance, two-thirds of all electricity is purchased from municipally owned energy companies and, since 2016, the Munich city council has supplied enough renewable energy for the needs of every household. As We Own It, a UK-based campaign organisation championing public services for people not profit, points out, Denmark has a fully publicly owned transmission grid, and the highest proportion of wind power in the world. A publicly owned energy system can be complemented by smaller-scale developments, like community-owned energy. In 2008, the isle of Eigg was the first community to launch an off-grid electric system powered by wind, water and solar, allowing local people to have a greater stake and say in their energy.

As the analysis reveals, the sizeable pay gap and the declining workforce within the Big Six raises questions about the unequal relations between top managers and average workers. This unequal relationship was laid bare when British Gas used ‘fire and rehire’ tactics, leading to 7000 engineers staging 44 days of strike action after they were threatened with losing their jobs should they not agree to new terms and conditions. An agreement was reached following what GMB describes as “gruelling negotiations.” This stark example points to deeper imbalances designed into the labour market, necessitating a broader New Deal for workers that bans ‘fire and rehire’, roots our precarity and insecurity, and significantly enhances workers’ rights and power.

A New Deal for workers can provide a foundation from which we can build an ambitious green industrial strategy, investing in green industries and infrastructures of the future, significantly increasing renewable energy capacity - which the UK is well placed to do - and output to reduce reliance on fossil fuel intensive energy sources and diversify the energy market. An ambitious green industrial strategy should extend to all corners of the economy. National retrofitting programmes for homes can and should be a pillar of this, reducing energy costs, tackling fuel poverty, and creating good, green jobs throughout the UK. Importantly, while the fossil fuel era has been dominated by concentrated ownership and extraction, a just transition presents an opportunity to reimagine a new institutional framework centred on democratic management, sustainability and shared prosperity.