A devastating public health crisis, Covid-19 has also triggered a profound crisis of the company: from vast multinational corporations to the small firms that are the lifeblood of local economies. The unprecedented economic fallout from the virus has exposed the inefficiencies and injustices embedded in the company’s operation – limitations that stretch back decades. Our response to this crisis cannot ignore these limitations when we emerge from the period of economic hibernation. Instead, it must reimagine the company so that it is democratic, resilient, and sustainable by design – and rebuild a new economy centred on meeting the needs of society and the environment.

Since the 1970s, the company has transformed from an institution focused on production – even if still one laced through with hierarchy and injustices – into an engine of increasing wealth extraction and growing financialisation, funnelling cash to shareholders and executive management in the form of dividends, share buybacks and share-based pay awards. This has been driven by key shifts in the legal, managerial, and ownership structures of the corporation, with an increasing share of corporate earnings redirected to investors and management over workers or re-investment. Shareholding has concentrated and corporate debt has soared, with UK listed company debt reaching record levels by 2018;[1] mergers and acquisitions have created dominant oligopolies in key sectors; managerial power has grown; and labour has been subject to a relentless squeeze on wages, autonomy, and security in order to boost short-term profit.

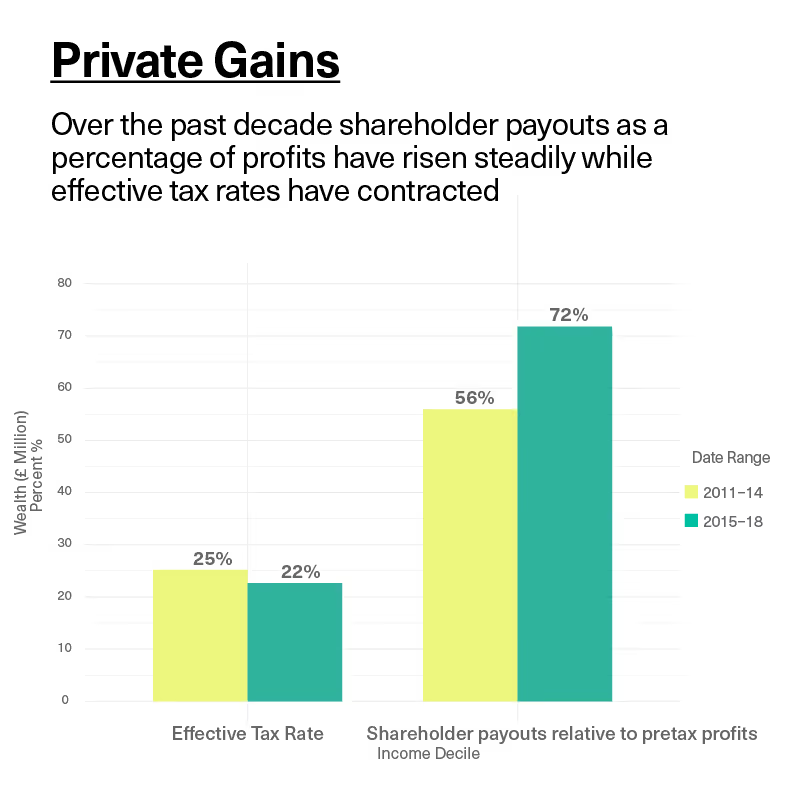

Corporate earnings have in turn been redirected to shareholders in the form of rising dividends and share buybacks, rather than re-invested in the productive capacity of the firm or in rising real wages, with corporate cash shifting from productive to financialised use. In the 8 years between 2011 and 2018, the 100 largest UK-domiciled non-financial companies paid out over £400bn in dividends – the equivalent of 68% of their net profits over the period – and an additional £61bn in buybacks.[2] In 2019 alone, dividend payments from FTSE100 listed companies, a slightly different cohort including financial companies and non-domiciled corporations, hit a record £110.5 billion – a rise of 10.7% over 2018 and more than double the £54 billion paid out in 2009.[3] And executive remuneration has become entirely disproportionate to performance. As of latest filings, just over 700 executives at 86 of the 100 largest non-financial UK companies held a collective £6 billion in equity at their respective corporations, representing nearly £8.5 million per director.[4]

Workers, companies themselves, and the public have lost out. Corporate behaviour has left our economy ill-prepared for crisis – less resilient as a whole and with income, wealth, and power intensely concentrated, leaving many acutely vulnerable. What’s more, absent intervention, the crisis will likely result in a further consolidation in ownership, with distressed firms purchased on the cheap by large corporations and private equity, accelerating the concentration of wealth and power.

This is not inevitable. The corporation is an entity with a separate legal personhood endowed by the law with extraordinary privileges to organise production. It is not a fixed, ‘natural’ institution, but rather constituted by politics and law. Economic coordination rights in the corporation are currently assigned exclusively to capital via property; labour is excluded from the government of the company. Yet these rights and powers are publicly granted, legally defined, and re-codable; the corporation is not a space of private contract and property whose actions should be shielded from democratic intervention, but rather one undergirded and made possible by public power. The crisis, like so many before it, has underscored this codependency and the inseparability of the economic from the political. If the corporation is the original and vital public-private partnership, long captured by elite shareholder interests and managerial power, we can still transform it from an institution of extraction to a generative entity: purposeful and democratically governed, where all its stakeholders have stake and a say in the wealth we create in common.

[.notes]Source: Orbis & Zephyr databasesNotes: Aggregate data for the 100 largest non-financial companies domiciled in the UK.[.notes]

[.num-list][.num-list-num]1[.num-list-num][.num-list-text]Company bailouts should be conditional on working for the public good[.num-list-text][.num-list]

[.num-list][.num-list-num]2[.num-list-num][.num-list-text]Create a state holding company to secure a pluralistic business landscape[.num-list-text][.num-list]

[.num-list][.num-list-num]3[.num-list-num][.num-list-text]Create a social wealth fund to broaden ownership and improve outcomes[.num-list-text][.num-list]

[.num-list][.num-list-num]4[.num-list-num][.num-list-text]Rewrite the rules to democratise the company[.num-list-text][.num-list]

[.num-list][.num-list-num]5[.num-list-num][.num-list-text]Build resilience to future crisis by embedding ambitious net-zero targets in the design of the company[.num-list-text][.num-list]

All crises buckle and reshape the order of things; in what direction and in whose interest depends on politics and the balance of power within society. The immediate challenge is to rapidly scale up healthcare capacity while taking measures to ensure households and businesses can securely remain in economic hibernation for as long as the public health crisis demands. But it is critical we simultaneously prepare for an agenda of ambitious reconstruction for the post-crisis period: one that builds a new economy fit for human flourishing, rather than simply re-inflating the inequalities and insecurities of the old. The transformation and democratisation of the company must be fundamental to this.

[#fn1][1][#fn1] Link Asset Services (2019) ‘UK PLC Debt Monitor’, 1 July 2018. Available here.

[#fn2][2][#fn2] See Table 1, Appendix

[#fn3][3][#fn3] James Gard (2020) ‘Record 2019 for UK Dividends’, 27 January 2020, Morningstar. Available here.

[#fn4][4][#fn4] Source: BoardEx database. Includes directors with known equity stakes at the 100 largest non-financial companies domiciled in the UK. Note that 14 out of 100 companies analysed did not have data available. The mostrecent available data varies by company, with filing dates ranging from 09/2018 to 12/2019.